Don’t Be Fooled, There's Pain Headed to Stocks From Debt Markets

Credit Weakness Boosts Case to Own Quality, Bernstein Quants Say

(Bloomberg) -- Equity investors will have to focus “a lot more” on corporate credit this year and should avoid chasing recent gains for companies with weak credit ratings as spreads widen, according to quantitative strategists at Sanford C Bernstein Ltd.

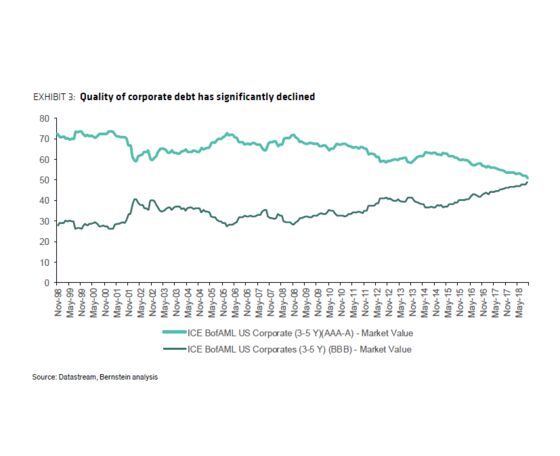

The highest-quality credits, those rated A3 and above, currently represent only half of large-cap equities in the U.S. and Europe, compared with 90 percent two decades ago, Bernstein’s quants found.

“We have simply never before seen a corporate sector with such low-grade debt,” analysts including head of global quantitative and European equity strategy Inigo Fraser Jenkins wrote in a note Wednesday. “The deterioration in the quality of credit means, we think, that credit spreads have a lot further to expand this cycle.”

Bernstein says recent strength in stocks with weak balance sheets is an opportunity to sell and recommends buying stocks with stronger creditworthiness instead, preferring that measure of quality to other factors such as high profitability, which have been bid up, the note said.

Quality stocks have trailed their value counterparts this year amid a wider rally for global equities as the Federal Reserve signals a possible deceleration in the pace of its balance sheet run-off. The MSCI World Quality Index has risen 4.6 percent, versus gains of 5.7 percent for a gauge tracking value stocks.

A narrowing of CDS spreads during the past month and outperformance for stocks with low quality credit ratings is a “fundamental misreading of the situation,” the note said. “Recent strength of bad credit quality stocks is an opportunity to sell.”

Owning low credit-quality-stocks has generated higher returns during the quantitative-easing era, Bernstein said, especially in U.S. markets where corporates became a bigger buyer of equities in recent years than asset managers. Quantitative tightening should be a catalyst for higher-quality companies to outperform.

“Having high leverage was rewarded in a market supported by QE, not least because buybacks expanded,” the strategists wrote. “Times are now changing.”

To contact the reporter on this story: Gregor Stuart Hunter in Hong Kong at ghunter21@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Joanna Ossinger, Ravil Shirodkar

©2019 Bloomberg L.P.