Citgo Eyes $1.2 Billion Term Loan Amid Fight for Refiner

Citgo Eyes $1.2 Billion Loan Amid Battle for Control of Refiner

(Bloomberg) -- Citgo Petroleum Corp. is looking to get a $1.2 billion loan to fund its daily operations as U.S. sanctions cripple its parent company, state oil giant Petroleos de Venezuela SA.

The Houston-based refiner hired Houlihan Lokey to find lenders to help it refinance bank credit lines maturing this year, a slide deck seen by Bloomberg shows. The deal launched this week and is expected to close on March 22, according to the presentation, which was given to investors by Curtis Rowe, Citgo’s vice president of finance.

The five-year term loan B may pay a coupon of between 4.5 and 5.5 percentage points above the Libor rate and could be issued at 99 cents on the dollar, according to the presentation. Proceeds will be used for "general working capital requirements" and to "provide ongoing liquidity,” the slides show.

The new loan would replace a $900 million secured revolver and a $320 million accounts receivable facility, according to the presentation. Deutsche Bank AG was the lead arranger of the revolver, issued in 2014 alongside Citgo’s existing term loan, which matures in 2021. The German lender and other banks involved in that financing have been reluctant to roll over their exposure, leading Citgo to consider other options, people with knowledge of the matter said.

Investor Interest

The company has been discussing the new financing with alternative asset managers and holders of its existing term loan, the people said. It has received dozens of calls from firms interested in providing refinancing options for its revolver since February, one of the people said.

Citgo said it values collateral for the loan, which includes its refineries as well as the value of inventory and receivables, at over $13 billion, according to the presentation. The company reported earnings before interest, taxes, depreciation and amortization of around $1.6 billion in the twelve months ended Sept. 30, the slides show.

Representatives for Houlihan Lokey, Citgo and Venezuela’s Finance Ministry didn’t respond to requests for comment. Deutsche Bank didn’t immediately provide comment.

PDVSA Payment

Petroleos de Venezuela, or PDVSA, has an upcoming interest payment of around $70 million coming due next month on its 2020 bonds. Those notes are backed by a stake in Citgo. Failure to pay could be catastrophic for PDVSA, and may lead bondholders and other creditors to attempt to seize the Citgo assets. The presentation doesn’t mention the PDVSA notes, and U.S. sanctions currently prevent Citgo from paying dividends to PDVSA.

A new Citgo board appointed by Venezuelan National Assembly President Juan Guaido has considered using an escrow account that may hold up to $560 million to pay the PDVSA 2020 bond. It’s unclear how the U.S.-backed Guaido, the Venezuelan legislature or President Nicolas Maduro are involved in the new Citgo loan.

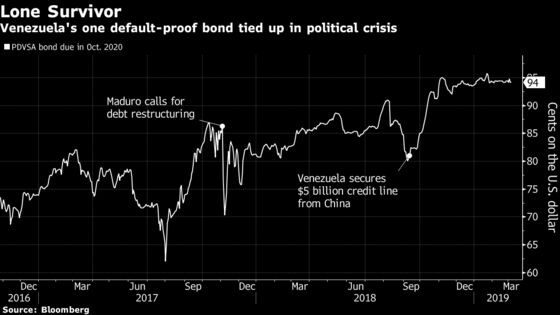

The PDVSA 2020 bond is the only Venezuelan debt security that hasn’t fallen into default, as Maduro’s regime prioritized payments to ensure he wouldn’t lose the collateral, a 50.1 percent stake in Citgo Holding Inc. Because the bonds are asset-backed and Venezuela has kept paying them, they’re quoted at 94 cents on the dollar, compared with an average price for Venezuelan and PDVSA debt around 30 cents.

After Maduro was sworn in for a new term Jan. 10, Guaido emerged to stake his claim to the presidency citing articles in the constitution. Since then, Venezuela has had two presidents of sorts and Guaido named his own boards to state oil company PDVSA and to Citgo. Despite not having physical control over PDVSA assets in Venezuela, given that the U.S. government has recognized him as the rightful leader of the South American country, he could receive favorable rulings to actions brought before U.S. courts.

--With assistance from Jack Farchy.

To contact the reporters on this story: Davide Scigliuzzo in New York at dscigliuzzo2@bloomberg.net;David Wethe in Houston at dwethe@bloomberg.net;Ben Bartenstein in New York at bbartenstei3@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, ;Rita Nazareth at rnazareth@bloomberg.net, ;David Marino at dmarino4@bloomberg.net, ;Simon Casey at scasey4@bloomberg.net, Dan Wilchins

©2019 Bloomberg L.P.