(Bloomberg Opinion) -- Like a lot of countries in East and Southeast Asia, Thailand has done a pretty spectacular job of controlling the coronavirus pandemic. There have been just 3,446 confirmed cases of the disease, and 58 deaths, in a country of nearly 70 million inhabitants. Its per-capita Covid-19 death toll is less than one-seven-hundredth that of the U.S.

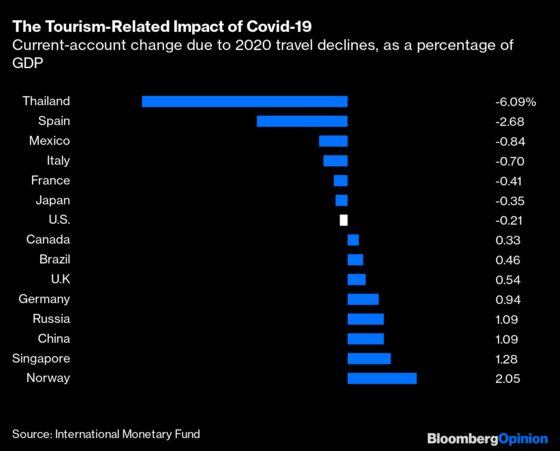

This hasn’t spared Thailand from an economic downturn that appears to be significantly worse than the one facing its neighbors, or the U.S. That’s mainly because Thailand’s economy depends heavily on tourists from abroad, whom it has prevented from entering the country since early in the pandemic and is only now beginning to allow back in under extremely restrictive conditions. In a recent analysis of the Covid-19 tourism bust’s impact on the current-account balances of 52 countries, the International Monetary Fund concluded that Thailand will be hit the hardest. Here are the IMF’s estimates for 15 of those countries.

The current account measures trade in goods and services plus cash transfers. The countries with the biggest negative numbers in the above chart normally export a lot more tourism services than they import, and Covid-19 has sharply reduced that tourism-trade surplus. Others taking especially big hits include Greece, at -5.9% of gross domestic product, Portugal,-4.45%, Morocco, -3.64%, and Costa Rica, -3.38%.

Thinking of tourism in terms of trade balances can be a little confusing at first. Countries that bring in more tourists than they send abroad are actually exporting more tourism services than they import, and thus running a tourism surplus. Countries that send huge numbers of people abroad in search of sun and other attractions and welcome smaller numbers of visitors are net importers of tourism. By halting or slowing travel, the pandemic has thus reduced their tourism trade deficits.

As my fellow Bloomberg Opinion columnist Noah Smith explained a few years ago in response to some silly things said by Trump administration trade adviser Peter Navarro, the fact that trade deficits show up as negative numbers in GDP accounting and surpluses as positive does not necessarily mean that reducing the former or increasing the latter will increase growth. But in this case the short-term economic impacts are probably more or less as described in the chart. Having to do without the spending of foreign tourists is in fact sharply reducing Thailand’s GDP. And in Norway, having its inhabitants spend money at home that otherwise would have been spent in Marbella or Phuket is probably boosting GDP somewhat — albeit in the face of lots of other forces, such as the fall in oil prices, that have driven it downward.

In Europe, where wealthier northern countries usually send lots more tourists to poorer southern countries than they get back in return, this means the pandemic has exacerbated the continent’s north-south economic imbalances. The 750-billion-euro ($885 billion) stimulus package that the European Union agreed to in June, which delivers its biggest benefits to Italy and Spain, thus seems like the right kind of response, if perhaps not a big enough one.

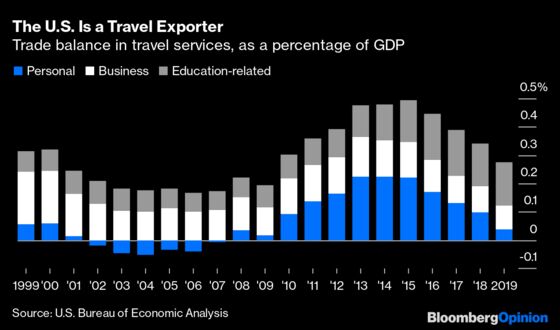

The U.S. is not poor or particularly southern, but it too is among the countries that get more money from foreign visitors than their residents spend abroad.

This trade surplus is not huge, and most of it comes not from tourists but from business travelers and foreign students studying at colleges and universities here. The U.S. is no Thailand. But it does garner clear economic benefits from cross-border travel — meaning that a pandemic or anything else that discourages such travel is bad news.

It does this in Figure 1.10 in Chapter 1, in case you want to look it up yourself.

It is of course the spending by tourists, not the number of tourists, that determines the trade balance, but I thought it was easier (and generally accurate) to describe in terms of flows of people.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Justin Fox is a Bloomberg Opinion columnist covering business. He was the editorial director of Harvard Business Review and wrote for Time, Fortune and American Banker. He is the author of “The Myth of the Rational Market.”

©2020 Bloomberg L.P.