Corporate Bond Market's Merger Fever Leaves Some Buyers Cold

Corporate Bond Market's Merger Fever Leaves Some Buyers Cold

(Bloomberg) -- U.S. blue-chip companies that have been waiting for the right time to tap the bond market to fund their acquisitions are starting to pull the trigger. Unfortunately for them, investors are showing some signs of getting warier.

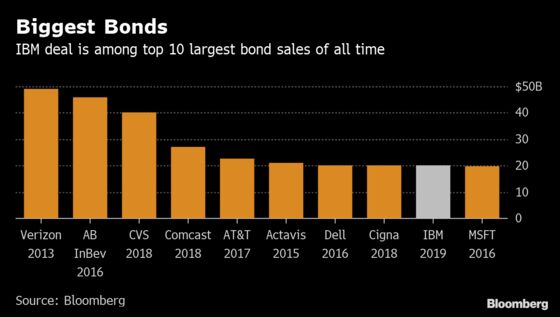

International Business Machines Corp. and Bristol-Myers Squibb Co. both sold about $20 billion of bonds this week to fund acquisitions. Companies including 3M Co., Fidelity National Information Services Inc., T-Mobile USA Inc. and Anadarko Petroleum Corp.’s ultimate buyer are among the corporations expected to issue bonds to finance takeovers.

They’re issuing debt in part because it’s around the cheapest it’s been in more than a year and investors have been pumping billions of dollars of cash into the market. The average high-grade company bond yielded 3.6% on Wednesday. The debt has gained around 5.7% this year, helped by issuance having fallen.

But this week’s deluge of offerings may also scare off investors. IBM got orders for less than twice the bonds it had for sale, when big issuers often get three times as many or more. In June 2018, Bayer AG borrowed $15 billion to help fund its acquisition of Monsanto Co. Days later, Walmart Inc. sold $16 billion of corporate bonds to fund its acquisition of a stake in Flipkart. New issuance volume was weak for weeks afterward.

Other factors may also weigh on demand for corporate bond offerings that investors expect in the coming weeks, such as T-Mobile and Fidelity National Information Services. U.S. stocks have been falling amid escalating trade tensions. When the U.S. Treasury auctioned benchmark 10-year notes on Wednesday, it found the weakest demand in a decade, illustrating the diminishing appetite among some investors to accept current yields. Companies that are selling bonds now may be looking to borrow before things get worse.

“There’s building uncertainty as to the economic outlook, so it’s good to get the money while the getting’s good,” said David Knutson, head of credit research for the Americas at Schroder Investment Management.

Companies are funding acquisitions in the bond market again after a slow start to 2019. Just over $60 billion of investment-grade corporate debt was sold for that purpose in the first four months of the year, including $2 billion in April, according to data compiled by Bloomberg. That’s out of $445.4 billion of total issuance. Companies instead focused on selling bonds to refinance maturing securities and fund capital expenditure, among other corporate uses.

What Bloomberg News Strategist Brian Smith says“While IBM set a record with size, it struggled to find the successful execution Bristol-Myers achieved. IBM paid 5-10 basis points in new-issue premium on the back of an order book that was 1.75 times covered while Bristol-Myers priced through its credit curve and was 3.5 times oversubscribed.” Read more |

Late last year, money managers grew increasingly alarmed about the high percentage of investment-grade companies in the BBB tier, leaving them just a few steps above junk. Many of these companies ended up with relatively low credit ratings through acquisitions funded with relatively cheap debt.

“The whole market started to think more about later stages of the economic cycle and how impactful carrying large debt burdens is going to be if the economy does deteriorate,” said Josh Lohmeier, head of U.S. investment-grade credit at Aviva Investors, which manages more than $420 billion.

Demand for this week’s bond offerings was relatively strong and dealer inventories are up by $1.4 billion, which is less than one might expect, according to strategists led by Hans Mikkelsen at Bank of America Corp. The bank anticipates that trade concerns will fade and corporate bond risk premiums will narrow well into the summer.

But if economic growth ends up slowing, companies could be in for a reckoning, said Steve Eisman, the Neuberger Berman Group money manager who famously predicted the collapse of subprime mortgages before the 2008 financial crisis.

“You will see big losses in things like triple-B corporate debt, high-yield etcetera, but you need a recession first,” Eisman said. “Corporate debt isn’t going to cause the next recession, but it’s where the pain will be in the next recession.”

To contact the reporters on this story: Natalya Doris in New York at ndoris2@bloomberg.net;Molly Smith in New York at msmith604@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins

©2019 Bloomberg L.P.