Commodities Hammered in China by Virus-Driven Demand Fears

Metals, energy and agriculture futures were all hammered.

(Bloomberg) -- Chinese commodity prices collapsed on the first day of trading after the Lunar New Year break as investors returned to markets gripped by fear over the impact the coronavirus will have on demand in the world’s biggest consumer of raw materials.

The country’s three major commodity exchanges were hit by a fevered bout of selling as they reopened with Chinese traders getting their first opportunity to catch up with losses inflicted on overseas markets while they had been on holiday.

Metals, energy and agriculture futures were all hammered, with iron ore, crude, copper and palm oil contracts all sinking by their daily allowable limit within seconds of markets opening. Shares in commodity also producers tumbled as stock markets resumed trading.

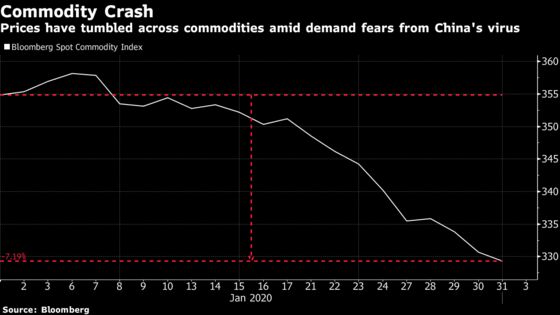

Investors have deserted raw materials around the world from copper in London to palm oil in Kuala Lumpur over fears about the economic fallout from the virus. More than a dozen Chinese provinces have announced an extension of the new year holiday by more than a week in a bid to halt the spread of the virus that has killed hundreds of people and sickened thousands.

“Investors are fleeing from commodities and seeking risk-aversion assets,” said Chen Tong, an analyst with Tianjin-based First Futures. “Everything from consumption to logistics has stagnated with 30 Chinese provinces and regions announcing the highest level of public health emergency and so the market is basically bearish across the board.”

By the 3 p.m. close of trading, iron ore was 6.6% lower at 606.50 yuan a ton, the weakest since November. Steel reinforcement bar closed down 7.6% after opening at its downside limit. Domestic oil futures saw the biggest decline since their debut in March 2018 while copper dropped 6.2% and palm oil by 6.9%. Markets won’t reopen until Tuesday morning after China canceled overnight trading.

The sell-off on commodities exchanges was repeated across China’s financial markets, with stocks plummeting by the most since an equity bubble burst in 2015. Bond yields dropped the most since 2014 and the onshore yuan weakened below the key 7-per-dollar level.

The mainland-traded shares of Chinese companies that mine, refine and smelt the nation’s raw materials weren’t spared the rout. Jiangxi Copper Co., the biggest copper smelter, tumbled by its daily limit of 10% in Shanghai, while Baoshan Iron & Steel tumbled 9.9%. PetroChina Co., its biggest energy company, lost 9%.

Authorities have pledged to provide abundant liquidity and urged investors to evaluate the impact of the coronavirus objectively. The central bank on Monday reduced rates as it injected cash into the financial system.

Investors are nonetheless spooked about the impact of the virus on growth as swathes of the country are locked down. Bloomberg Economics estimated growth could slump to 4.5%, the lowest in quarterly data going back to 1992.

For raw materials, regions accounting for about 90% of copper smelting, 60% of steel production, 65% of oil refining and 40% of coal output have told firms to delay restarting operations until at least Feb. 10.

Fears over the effect that’s going to have on demand and supply balances had hammered global prices while Chinese markets were shut. Brent crude tumbled about 6% and Singapore’s iron ore contract lost almost 11% during the new year holiday, while copper on the London Metal Exchange capped its worst month since 2015. Malaysian palm oil last week fell the most since 2008.

Traders are looking for any signs of how the virus will impact demand and the flow of commodities in to and out of the country. Chinese oil demand has already dropped by about three million barrels a day, or 20% of total consumption, as the coronavirus squeezes the economy, according to people with inside knowledge of the country’s energy industry.

The drop is probably the largest demand shock the oil market has suffered since the global financial crisis of 2008 to 2009, and the most sudden since the Sept. 11 attacks. China is the world’s largest oil importer, so any change in consumption has an outsize impact on the global energy market.

China is also the biggest producer of refined copper and steel, and imports two-thirds of the world’s seaborne iron ore. Its share of global base metals demand exceeded 50% in the first 10 months of last year, from less than 20% during the SARS crisis, Bloomberg Intelligence estimates.

While Chinese metals markets tanked on Monday, some contracts on the London Metal Exchange rebounded, with copper rising for the first time in 14 days.

And losses weren’t universal across China’s commodity markets. Bullion on the Shanghai Gold Exchange advanced 2.5%, while thermal coal escaped the massive sell-off as traders weighed extended mine shutdowns due to the virus outbreak.

--With assistance from Krystal Chia, Winnie Zhu and Andrew Janes.

To contact Bloomberg News staff for this story: Sarah Chen in Beijing at schen514@bloomberg.net;Alfred Cang in Singapore at acang@bloomberg.net

To contact the editors responsible for this story: Will Kennedy at wkennedy3@bloomberg.net, Anna Kitanaka, Alexander Kwiatkowski

©2020 Bloomberg L.P.

With assistance from Bloomberg