CLO Managers Offer Disaster Protection to Help Sell Bonds

CLO Managers Offer Disaster Protection to Help Sell Their Bonds

(Bloomberg) -- Money managers that bundle leveraged loans into securities are offering a type of disaster hedge to the increasingly uneasy buyers of their bonds.

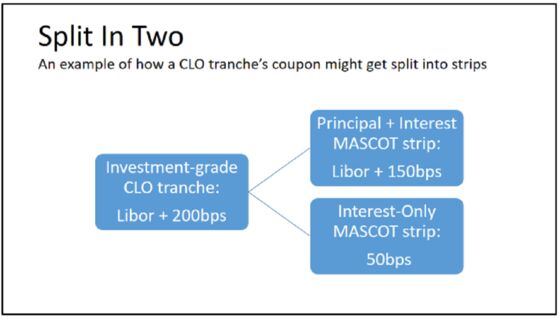

Asset managers that sell securities known as collateralized loan obligations are subdividing them into parts, including one that only pays interest and another that mainly pays principal. These instruments can help protect investors against big drops in credit markets. Credit Suisse, as arranger of these securities, has put together these deals for asset management firms including Rothschild & Co. and Greg Lippmann’s LibreMax Capital.

“It’s attracted investors that might not have looked at CLOs,” said Tom Majewski, founder and managing partner at Eagle Point Credit Management.

The Swiss bank’s efforts underscore how firms have been forced to get more creative to sell CLOs, as the Federal Reserve has stopped lifting rates, and may even be ready to start cutting. The securities pay floating interest rates, and a central bank on pause means investors won’t get to benefit from higher payments. Credit Suisse declined to comment, while LibreMax and Rothschild didn’t respond to requests for comment.

Disaster protection makes sense to some investors that are increasingly antsy about credit markets. Companies have been taking on more debt relative to their assets and income, and around half of investment-grade U.S. corporate bonds are now in the tier just above junk, compared with around a quarter in 1993. Scott Mather, chief investment officer of U.S. core strategies at Pacific Investment Management Co., said last month that “We have probably the riskiest credit market that we have ever had.” U.S. and European regulators have cautioned about the loans to junk-rated companies that get bundled into CLOs.

Credit Suisse’s split CLOs are similar to instruments known as “strips” that Salomon Brothers and other banks created for mortgage bonds and Treasuries in the 1980s. In this case strips are created by taking the safest portions of CLOs and splitting them into two: one instrument that pays only interest, and another that pays a little interest and mostly principal. The investor then has the option to exchange the original security for any combination of the strips whenever he or she wants.

Managers have been using other tactics to sell CLOs this year. For instance, in the first quarter more than 25% of CLOs were sold with shorter or static maturities, compared with only 10% for the same period last year, Fitch said in a report last month. Investors like shortened risk horizons and hence such strategies reduce the cost of funding for the manager.

Each of those can help CLO investors manage risk, but the interest-only portion may be the most helpful in a downturn. The IOs become much more valuable if credit markets tank and CLO risk premiums -- the extra yield they pay over benchmark rates -- jump.

The portion that’s mainly principal can become more valuable if risk premiums, or credit spreads, narrow. That’s attractive to investors looking to hedge a risk known as negative spread convexity: when investors grow less worried about companies defaulting, CLOs benefit less than a typical corporate bond, because their risk premiums narrow less.

Some Skeptical

Credit Suisse calls the structure Mascot, for modifiable and splittable/combinable tranches. It is based on a technique long used in the residential mortgage-bond market known as MACR, or modifiable and combinable Remics. (Remics, or real estate mortgage investment conduits, are special-purpose vehicles that sell mortgage bonds.)

Asset managers’ efforts to put together deals in novel ways or pony up more of their own equity has allowed issuance of U.S. CLOs to reach $58 billion, close to last year’s pace. There are more than $600 billion of the securities outstanding.

Some investors are skeptical of CLO strips. If the instruments aren’t liquid enough, they may not offer the benefits that investors seek, said Dave Preston, a CLO analyst at Wells Fargo. He has heard this concern from only a minority of investors he talks with.

“They wondered if market frictions (including less liquidity) could limit the benefits,” Preston wrote in a note dated May 24. At least 75% of investors he spoke to were “highly interested” in the securities, he added.

Refinancing Risk

Using a mortgage-bond technique for CLOs makes sense because both instruments have risk known as negative convexity, stemming from borrower refinancing. For mortgage bonds, when rates fall, homeowners refinance their loans. Owners of the securities get principal returned to them when they least want it: after rates have fallen and any bonds for sale will pay lower yields.

With CLOs, the asset manager that issues the security can refinance anytime it wants, starting two years after it originally sold the instruments. CLOs carry floating coupons, so the decision to refinance isn’t usually tied to where rates are, but instead where risk premiums are.

When those credit spreads narrow, asset managers that package CLOs may be able to cut their funding costs and boost their profit by refinancing. That hurts CLO investors by giving principal back to them, forcing them to reinvest at tighter spreads and reducing their returns.

An interest-only portion of a CLO grows more valuable to investors the longer it pays interest, which is linked to how long the CLO remains outstanding. That’s what makes it a good hedge when times are getting worse for corporate borrowers: When credit spreads widen, CLOs are less likely to be refinanced, lifting the value of the interest-only portion.

The IO strips have “the potential to be the cheap hedge a bondholder can construct for a CLO portfolio,” according to a Credit Suisse pitching presentation on the structure seen by Bloomberg. The new structure was recently used on CLOs from Rothschild’s Five Arrows unit and LibreMax’s Trimaran Advisors.

The mainly principal portion has a lower coupon than the original CLO portion it is based on, and so it is priced lower, usually at face value. Conventional CLOs can trade above their face value if spreads narrow.

CLOs usually can’t be refinanced for two years, and whenever they do get refinanced, the investor gets the face value of the securities they own, not the premium to face value they may have paid in the secondary market. A lower original price for a mainly principal strip can translate to higher possible returns for the investor until the point the instruments are refinanced.

To contact the reporter on this story: Adam Tempkin in New York at atempkin2@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins, Boris Korby

©2019 Bloomberg L.P.