Corporate America Goes on Debt Diet After $3 Trillion Binge

U.S. companies are finally listening to stock and bond investors that have been pressing corporations to cut their debt loads.

(Bloomberg) -- U.S. companies are finally listening to stock and bond investors that have been pressing corporations to cut their debt loads.

General Electric Co. is selling its biopharmaceutical business to Danaher Corp. for more than $21 billion, and using the money to pay down borrowings. Kraft Heinz Co. said last week it was slashing its dividend and using the proceeds of asset sales to reduce its liabilities.

Randall Stephenson, AT&T’s chief executive officer, said last month that the company’s top priority in 2019 is to lower its debt. Plans like these are good news for bondholders who have spent years watching these companies borrow ever more to finance moves like acquisitions that are designed to boost share prices, said Brian Kennedy, a senior portfolio manager at Loomis Sayles & Co.

“They’re in credit repair mode and going full force at this,” said Kennedy, whose firm managed around $250 billion at the end of December.

The steps that companies are taking could mean that the credit meltdown that many banks and investors are bracing for -- JPMorgan Chase & Co. said on Tuesday that its lending growth should slow as a recession grows more likely -- will be relatively tame. Investors have grown more confident that any credit downturn will be mild, with U.S. junk bonds on track for their best performance for the first two months of a year since 2001.

Stock and bond investors often pressure a company in different directions: equity money managers usually want more risk taking and borrowing to improve profit growth. Debt investors typically press for more measured growth and fewer share buybacks, to ensure that cash flow remains strong relative to debt obligations. But that’s changing, said Tom Murphy, head of investment-grade credit at Columbia Threadneedle Investments, which oversees around $431 billion of assets.

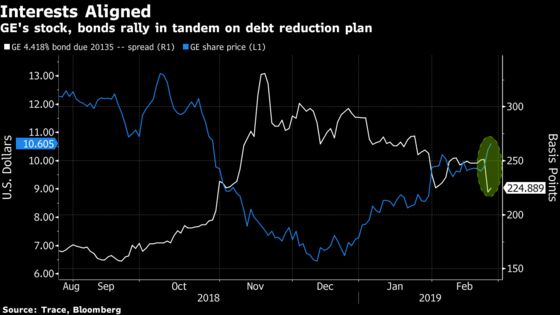

“Now the interests are much more aligned,” Murphy said. “It’s about generating profitable growth, not growth for growth’s sake.” When GE announced its asset sale to pay down debt on Monday, its shares jumped and risk premiums on its bonds narrowed.

Repairing credit may be overdue. There’s more than $5.2 trillion of U.S. investment-grade corporate bonds outstanding, according to data compiled by Bloomberg, a figure that has grown by more than $3 trillion over the last decade. As debt has grown, it’s become riskier: around half of blue-chip corporate bonds are in the tier just above junk, while in the early 1990s that level was closer to 27 percent.

The bonds at that tier are relatively low quality by at least one measure. More than half of the BBB U.S. and European companies have debt levels relative to a measure of earnings that would be more appropriate for junk than high-grade companies, strategists at JPMorgan Chase led by Nikolaos Panigirtzoglou in London wrote in December. Distressed debt investors from Avenue Capital’s Marc Lasry to Bruce Richards at Marathon Asset Management have warned of risks to investment-grade companies with high levels of debt.

Equity Caution

It’s not just debt investors that are alarmed. Equity investors have been flocking to companies with less debt on their balance sheet, and money managers including JPMorgan Asset Management and Northern Trust Asset Management have touted high-quality stocks to buffer against possible market meltdowns. Shares of U.S. companies with strong balance sheets are close to their highest valuations relative to weaker peers since 2003, according to Goldman Sachs Group indexes.

Some companies are acknowledging they need to tame their debt piles to improve their growth prospects. AT&T’s $171 billion debt load is making it harder for it to cut prices to compete, hindering its hanging onto customers in areas like cell phone service. Competitor Verizon Communications Inc. has been actively taming its $113 billion debt pile, most recently lowering its leverage target. It aims to regain a single A rating.

“Telecom is the poster child right now for balance sheet religion,” Michael Temple, director of U.S. credit research at Amundi Pioneer, said on Bloomberg TV this month. “They are clearly focusing on deleveraging, and AT&T being one of the largest issuers, has clearly been given the mandate. Rating agencies are hovering over everybody as we speak, and saying ‘get it down, get it down.”’

When Kraft Heinz posted its quarterly results last week, most investors focused on its $15.4 billion goodwill writedown and a decline in a key measure of earnings. But the company also said that it’s cutting its annual dividend by 36 percent, a step that frees up $1.1 billion in cash flow a year. The proceeds from the sale of its India beverages and Canada natural cheese business, and future asset sales, will pay down debt. The company, which had more than $31 billion of borrowings on its books at the end of 2018, now sees more urgency in cutting debt and refinancing debt maturing in the near term, Chief Financial Officer David Knopf said last week.

GE CEO Larry Culp called his company’s sale of its biopharmaceutical business, and the attendant paydown of debt, a “pivotal milestone” on Monday. Credit investors cheered the move, and the cost to insure against a GE default dropped to the lowest in four months. The next day, Culp told investors in his first annual shareholder letter that cutting debt is a top priority in turning around the company.

It all adds up to make 2019 the year of the “debt diet,” said Peter Tchir, head of macro strategy at Academy Securities, said on Bloomberg TV this month.

“This is really a year that corporations are going to focus on their debt,” Tchir said. “That will actually be good for stock prices. And that’s why they’re doing it.”

To contact the reporter on this story: Molly Smith in New York at msmith604@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins, Sally Bakewell

©2019 Bloomberg L.P.