U.S. Energy Transition to Fuel Utility Dealmaking in 2021

Clean-Energy Transition Set to Fuel Utility Dealmaking in 2021

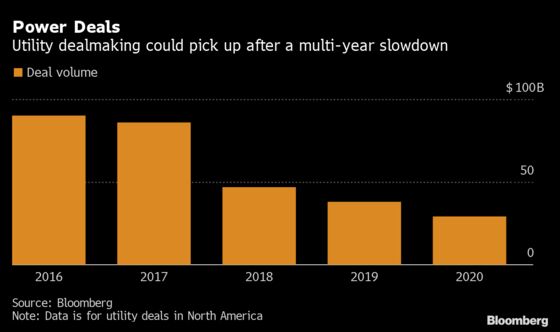

(Bloomberg) -- Utility dealmaking is poised to pick up in 2021 as companies shake off a dour year that saw the least activity in more than a decade.

While energy powerhouses including NextEra Energy Inc. are on the hunt for their next big acquisition, others may look to shed their natural gas arms or other assets to simplify their businesses and meet climate goals.

“We believe 2021 will be a volatile and intense year, with incredible pace,” said George Bilicic, vice chairman of investment banking and the global head of Power, Energy & Infrastructure at Lazard Ltd. “It is completely possible to see a couple or more very large transactions, whether of a merger-of-equals type or otherwise.”

Here’s a look at some of the forces driving activity this year.

Gas Dump

More utilities may look to sell their natural gas assets in 2021 as climate concerns push the fossil fuel further out of favor and power providers face pressure to curtail their emissions.

“The global ESG theme has been building momentum for the past 18 months or more,” said Ray Wood, co-head of global natural resources investment banking at Bank of America. “This has pressured valuations for fossil-heavy exposures.”

CenterPoint Energy Inc. has already said it will announce a sale of its Oklahoma Gas and Arkansas Gas utilities by the second quarter. CenterPoint, together with OGE Energy Corp., is also considering a sale of pipeline company Enable Midstream Partners. Dominion Energy Inc. last year unloaded most of its gas units to Warren Buffett’s Berkshire Hathaway Inc. for $4 billion.

“To the extent that utilities have carbon-intensive assets, they will be under pressure from government entities and the marketplace,” said James Schaefer, a senior managing director and head of energy and utilitiesat Guggenheim Securities LLC, the investment banking arm of Guggenheim Partners LLC. “The pressures we are seeing from investors are unique in history.”

Reliable Returns

Other utilities could look to streamline their businesses, spinning off unregulated power assets in a bid for more predictable returns.

Exelon Corp. said last quarter it had hired advisers to evaluate its corporate structure -- and the potential separation of its generation unit. Public Service Enterprise Group Inc., meanwhile, said last summer it was weighing the sale of about 7.2 gigawatts of generation. CenterPoint Energy Inc. also has said it wants to sharpen its focus on regulated utilities.

“We’re going to see M&A investment driven by divestitures,” said Miles Huq, a partner at Ernst & Young LLP. Utilities will opportunistically look to shed non-core assets “that may be better-suited for other investors.”

Activist Investors

Underperforming utilities may face pressure from activist investors to explore sales as a way to boost their value. One investor, Elliott Management Corp., had pushed this strategy on several utilities, including NRG Energy Inc., which in 2018 completed a $1.35 billion sale of clean-power assets. Last year, Elliott took a stake in Midwest utility-owner Evergy Inc. and pushed the company to conduct a review of its business including a possible sale. The company ultimately reached an agreement with Elliott to remain independent.

“Activism is here to stay in the power and utility sector,” said Anthony Ianno, global co-head for power, utilities and infrastructure at RBC Capital Markets.

Big Game Hunting

NextEra, the world’s most valuable electricity company, has been on the hunt for a major acquisition. Last year, it made an unsuccessful bid for Duke Energy Corp., one of the biggest U.S. utilities, and it may be looking at other targets this year in an effort to balance its heavy wind and solar portfolio with its utility arm.

At an investor conference in September, Chief Executive Officer Jim Robo laid out the ground rules for an acquisition: A deal must be strategic, accelerate the clean-energy transformation, reduce costs for consumers and be doable from a regulatory standpoint. However, such deals are time-consuming and face significant regulatory scrutiny. A NextEra representative declined to comment.

European Expansion

There’s strong interest from companies in Europe and elsewhere to establish or expand their U.S. presence as the energy transition takes root there, according to Jeff Holzschuh, a Morgan Stanley managing director and chairman of the institutional securities group.

In October, Avangrid Inc., the U.S. arm of Iberdrola SA, agreed to buy PNM Resources Inc. of New Mexico for $4.3 billion, strengthening the Spanish utility giant’s position as a global giant in the power industry. Total SE and Orsted A/S have also explored U.S. expansion, according to advisers.

While some companies are looking for new growth areas after saturating their home market, others have have clean-energy expertise that they want to export. “There’s a consensus change is coming,” Holzschuh said.

Clean-Energy Caveat

While these factors point to an uptick in deals this year, there’s at least one thing that might mute activity: renewables growth.

States keen to boost emissions-free electricity can allow utilities that build wind and solar farms to pass those costs to ratepayers, which is a less expensive way to grow.

“M&A is ultimately the most expensive form of growth,” said Katie Bays, an analyst at FiscalNote Markets.

©2021 Bloomberg L.P.