U.K. Housing Is a Sick Canary in the Economic Coal Mine

(Bloomberg Opinion) -- In any league table of institutions with the keenest view of what’s happening in a local economy, banks should be ahead of the pack. So the fact British lenders are starting to exhibit a lack of faith in the U.K. housing market is a worrying barometer of how fragile the economic outlook is becoming.

Fault lines are widening. Figures published on Tuesday showed the pandemic has already wiped out almost 700,000 jobs. Some 2.7 million Britons are claiming jobless benefits, an increase of 121% since March. And escalating tension with the European Union over Brexit has increased the chances of the U.K. leaving the bloc without a trade deal, posing the danger of a chaotic change in the rules governing the relationship with Britain’s biggest export market for businesses already trying to cope with the repercussions of the pandemic.

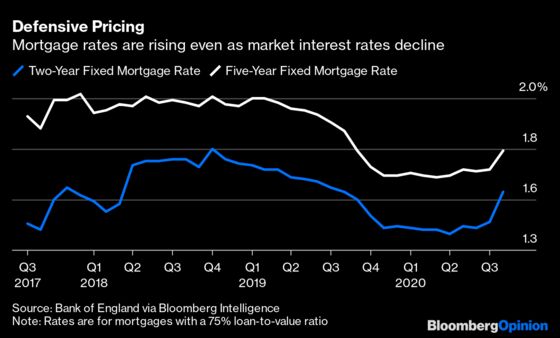

The prospect of the end to the government’s furlough support next month means unemployment will worsen, making it harder for people to pay their mortgages and other household bills. To defend themselves, mortgage providers are cranking up the rates they charge on home loans.

The figures in the chart above relate to home loans where the house is worth at least 25% more than the amount borrowed, known as the loan-to-value ratio. But that’s only part of the picture. Moneyfacts, a consumer data company, reckons that this month, across the entire LTV range including loans much closer to the house price, two-year fixed rates have posted their biggest jump since July 2009.

Lenders are seeking to protect themselves from a worsening economic downturn in other ways as well. The overall number of mortgage products on offer has contracted by a staggering 54% since March, Moneyfacts estimates, while the average fee charged for arranging a home loan has risen to its highest level since February 2013.

U.K. banks are clearly pulling back from the mortgage market.

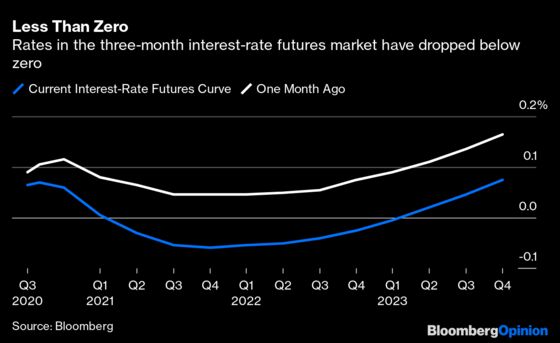

This trend had nothing to do with market participants anticipating higher interest rates from the Bank of England as might usually be the case outside of a global pandemic. Last week, for the first time ever, investors were willing to pay for the privilege of lending to the U.K. government for six months. The Debt Management Office got the Friday bill auction away at an average yield of minus 0.0005%, the first negative yield at an offering of that maturity.

Two-year gilt yields, meantime, declined to a record -0.16% last week. And in the interest rate futures market, the levels on three-month contracts expiring in the coming quarters have posted a significant drop below zero in the past month.

That backdrop makes it all the more important that Chancellor of the Exchequer Rishi Sunak, who’s done a good job in protecting workers since the economy went into lockdown, get his next moves right. He’s currently planning an October end to paying the bulk of wages for workers furloughed by their employers, in contrast with lengthy extensions to similar programs from European neighbors including Germany, Italy and France. Halting that support at such a crucial juncture would be a mistake.

The message from both the money markets and the mortgage market suggests fiscal support is still essential. The British government needs to perform yet another U-turn to avoid a second downturn in growth in the months ahead.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2020 Bloomberg L.P.