Citadel Puts Clout Behind Effort to Safeguard U.S. Treasuries

Citadel Puts Clout Behind Effort to Safeguard U.S. Treasuries

(Bloomberg) -- Ken Griffin’s $32 billion hedge fund is backing efforts to make the Treasury market safer and sounder through the backstop of a central clearinghouse.

Citadel last month became the first firm to clear both a Treasury and repurchase agreement through a new Depository Trust & Clearing Corp. platform. In March, DTCC changed its rules so more companies like Citadel that aren’t members of its clearinghouse can get trades processed there by going through a member firm.

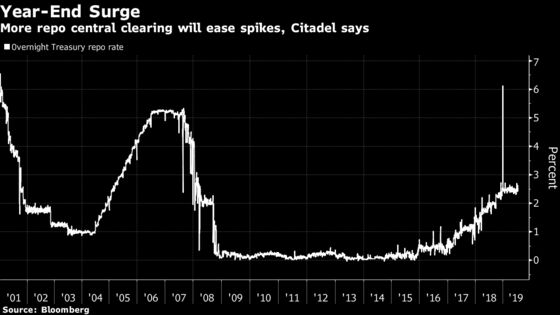

Short-term funding markets have been increasingly vexed over recent years by spikes in rates at month- and quarter-end, when many dealers pull out of the market. Citadel sees DTCC’s new clearing program as a way to help eliminate that.

“We support the expansion of central clearing options for Treasury market participants,” Dan Dufresne, global treasurer at Citadel, said during an interview about the DTCC program. “There are many benefits to expanding access to central clearing of cash and repo trading, including improved funding market functioning and liquidity, reduced repo volatility, improved market depth and a reduction of counterparty credit risk.”

Citadel hasn’t been the only new participant: J.P. Morgan Securities LLC, the broker-dealer division of JPMorgan Chase & Co., also used the new system.

While regulators mandated central clearing for other assets including most swaps in the wake of the financial crisis, it wasn’t required for Treasuries. Clearinghouses, which pool resources of members to ensure losses at one firm don’t harm others, are a key way to reduce systemic risks to financial markets.

The Federal Reserve pushed through changes to shore up repo and has advocated for central clearing after the 2008 collapse of Lehman Brothers Holdings Inc. showed just how crucial short-term funding markets were. Attention was put on how Treasuries clear after Oct. 15, 2014, when there was a massive “flash rally” in Treasuries that had no apparent trigger. The Treasury Department got a bundle of feedback on the event, with many blaming the huge move on a lack of uniform clearing methods.

DTCC, through its Fixed Income Clearing Corp. division, launched the sponsored-member program that Citadel is using several years ago and has been making adjustments to bring in more participants. The system is handling more repo activity. FICC was counterparty to about $190 billion in repo with money-market mutual funds at the end of June, up from $5 billion two years earlier, according to Office of Financial Research data.

In the cash market, FICC has long cleared Treasury trades conducted between dealers. But more transactions are being done by a relatively new class of company called principal trading firms, many of which aren’t FICC members so most of these trades don’t go through DTCC’s clearinghouse. That’s where the new sponsorship program can help.

“Participants in the U.S. Treasury and Treasury repo markets interact and clear their trades through a complex, inefficient and opaque system,” said Dufresne. He is also vice chairman of the Treasury Borrowing Advisory Committee, which meets with the Treasury regularly to advise on debt-management polices. “Leveraging a clearinghouse for more of this activity greatly simplifies and reduces unnecessary frictions in this critical system.”

To contact the reporter on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Nick Baker, Mark Tannenbaum

©2019 Bloomberg L.P.