China’s Stressed Borrowers Face Wall of Debt Due in March

China’s Stressed Borrowers Face Wall of Debt Coming Due in March

(Bloomberg) -- China’s most stressed dollar debtors face a major test of their financing capacity next month, with over a tenth of all bonds coming due just as the nation grapples with the economic impact of a virus that continues to spread.

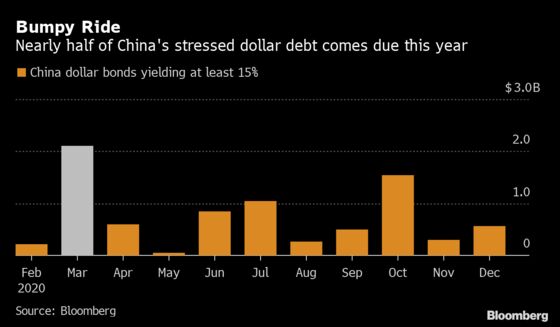

About $2.1 billion of offshore notes with yields of at least 15% -- characterizing them as stressed -- are due in March, the biggest monthly maturity wall this year, according to data compiled by Bloomberg. Most were sold by property developers, an industry that’s been hard hit with China’s transport system hobbled and much of the economy in an effective lockdown in recent weeks.

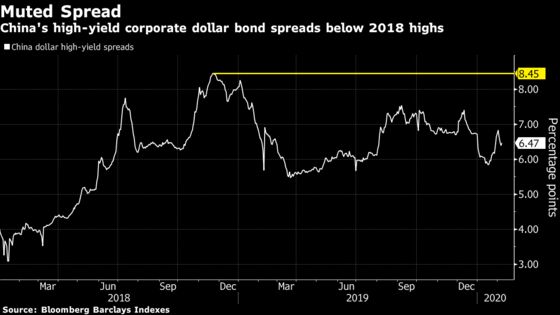

While the premiums on China’s high-yield debt look all the juicier after the recent slide in global bond yields, the risks have arguably risen and spreads are still well below levels seen as recently as 2018. The upcoming refinancings will showcase how confident buyers are in the housing market’s resilience, and in officials’ preparedness to assure liquidity to a vital industry.

“If the virus lingers longer than expected, the economy will take a sharp hit, and Beijing will be in the awkward position of finding ways to inject larger stimulus measures without leading to more debt problems down the road,” said Andrew Collier, a managing director at Orient Capital Research in Hong Kong.

Home sales are set to collapse this month as firms close their sales offices, according to Bloomberg Intelligence analysts including Kristy Hung. The immediate saving grace is that January and February only account for about 4% of typical annual property sales, according to Goldman Sachs Group Inc. analysis.

So far, the indicators are that demand remains for high-yield China dollar debt. China Central Real Estate Ltd. got more than $2 billion in orders for a $300 million note last week.

Analysts point to past equity-capital raising and significant land banks among some of the larger developers as strengths. Another aid: China’s securities regulator has agreed to fast-track approval on refinancing plans and “proactively guide” investors to offer greater flexibility on repayment deadlines.

Struggling issuers typically sell land parcels to stronger developers with ample funding or otherwise monetize their holdings, said Omotunde Lawal, head of emerging market corporate debt at Barings UK Ltd. in London. “Only after those types of avenues have been exhausted will we start to see true strain for the weak developers.”

But some may encounter liquidity crunches if the health crisis lasts beyond several months, according to Christopher Yip, a credit analyst at S&P Global Ratings. “Weak developers that rely on asset disposals to deal with maturing debt may find it difficult to close deals, as most potential buyers may take a step back,” Yip wrote in a note earlier this month.

Bloomberg Intelligence: China Property Bonds to Provide Premium After a Price Correction

Xinhu Zhongbao Co., a Hangzhou-based firm, has the biggest stressed bond bill coming due in March, at $600 million. In November -- months before the coronavirus fears hit -- S&P lowered its outlook on the company to negative, saying “liquidity hinges on an improving sales performance, successful execution of onshore and offshore debt issuances, and monetization of its investments or land assets.”

Calls and emails to the firm went unanswered.

Conditions may be all the tougher for leveraged borrowers given that policy makers have steered clear of any big-bang stimulus, with the People’s Bank of China continuing to favor a more targeted approach. As a significant chunk of bonds now in a stressed state comes from the private sector, the question remains whether public assistance would be forthcoming. Another challenge: how Beijing could press upon overseas bondholders to show forbearance if needed.

“Measures announced -- such as flexible repayments etc. -- could help domestic institutional investors, they may accept that,” said Roy Kwok, a partner and senior portfolio manager at DeepBlue Global Investment in Hong Kong. “However, that won’t really help the offshore market. Issuers still need to repay debts on time -- or if they can’t they need a restructuring plan.”

--With assistance from Helen Sun and Annie Lee.

To contact the reporters on this story: Rebecca Choong Wilkins in Hong Kong at rchoongwilki@bloomberg.net;Molly Dai in Singapore at bdai13@bloomberg.net

To contact the editors responsible for this story: Chan Tien Hin at thchan@bloomberg.net, Christopher Anstey, Shamim Adam

©2020 Bloomberg L.P.