Cruise-Line Bonds Buoyed by Huge Yield Buffer for Now

(Bloomberg Opinion) -- Imagine this scenario unfolding in the span of just three weeks:

- Two large junk-rated companies extend their suspension of all U.S. operations until at least Oct. 31.

- To get by, they borrow a combined $1.6 billion of bonds and loans after already piling debt onto their balance sheets several times during the coronavirus pandemic.

- Moody’s Investors Service downgrades both companies by three levels in what’s colloquially referred to as a “superdowngrade,” citing high leverage and uncertain earnings potential. Analysts warn of additional cuts deeper into junk over the longer term.

This was August for Carnival Corp. and Royal Caribbean Cruises Ltd.

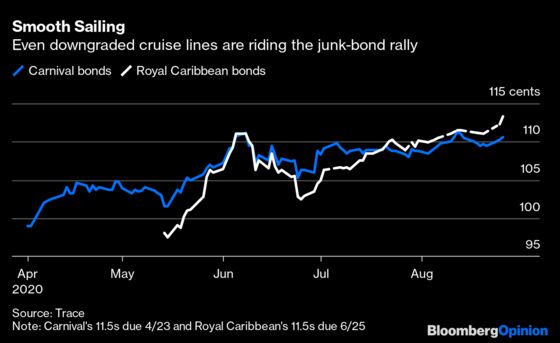

And yet, in what may seem counterintuitive, investors have reacted to these developments by bidding up prices on the junk debt of the two largest global cruise-line operators. Consider Royal Caribbean’s bonds, which were issued in May with investment grades from both Moody’s and S&P Global Ratings. Now rated two steps into speculative grade by Moody’s, the securities due in June 2025 traded Wednesday at 113.5 cents on the dollar, the highest price yet. Similarly, Carnival’s debt maturing in April 2023 has rallied in each session since the Moody’s downgrade on the largest trading volume this month.

It’s tempting to explain this away as “the bond market had it right all along” and Moody’s is just now catching up to what investors knew about the difficult path forward for cruise lines. Indeed, Carnival’s bond sale almost five months ago was run off of JPMorgan Chase & Co.’s high-yield syndicate desk, even though it carried investment grades. It’s hardly a secret that the likes of Carnival and Royal Caribbean, along with other travel and leisure companies, would suffer the most financially as long as persistent Covid-19 outbreaks flare up across the U.S.

That explanation doesn’t tell the whole story, however. If Moody’s had moved in line with market pricing, its downgrade would have been even more severe. If anything, the recent rally could be viewed as temporary relief among investors that the credit-rating company didn’t have an even more dour outlook for the cruise-line industry. For now, credit buyers have been given the go-ahead to coast on super-high interest rates from this year’s bond sales.

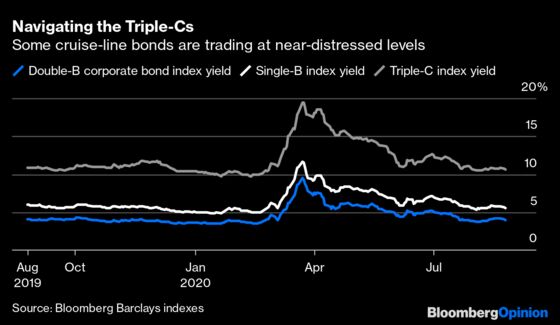

The above-par prices on debt from Carnival and Royal Caribbean largely reflect that both companies had to offer interest rates of 11.5% for enough investors to lend them cash even though the bonds are first-lien obligations and rated two steps higher (Ba2) than their overall grade. Carnival’s debt due in April 2023 yields 6.6% and Royal Caribbean’s securities maturing in June 2025 yield 7.6%. By contrast, the average yield on a Bloomberg Barclays index of double-B rated corporate debt is 3.92%, and the index of single-B debt yields 5.51%.

A look at older obligations provides an even more sobering view of the industry. Carnival has senior unsecured bonds, rated B2 by Moody’s, that were issued in 1998 and mature in 2028. They last traded at 84 cents on the dollar to yield 9.7%. Royal Caribbean debt with the same Moody’s rating and maturing around the same time trades at 74 cents to yield 8.4%. Bonds issued late last year by Norwegian Cruise Line, the smallest of the three and also cut three steps by Moody’s, last traded at 68 cents to yield 13.7%, or 300 basis points more than a Bloomberg Barclays index of triple-C rated junk bonds. That’s typically the point at which investors have to separate the distressed companies from those that are doomed.

Moody’s, which put the companies on review for downgrade on July 14, suggests it’s too soon to call for their demise. All have “good liquidity,” with enough cash to cover needs over the next 12 to 18 months and strong positions within the cruise-line industry. In the short run, their businesses “will be dominated by the length of time that cruise operations continue to be highly disrupted and the resulting impacts on the company's cash consumption and its liquidity profile.” Yet “over the long run, the value proposition of a cruise vacation relative to land-based destinations, as well as a group of loyal cruise customers, supports a base level of demand once health safety concerns have been effectively addressed.” Moody’s base case is for U.S. cruising to resume in the first half of 2021. If that doesn’t happen, or if the companies need to take on even more debt to stay afloat, it would consider additional downgrades.

That all sounds tremendously uncertain, even for these uncertain times. Carnival’s Princess line has already canceled some early 2021 world voyages, and its Cunard line said it would extend its pause in operations until next year. The fact that the bonds are nonetheless rallying suggests investors are willing to set aside their trepidations — as long as yields remain significantly above what current credit ratings would indicate.

Remember that just a few weeks ago, Ball Corp., a junk-rated aluminum-packaging company, sold $1.3 billion of 10-year securities at 2.875%, the lowest ever for U.S. speculative-grade debt with a maturity of longer than five years. Yes, coronavirus lockdowns are causing a can shortage, which would obviously benefit a chief producer of aluminum drink cans. But that’s still a stunningly low interest rate for debt billed as high yield. If Moody’s says the cruise lines are sound for at least the next year or so, why not clip a double-digit coupon and see whether America and the rest of the world can rein in Covid-19?

Meanwhile, high-yield credit spreads are close to the narrowest since before the pandemic escalated, even after August proved to be the second-busiest month for junk-bond sales in history. The relentless rally is opening up the possibility that September may bring up to $40 billion in new offerings. Few borrowers are likely to offer the mix of relatively high yields and major industry-leader positions as the cruise lines.

Betting on a successful comeback for cruises, after almost half a year working from home and just in the wake of a Moody’s superdowngrade, might not feel too secure. But for fixed-income investors, a sufficiently high yield can assuage just about any fear. In the case of Carnival and Royal Caribbean, that should be enough to continue buoying their bonds.

According to Moody's, Carnival isthe largest worldwide cruise line in terms of revenue, fleet size and number of passengers carried, whileRoyal Caribbean is the second largest global ocean cruise operator based upon capacity and revenue.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.