CLOs Split Wall Street Over Whether It's Time to Buy or Bail

CLOs Split Wall Street Over Whether It's Time to Buy or Bail

(Bloomberg) -- As demand for one of Wall Street’s hottest fixed-income products cools, money managers are divided over whether it’s time to bow out or go bargain hunting.

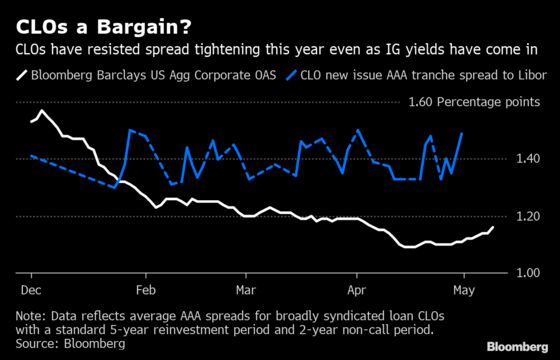

Collateralized loan obligations are one of the few assets classes that have largely resisted spread tightening in 2019. After reaching about 141 basis points over the London interbank offered rate at the end of last year, the average pickup for new issue AAA rated tranches has remained in a tight range ever since. In contrast, yields on high-grade corporate bonds have tightened 39 basis points, while those on top-rated commercial mortgage securities have narrowed 28 basis points, according to data compiled by Bloomberg and JPMorgan Chase & Co.

The growing debate over CLOs -- which bundle risky debt into new floating-rate securities -- is a key part of fund managers’ efforts to reposition as the Federal Reserve signals its intent to keep interest rates on hold for the foreseeable future. Some say an overweight allocation to fixed-coupon corporate and mortgage bonds makes the most sense in a stable rate environment. Others cite the sheer spread advantage of CLOs as reason enough to pile in.

CLOs have “become this great relative-value proposition, especially with the tightening in other areas of the credit markets,” said Laila Kollmorgen, a Los Angeles-based portfolio manager at PineBridge Investments. “What you’ll find is people are reassessing their portfolios.”

CLO issuance reached a record $130 billion in 2018 as investors sought out floating-rate debt with higher yields. Yet some money managers began to flee the asset class at the start of the year, chasing interest-rate duration in fixed-rate bonds, which rallied in the first quarter.

“Duration is back in vogue,” said Rishad Ahluwalia, head of CLO research at JPMorgan. “If the economy starts to weaken and inflation remains low, investors likely want to be in duration. You might see more of an increasing shift to a reallocation to fixed-rate products, depending on how things evolve.”

In fact, with the Fed’s tightening cycle showing little sign of resuming anytime soon and the Treasury curve inverting for the first time since March this week, floating-rate paper like CLOs may be out of favor for some time, he said.

Others say not so fast.

Lower-rated CLO slices have begun to outperform corporate bonds over the past couple weeks for the first time this year. Even AAA tranches have tightened slightly in secondary-market trading.

“Up and down the CLO capital structure remains very attractive,” said Tom Majewski, managing partner of Eagle Point Credit Management.

He cites the average BB tranche paying roughly 400 basis points more than high-yield bonds, and the AA class -- which has never defaulted in the history of the CLO market -- offering about 100 basis points versus an index of high-grade notes as compelling valuations.

Turning the Corner

Wider relative CLO spreads this year along with higher prices on underlying loans have damaged the so-called CLO arbitrage, or gap between the money brought in from the loans and the cost of borrowing for a CLO manager. This makes it less profitable for managers to form new CLOs. While issuance has remained robust to start 2019, the pace is likely to slow as a result, according to analysts.

CLO creation is also expected to wane due to a scarcity of underlying leveraged loans. Loan issuance has totaled less than $130 billion year-to-date, well off last year’s pace.

Less primary-market CLO supply should support further spread tightening, Bank of America Corp. analyst Chris Flanagan wrote in a note to clients.

“Some are not confident that being completely in fixed-rate products over the next few months is where they want to be,” PineBridge’s Kollmorgen said. “The so-called ‘greed factor’ kicks in -- the relative value of CLOs is too good to pass up.”

--With assistance from Charles Williams.

To contact the reporter on this story: Adam Tempkin in New York at atempkin2@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Boris Korby, Rizal Tupaz

©2019 Bloomberg L.P.