Citi Shares Slump After Revenue Growth Stalls in Consumer Unit

Citigroup Bond Traders Eke Out Win in Market That Stung JPMorgan

(Bloomberg) -- An unexpected bounce in bond trading wasn’t enough to counter a lack of growth in Citigroup Inc.’s sprawling consumer division.

Shares declined after revenue was little changed in the firm’s global consumer bank, an area where shareholders have been told to watch for acceleration this year. The number of open accounts in Citigroup’s U.S. retail banking division hasn’t increased in the past year, while average deposits for the unit climbed only 1 percent.

Citigroup has spent years expanding its credit-card offerings and retail-banking services, so the division’s slowing revenue growth has been a source of frustration. Last week, the company’s president, Jamie Forese, said he was leaving the company. He struggled to have his voice heard on strategy for the division, which offers retail products across 19 countries, a person familiar with the matter told Bloomberg at the time.

Citigroup shares declined 0.3 percent to $67.20 at 11:37 a.m. in New York. They have gained 29 percent this year, compared with a 15 percent increase in the KBW Bank Index.

Still, Chief Executive Officer Michael Corbat said on Monday that the firm’s strategy for its U.S. consumer unit was “showing good early results” after the firm introduced new products in recent quarters. Excluding gains from the sale of the Hilton Worldwide Holdings Inc. credit-card portfolio a year earlier, the unit’s revenue climbed 4 percent.

The bank rolled out a national digital-banking franchise and debuted a high-yield savings account to attract customers outside its core metropolitan areas. The firm also introduced new personal loan products for card customers.

“Our digital sales deposits grew by $1 billion -- that’s both new to bank customers as well as to existing customers,” Chief Financial Officer Mark Mason said on a conference call with reporters Monday morning. “We’re actually very pleased with the progress that we’re seeing. That $1 billion of deposits through our digital channel is the equivalent of all that we did last year in 2018. So very good take-up in terms of those capabilities and deposit growth there.”

In a potentially foreboding sign for the division, Citigroup set aside $1.98 billion to cover souring consumer loans during the first quarter as the unit’s net credit losses climbed 10 percent. Card loans are “seasoning” in the U.S., the bank said, using an industry term signifying some increase was to be anticipated after a period in which the bank signed up more borrowers. Citigroup has said it plans to use its status as the world’s largest credit-card issuer to sell customers other products and services, such as online checking accounts.

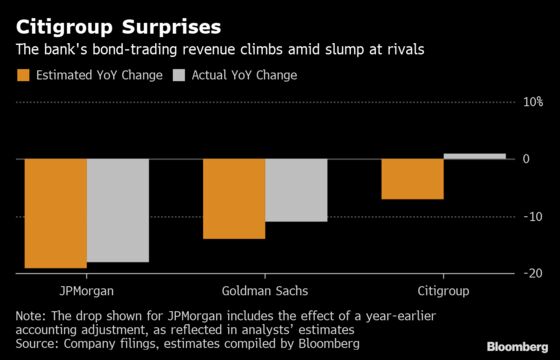

The bank’s fixed-income, currencies and commodities traders managed to boost revenue 1 percent from a year earlier, withstanding a slump that ensnared rivals JPMorgan Chase & Co. and Goldman Sachs Group Inc. FICC traders generated $3.45 billion, countering disappointing results from their colleagues in equities, where revenue slumped 24 percent to $842 million. Combined, trading was down 5.2 percent.

Citigroup credited resilient demand for spread products, but said it also fared well with products tied to interest rates -- a category JPMorgan said last week suffered from lower investor activity. That helped Citigroup’s fixed-income unit narrow the gap with JPMorgan’s franchise, which still ranks No. 1.

“We saw continued strength inside of our FICC business, particularly around rates as a bit more certainty around the direction of rates started to play out,” Mason said on Monday. “And we saw good corporate client activity in G-10 rates specifically. So the combination of that activity in basically the final two weeks of the quarter really aided in what we were able to deliver.”

Here are other highlights from Citigroup’s results:

- Net income climbed 2 percent to $4.71 billion, or $1.87 a share. That topped the $1.80 average of analyst estimates compiled by Bloomberg.

- Firmwide revenue during the first quarter slipped 2 percent to $18.58 billion, in line with analysts’ estimates. Costs fell 3 percent to $10.58 billion, a bigger drop than analysts had expected.

- Total revenue from investment banking amounted to $1.35 billion. Debt underwriting brought in $804 million, a 15 percent increase that topped estimates and countered weakness from the equity capital markets division. Advisory revenues surged 76 percent to $378 million, compared with the $307 million analysts projected.

- The firm’s efficiency ratio -- a key measure of profitability that shows how much it costs to produce a dollar of revenue -- improved to 57 percent. It was 57.8 percent in the final months of last year.

To contact the reporter on this story: Jenny Surane in New York at jsurane4@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, Daniel Taub

©2019 Bloomberg L.P.