Venture Capital Firms Are Fighting to Throw Money at Cleantech

Venture Capital Firms Are Fighting to Throw Money at Cleantech

(Bloomberg) -- Just last month, a pair of investment funds closed more than $12 billion of private equity funding for climate- or energy transition-related investments. I noted at the time that it was a welcome inflow of capital to an area that hadn’t seen much interest in years … or ever, really. I also wondered a bit where that money might go.

Now we know — or at least have a decent idea — thanks to Climate Tech VC’s review of funding in the first half of 2021. The newsletter’s authors tracked about $16 billion of funding in 1Q and 2Q 2021, including more than 250 individual deals across seven sectors: carbon, climate, consumer, energy, food and water, industrial, and mobility. That’s almost as much as all of 2020 and not far behind 2018’s total of $17.9 billion.

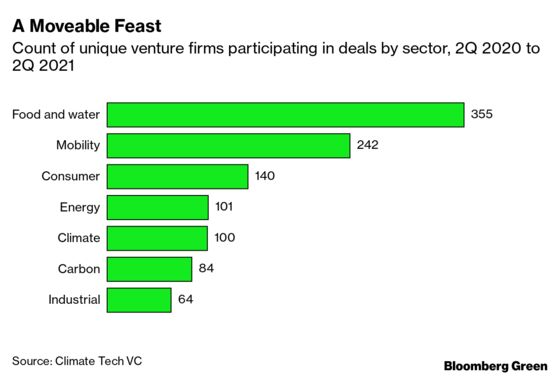

That big investment figure is noteworthy, but equally noteworthy is how investors are approaching the sector. Climate Tech VC splits its data in a very useful (if atypical) way: by the number of unique firms investing in each sector.

A decade ago, almost the entirety of investor interest in cleantech was electricity- (solar, wind), transport- (biofuels) or efficiency-related (a suite of software applications and software-as-a-service business models). Today? More venture firms are interested in food than anything else, by a wide margin. Next in investor interest is mobility, which, given that it includes everything from scooters to aviation, is a far broader category than transport fuel. The consumer sector, which was relatively minor a decade ago, is third.

Meanwhile, the leading sectors of 10 years ago are now laggards, at least in terms of the number of firms interested in backing early-stage companies and founders. To me that’s a very good thing, a sign of how much wind, solar, lithium-ion batteries, and some industrial service models have matured.

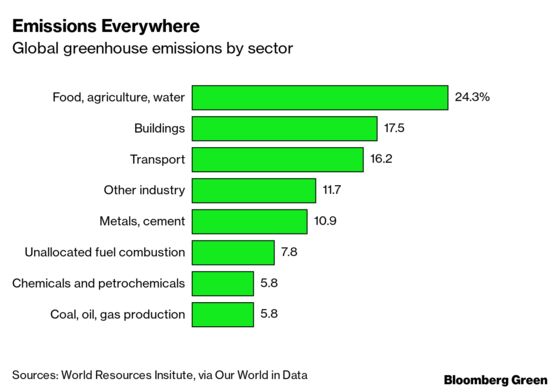

There’s also now a pleasing alignment between the number of firms interested in climate tech sectors and those sectors’ climate significance. Food and water is the single biggest category of emissions today; transport is third, only slightly behind the buildings sector, which consumes a great deal of both electricity and heat generated by fossil fuels.

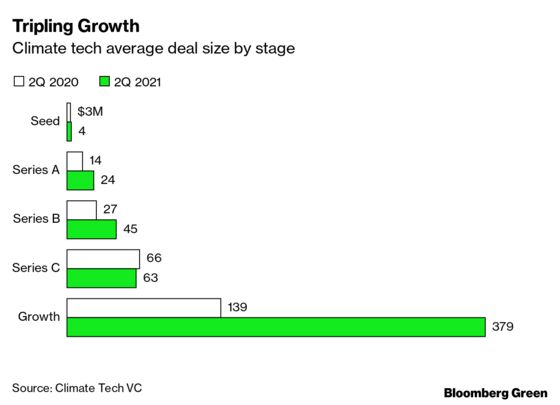

Also noteworthy in Climate Tech VC’s data: Deal sizes in almost every tier of climate tech venture investing increased last year. Growth equity rounds, which fund major expansions and often involve building manufacturing capability and/or expanding to multiple markets, tripled on average to almost $400 million. With the two funds I mentioned in my earlier newsletter — TPG Rise Climate and the Brookfield Global Transition Fund — possibly closing as much as $20 billion in total this year between them, there looks to be plenty of interest in that cohort.

Again, all good news for climate. Here’s one more trend worth watching for both founders and investors: Climate Tech VC’s data show that seed funding sizes rose by a third in the past year, to $4 million from $3 million. But that relatively modest increase belies the valuations these startups have been tagged with once that fundraising is completed.

Last weekend, founder and early-stage investor Immad Akhund noted on Twitter that in the latest batch of Y Combinator startups he’d considered, “climate tech startups have the biggest premiums and are the hardest to get allocation in.” Nothing wrong with being a hot ticket, of course, though as veteran angel investor Joanne Wilson says of early-stage investing in general, “valuations have become out of control.” The median later-stage fundraise, meanwhile, is now taking place at a billion dollars.

Heady valuations and investor FOMO (fear of missing out) coupled with the very real need to fund planetary-scale innovation provide quite a tailwind for climate tech. Those outsize numbers are a sign of enthusiasm, but they’re also an implicit promise from founders to investors that their companies will grow to match expectations. Here’s hoping, for the climate’s sake, that a healthy number of highly-valued climate tech startups succeed in that.

©2021 Bloomberg L.P.