(Bloomberg Opinion) -- The reasoning given by Australia’s Treasurer Josh Frydenberg for blocking a CK Asset Holdings Ltd.-led consortium from taking over pipeline operator APA Group doesn’t make a lot of sense.

A deal would be contrary to the national interest because it would result in “an undue concentration of foreign ownership by a single company group in our most significant gas transmission business,” Frydenberg wrote Wednesday in a statement halting the A$13 billion ($9.5 billion) acquisition.

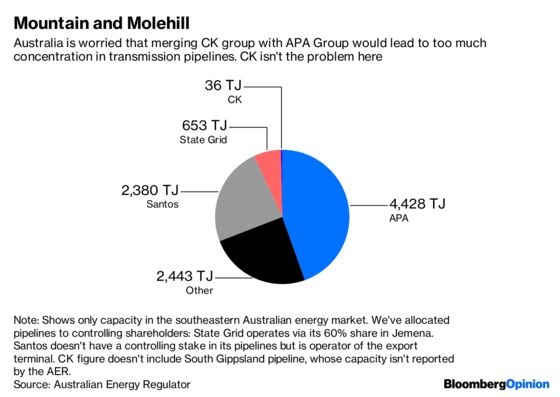

If a merged CK-APA would have undue concentration in gas transmission, that’s entirely down to the APA side of the deal. CK group companies have just four tiny transmission pipelines in Australia: two of them serving a handful of country towns in Victoria and two others supplying the minor cities of Rockhampton and Alice Springs. Another is being built to fuel remote gold mines in Western Australia.

In total, they can move a bit more than 36 terajoules of gas a day. APA, by contrast, shifts about 4,428 terajoules a day on its transmission pipes. The country’s antitrust regulator has already examined the deal and found no reason to block it on competition grounds.

Reading between the lines of Frydenberg’s statement, it’s clear there are two real issues afoot.

One is the dominance that APA has already attained in the domestic market. That’s an obvious issue: Australia, on track to become the world’s largest LNG exporter, is looking to build multiple gas import terminals because of the difficulty of getting competitively priced methane from domestic fields to consumers in the country’s southeast. That was the fault of Frydenberg’s predecessors, but if he’s serious about the problems it’s causing he needs to look at ways to break up this company.

Another is the question of CK group’s relationship with China. As we’ve argued in the past, there’s a mistaken tendency in Australia to treat CK group – whose main divisions are independent, Hong Kong-based Cayman Islands-registered companies – as the equivalent of state entities such as State Grid Corp. of China. (The country’s national broadcaster described it as a “Chinese-backed company” in its report on Frydenberg’s decision.)

The Li Ka-shing dynasty’s relationship with the mainland is complex and awkward, but everything about the history of CK’s investments in recent years suggests the group is more wary of Beijing than inclined to do its bidding. Even then, Australia this year passed legislation giving the Treasurer wide-ranging powers to block any nefarious foreign activity in its critical infrastructure.

Still, the decision indicates just how narrow a line CK will have to walk in the future as Beijing attempts to increase its control over Hong Kong and the wider region. A few years ago, Australia was happy to let Li buy numerous local infrastructure assets on the basis that 2047 (the date of expiry for the “one country, two systems” arrangement under which Hong Kong returned to Chinese sovereignty) was far distant.

Back then, the prospect of a privately controlled Hong Kong business becoming a proxy for the Chinese state seemed absurd. Right now, it looks a little less outlandish. Victor Li, who replaced his retired billionaire father as group chairman this year, will have to tread carefully in his dealmaking if this view spreads more widely.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2018 Bloomberg L.P.