(Bloomberg Opinion) --

It’s going to be unbearably hot across much of the U.S. this weekend, but the early returns on industrial earnings have been decidedly cool. A nearly 30% run in CSX Corp. shares heading into its second-quarter earnings report suggested this was a company where investors thought they could find shelter amid a growing body of worrisome manufacturing data. They were wrong. The shares slumped more than 10% the day after CSX reversed a forecast for low single-digit growth in revenue this year and predicted instead that revenue would dip as much as 2%. The East Coast railroad says it’s being cautious, but the time for conservatism is when you start the guidance-giving process, so that strikes me as an inadequate explanation for such a deep cut. CEO James Foote said the macroeconomic backdrop was one of the most “puzzling” he’s ever experienced and that there are no concrete signs of improvement in weak coal, intermodal and industrial volumes.

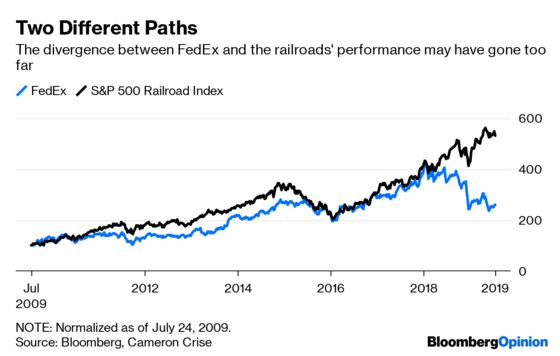

Elsewhere in transportation, J.B. Hunt Transport Services Inc. and West Coast railroad Union Pacific Corp. actually saw their shares pop on earnings, but that seems to be a case of more realistic expectations than a drastically more positive view of the macroeconomic environment. J.B. Hunt was essentially flat going into earnings, for example, and Union Pacific had sold off in sympathy with CSX before it reported. Union Pacific said it expects second-half volume to be down about 2%, which implies a decline for the full year compared with an earlier call for a low-single digit gain – basically mimicking CSX’s move. The other challenge with CSX is that it appears to be far enough along in its conversion to precision-scheduled railroading that there isn’t as much fat left to cut as there is at Union Pacific. But it’s track record of improved performance is still relatively short, capping its ability to make market share gains amid a surplus of capacity and lower spot rates in the trucking market. Bloomberg News’s Cameron Crise points out the sharp divergence in the performance of S&P 500 railroads and FedEx Corp. over the past, calling it a proxy of sorts for the trade war-inspired slowdown that’s hit companies with international exposure like FedEx harder than those focused on the domestic market. If U.S. railroad stocks fail to recover from the CSX-inspired selloff and the gap to FedEx narrows, that could be a sign that the domestic economy and the bull market are running out of steam, he writes. FedEx, of course, has plenty of idiosyncratic issues holding back its stock. The company’s annual report filed this week included interesting disclosures abut the risk of an activist shareholder getting involved and some additional detail on the logistics investments that could render Amazon.com Inc. a competitor.

Things were a bit better at the multi-industrial companies, but there was still cause for concern. Textron Inc. said its aviation backlog slipped by $100 million in the second quarter as macroeconomic concerns and President Donald Trump’s threat to impose wide-ranging tariffs on Mexico spooked business-jet customers. That’s counteracted by Honeywell International Inc.’s report of double-digit sales growth for new business jet equipment, but still a troubling sign of just how nervous people are about making big investments. You can usually count on Honeywell to churn out an earnings beat, and the company didn’t disappoint, raising its profit guidance for the full year. But the outlook wasn’t as robust as some analysts were expecting. Organic sales growth of 5% could end up being the pace to beat this quarter, but that was weaker than anticipated and a forecast for 2% to 4% growth in the third quarter would suggest an accelerating slowdown. The dynamic of somewhat disappointing sales numbers but steady earnings growth in some ways reinforces Honeywell’s argument that last year’s breakups and a pristine balance sheet will make it more resilient in a downturn, but I remain unconvinced that margins for anything except funeral homes are recession-proof. It helped Honeywell that the sales weakness was mostly confined to its safety and productivity solutions unit, the smallest of its four main businesses, and aerospace remained impressively robust with 11% organic sales growth. The industrial companies on tap to report earnings next week may not be so lucky, particularly 3M Co., which seems destined for yet another guidance cut to reflect the deepening slowdown.

ALL BOEING WANTS FOR CHRISTMAS IS A FLYABLE MAX

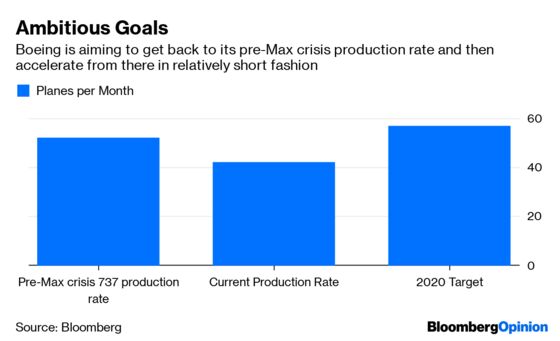

Boeing Co. this week pre-announced a $4.9 billion after-tax second-quarter charge to reflect its estimate of compensation owed to airlines grappling with a grounding of the beleaguered 737 Max that’s now entering its fifth month. American Airlines Group Inc., Southwest Airlines Co. and United Airlines Holdings Inc. this week pulled the Max from their schedules through the beginning of November – a timeline that jibes with Boeing’s call for the plane to return to service during the fourth quarter. But the risk remains that the grounding stretches into 2020. The Federal Aviation Administration, mindful of restoring its reputation as the global standard-bearer of safety protocol, is keen to coordinate a return to service with European and Asian regulators. And while a fix for the flight-software system linked to the Max’s two fatal crashes has essentially been completed, there remain hurdles to remedying a separate issue with a microprocessor that was identified in June, including convincing the FAA that a software update is sufficient, according to the Wall Street Journal. Even if Boeing can get the plane recertified and flying again by the fourth quarter, it matters a great deal which particular month that happens. Airlines estimate it will take a month to 45 days to complete the maintenance necessary to bring the Max jets they already operate out of storage, which is to say nothing of the additional planes they had been expecting to support busy schedules. I would imagine airlines’ demands for compensation would rise materially if they are forced to scramble and reassess capacity for holiday flights. Ryanair Holdings Plc said this week it’s prudently planning for a December return of the Max, but pared its growth plans for the 2020 summer travel season. It can only accept six to eight new Max planes per month, which will leave the budget airline with about half of the fleet it had been planning on for that peak season. Data points like that make me highly skeptical of Boeing’s aspirations to ramp up to a 57-per-month production pace for the 737 program in 2020.

A WORD ON WAREHOUSES

There has been a surge of spending over the past few years on industrial warehouse assets. The latest deal came this week , when Prologis Inc. agreed to buy Industrial Property Trust and its 236 properties in areas such as the San Francisco Bay Area, Chicago and New Jersey for about $4 billion. This follows Prologis’s acquisition of DCT Industrial Trust Inc. last year for more than $8 billion and its pursuit earlier this year of GLP Pte’s U.S. warehouse assets, which ultimately went to Blackstone Group LP instead for $18.7 billion. Meanwhile, Tom Barrack’s Colony Capital Inc. is exploring a sale of its unit that owns warehouses as part of a strategic review meant to resuscitate its plunging market value, according to Bloomberg News. I understand the logic of these deals: Retailers are under immense pressure to build out their e-commerce capabilities and shorten their delivery times and on the face of it, that trend looks less vulnerable to the trade war and macroeconomic uncertainties than many others. Even so, it gives me pause to hear Honeywell say customers for its Intelligrated warehouse-automation business are pushing major system rollouts into the second half of the year. Intelligrated is still growing rapidly, with organic sales growth of more than 20% for the first half of 2019, and Honeywell CEO Darius Adamczyk said he knew for a fact that the delayed orders hadn’t gone away. But going back to my earlier comment about funeral homes, I’m getting less confident that even this trend can withstand the test of a true downturn. I asked Bloomberg Opinion's retail expert Sarah Halzack what she thought. She pointed out that companies like Walmart Inc. and Williams-Sonoma Inc. are too far along in converting their businesses to e-commerce to back out, whereas those who are already struggling such as J.C. Penney Co. will find it harder to justify making those kinds of investments.

DEALS, ACTIVISTS AND CORPORATE GOVERNANCE

John Flannery has resurfaced. The former CEO of General Electric Co. will now be an advisory director to Charlesbank Capital Partners, a middle-market private equity firm managing more than $5 billion of capital. I’ve always felt a bit bad for Flannery, who spent 30 years working his way up the ladder at GE and finally ascended to the CEO post, only to find out that his actual job was going to be more akin to a garbage man. Sure, he made his share of mistakes as CEO. But the reality is he was probably never going to last in that job no matter what he did. GE needed one CEO to publicize and unearth the skeletons in its closet ($22 billion goodwill writedown on the disastrous Alstom SA deal, $15 billion reserve shortfall in the long-term care insurance business) and another CEO to try to fix the mess. That’s now Larry Culp. Still, it has to sting a bit that Steve Bolze, Flannery’s competitor in the race to succeed Jeff Immelt, is a senior managing director at Blackstone, a slightly more prominent firm than Charlesbank. Bolze is blamed by many investors for mismanaging GE’s power unit and exacerbating the financial pain from a slump in gas turbine demand.

Crane Co.’s bid for Circor International Inc. got a last minute surge of support. Mario Gabelli’s Gamco Investors Inc. agreed to tender shares to Crane after the buyer raised its price to $48 a share earlier this month. Roughly 45% of outstanding Circor shares have been elected to be tendered, people familiar with the matter told Bloomberg News. That’s not enough to force a merger (although there are still a few more hours before the tender offer expires at midnight), but it should be enough to get the attention of Circor’s board’s. In the wake of the Crane offer, Circor laid out a bold (and by nature, rather fluffy) plan to boost margins and lower debt. Shareholders are now signaling quite loudly that they don’t have much faith in the company’s ability to follow through. It’s pretty remarkable to see this level of pushback outside of an annual meeting, though. I had worried Crane’s bid might have been the victim of bad timing, with its offer becoming public a few weeks after Circor’s 2019 meeting. The fact that Circor’s board had privately received the Crane offer prior to the meeting and didn’t feel a need to tell investors about it has been one of Gabelli’s chief criticisms. This level of support from Circor shareholders may save Crane from having to wait a year to relaunch its bid with a proxy fight.

Osram Licht AG, the lighting maker that’s agreed to sell itself to Bain Capital and Carlyle Group LP, disclosed this week that Austrian industrial manufacturer AMS AG had made a fresh offer for the company at a higher price. Bain and Carlyle are offering 35 euros per share, or 3.4 billion euros ($3.8 billion), while AMS had proposed to pay 38.50 euros per share, or about 3.7 billion euros. The problem is, AMS itself is valued at less than what it offered for Osram; it’s had negative free cash flow for at least the past two years; and it’s already carrying about 1.2 billion euros of net debt. Osram agreed to let AMS perform due diligence, but said the probability of a deal materializing was “rather low.” Literally the same day that its latest offer was disclosed, AMS said it was walking away. In some ways that’s actually kind of surprising – why wouldn’t you take the opportunity to do due diligence? But anyway, this amusing M&A adventure has now come to an end.

Callon Petroleum Co. agreed to buy Carrizo Oil & Gas Inc. in an all-stock transaction valued at $3.2 billion including debt. Bernstein analyst Bob Brackett called it a “pretty lame deal all-in-all”, while my Bloomberg Opinion colleague Liam Denning said the merger sounds a “distinct sad-trombone note.” Carrizo helps Callon double down on the Delaware Basin with contiguous acreage and lets it add free cash flow on the cheap, but it also dilutes its status as a pure-play operator by adding acreage the Eagle Ford region, where it may be harder to find cost savings. Some investors may have viewed Callon as a target and are disappointed to see it on the other end of a deal. The consolidation of shale players is healthy and necessary, Liam writes. But the fact that Carrizo has chosen to sell at a modest premium when its stock was trading at the lowest levels in a decade is pretty telling, too.

CRH Plc agreed to sell its European plumbing and heating-distribution business to Blackstone for 1.64 billion euros ($1.9 billion). CEO Albert Manifold has been trying to steer the company toward higher growth markets including cement and raise money for acquisitions. This deal helps it do both. Davy analyst Robert Gardiner says the purchase price is attractive at about 16 times earnings before interest and taxes.

BONUS READING

Saturday Will Be Hot. Oil and Gas Will Be Not: Liam Denning

Axalta Is Said to Draw Interest From Kansai Paint and PPG

Ex-Cons Find Second Chances Easier to Get in Tight Labor Market

The Moon Is the Next Frontier in Rivalry Between China and U.S.

Porch Pirates Spot Criminal Opening in Amazon Prime Day Bonanza

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.