Bad Credit Card Debt Is on the Rise

Bad Credit Card Debt Is on the Rise

(Bloomberg) -- Red flags are flying in the credit-card industry after a key gauge of bad debt jumped to the highest level in almost seven years.

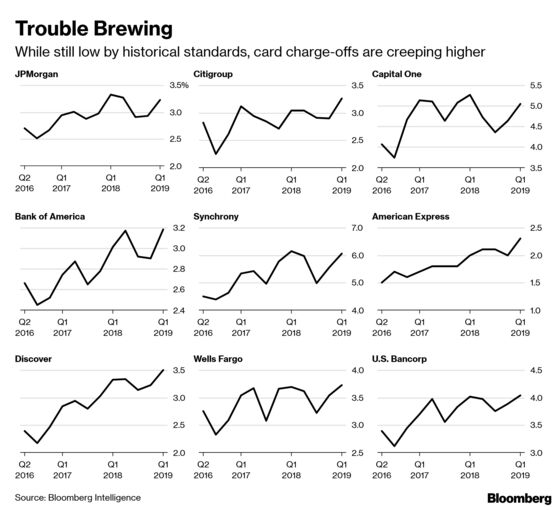

The charge-off rate -- the percentage of loans companies have decided they’ll never collect -- rose to 3.82 percent in the first three months of 2019, the highest since the second quarter of 2012, according to data compiled by Bloomberg Intelligence. And loans 30 days past due, a harbinger of future write-offs, increased at all seven of the largest U.S. card issuers.

There’s been a “degradation” in credit quality for certain customers, according to Richard Fairbank, chief executive officer at Capital One Financial Corp., the country’s third-largest card issuer. Fairbank said some customers with negative credit events during the financial crisis are now seeing those problems disappear from their credit-bureau reports.

“We may be looking at data that might not paint the full picture of a consumer’s credit history,” Fairbank said Thursday on a conference call with analysts. “Part of the context for our caution has been not only how deep we are in the cycle but, also, this is the time period when there is less information than there once was.”

Capital One said Thursday that its first-quarter U.S. card charge-off rate climbed to 5.04 percent from 4.64 percent at the end of 2018. At Discover Financial Services, which also reported results on Thursday, the charge-off rate increased to 3.5 percent from 3.23 percent in the prior quarter.

“Certainly, this has been one of the longest recoveries, so, in general, we have been contracting credit policy at the margin and tightening,” Discover CEO Roger Hochschild said in an interview. Hochschild said his company has been closing inactive accounts and slowing down the number and size of credit-line increases for both new and existing customers.

The industry’s latest warnings build on developments in January, when fourth-quarter results showed charge-off rates near the lowest in decades were coming to an end. Competition for the highest-quality customers remains fierce, leading many issuers to spend more on marketing and rewards to gain market share with that group. But a growing wariness about the potential for a rise in bad debt has led many issuers to tighten underwriting.

To be sure, charge-offs remain not far from historic lows as banks benefit from low unemployment rates in the U.S. And Capital One on Thursday surged 4 percent in New York trading after telling investors that its efficiency ratio, a key profit metric that measures how much it costs to produce a dollar of revenue, would improve to 42 percent by 2021 as it closes data centers and migrates its systems to cloud computing.

“If you think about lending products, there are always people who want to take your money,” Hochschild said. “You’re going for people who have many choices -- they have existing cards, they could get any card they want. So our job is to make sure those are the ones we attract to Discover.”

To contact the reporter on this story: Jenny Surane in New York at jsurane4@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, Steve Dickson, Daniel Taub

©2019 Bloomberg L.P.