(Bloomberg Opinion) -- Here’s a trivia question: Who said this, and when?

“There is some evidence of reach-for-yield behavior. That’s one of the reasons I mentioned that this environment of low volatility is very much on my radar screen and would be a concern to me, if it prompted an increase in leverage or other kinds of risk-taking behavior that could unwind in a sharp way and provoke a sharp, for example, jump in interest rates. And we've seen what effect that can have on the global economy, and I think it’s something that is important to avoid.”

If you said Federal Reserve Chair Janet Yellen in June 2014, give yourself a round of applause.

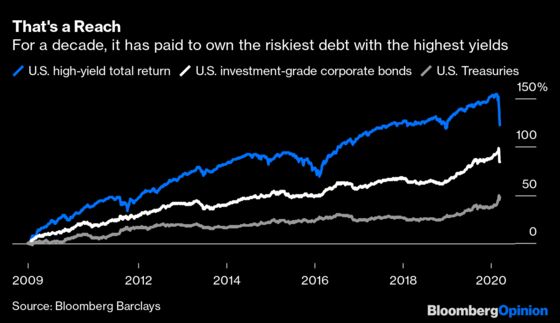

I bring up this six-year-old quote because “reaching for yield” has been arguably the defining characteristic for investors in the $100 trillion global bond market since the end of the last recession. The Bloomberg Barclays U.S. Corporate High Yield Index delivered annual returns of 9.2% from June 2009 through last month. By comparison, investment-grade company debt gained an average 6.5% annually while U.S. Treasuries earned 3.5%. Even during tough stretches — the oil price collapse in 2014 and 2015 that roiled risky energy companies, or the “retailpocalypse” — there always seemed to be a feeling that taking more risk would ultimately pay off. Defaults and downgrades would remain low and could be easily sidestepped with a bit of research.

A couple of cases in point. In a Jan. 27 report, Moody’s Investors Service predicted that the speculative-grade default rate would fall back to 3.5% by the end of this year as strains in energy and retail moderate. In Bank of America Corp.’s 2020 outlook, strategists wrote that “the 11-year high-yield credit cycle is expected to keep on rolling,” with defaults stabilizing at 4%. This was more or less the consensus view. The Bloomberg News headline for top credit calls of 2020? “Don’t Give Up on Riskiest Corporate Debt.”

All this, of course, came before the escalating coronavirus outbreak caused entire regions across the globe to grind to a halt. The expert advice in this new reality is precisely the opposite: Get out of the riskiest debt if you still can.

Since the high-yield index peaked on Feb. 20, it has declined 12.7%, a stunningly sharp drop the likes of which hasn’t been seen since Oct. 29, 2008. The latest oil-price crash certainly plays a role — the average spread on junk bonds in the energy sector hit a record high 1,924 basis points this week, and year-to-date they’ve lost almost 36% — but no industry has held up. The spread on the high-yield index excluding energy bonds surged 96 basis points on Monday, the biggest jump since Bloomberg began tracking daily moves in 2015. Now at 722 basis points, it’s just 17 basis points from breaching its February 2016 high.

I could go on with superlatives. But suffice it to say, investors are fleeing the riskiest corners of the bond market. And this time, even with the loftiest yields in a decade, it doesn’t seem all that likely that the securities will bounce back quickly.

It’s no secret why bond traders are squeamish about stepping into the sell-off. Wall Street economists are growing more convinced that the coronavirus has triggered a global recession, with those at Goldman Sachs Group Inc. and Morgan Stanley just the latest to turn from the question of whether there will be a downturn to just how bad it could get. In no uncertain terms, that’s the worst-case scenario for investors holding debt from the riskiest companies.

The scariest part harks back to one word from Yellen’s quote: Leverage.

It’s well known that the amount of triple-B rated corporate bonds is now roughly $3 trillion, up from $800 billion at the end of the last recession, as companies seized upon cheap borrowing costs and boosted their leverage ratios. If the world does tip into a recession, that ought to be enough for at least a fraction of that much-watched powder keg to blow. Finance officers pledged to go on a “debt diet” last year, but they probably expected to have a bit more time to slim down.

“If the gods wanted to put together the perfect storm for the corporate-bond market, they’ve done it,” Jeffrey Gundlach, DoubleLine Capital’s chief investment officer, said Tuesday in a webcast. In addition to the coronavirus and oil price shock, he cited years of yield starvation driving demand and issuance, while dealers no longer have the wherewithal to take down the securities during periods of stress. He expects downgrades “coming fast and furious.”

That’s to say nothing of the even riskier corners of debt markets. Leveraged-loan prices have plunged to levels last seen in 2009, and virtually no new deals are pricing during the collapse. That’s an ominous sign, given how desperately some of these companies need market access to survive. As for private credit, there’s already speculation that funds may need to wind down, particularly smaller ones that can’t inject more money into companies to weather the impending slowdown.

All of this reminds me of following up on a New York Times op-ed from Ruchir Sharma, chief global strategist at Morgan Stanley Investment Management. He argued in June that a swarm of “zombie firms” propped up by ultra-low borrowing costs and excessive risk-taking posed a serious threat to the economy. “To assume that central banks can hold the next recession at bay indefinitely represents a dangerous complacency,” he wrote.

That assumption is crumbling before our eyes. The Fed has tapped its entire toolbox from the last crisis, including Tuesday’s announcement that it was using emergency authorities to restart the crisis-era Commercial Paper Funding Facility. It sounds more likely by the day that the Trump administration will provide some sort of direct payment to Americans to bridge this turbulent time. Risk assets seemed to appreciate the support, but one day in the green is hardly a cure-all.

Sharma was back this week with a new op-ed titled “This Is How the Coronavirus Will Destroy the Economy.” It centers on the same firms he discussed nine months ago. “The longer the pandemic lasts, the greater the risk that the sharp downturn morphs into a financial crisis with zombie companies starting a chain of defaults just like subprime mortgages did in 2008,” he wrote.

There may yet be time to prevent this dire scenario, but the window is closing fast. At the very least, the severe losses in risky debt are a painful reminder that reaching for yield will eventually come home to roost. Investors had become so comfortable with the status quo that some suggested in January that the days of a boom-and-bust economic cycle were over.

The bust is coming. Like recession forecasts, the only question now is how bad it will get.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.