(Bloomberg Opinion) -- Concerns over Lenovo Group Ltd.’s financial outlook have brought new scrutiny to the Chinese maker of computers, servers and smartphones.

Its stock dropped 5.7% Wednesday in Hong Kong, the fourth straight decline, after a tweet from short-seller Muddy Waters referenced a recent report by Bucephalus Research Partners Ltd. That piece highlighted a series of issues it had with Lenovo’s financial position and accounting. Lenovo didn’t provide a response to questions sent by Bloomberg Opinion.

Without expressing any opinion on the issues raised by Bucephalus, there is one Lenovo data point that deserves closer scrutiny: accounts receivable.

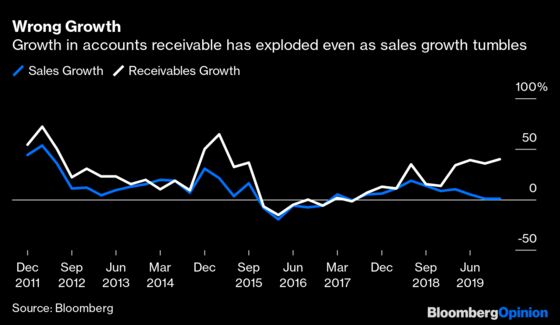

Lenovo, like much of the technology hardware sector, has suffered a slowdown in sales growth over the past few years. Revenue climbed just 0.5% in the December quarter, and 1.1% in the prior three months.

Yet accounts receivables has shot up. It rose 40% in the December quarter, the fourth straight period that growth exceeded 30%. This might make sense in an era where growth is strong and the company has a longer list of IOUs on the docket waiting for clients to pay. But when revenue has barely changed, and there’s little prospect of a rebound in the near-term, such a metric stands out.

One follow-on effect of this disparity, as Lenovo points out in its Feb. 20 investor presentation, is the negative impact on operating cash flow, which dropped almost two-thirds to $538 million, from $1.5 billion a year earlier.

Over the past two years I have sounded the alarm over rising inventories, using that measure across companies and slices of the supply chain to warn about a slowdown in the sector. If you think of accounts receivable as a kind of financial inventory — something that has the potential, but not the guarantee, of being turned into cash — then Lenovo’s current situation isn’t dissimilar.

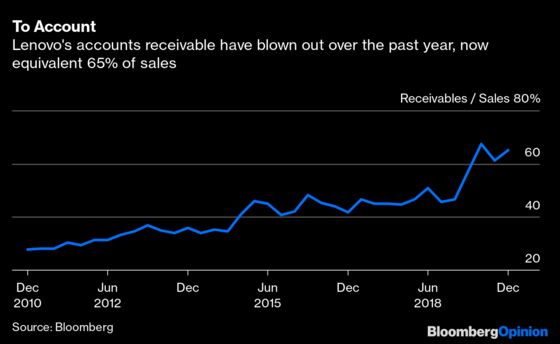

This disparity between sales and receivables growth pushed the receivables-to-sales ratio to 65% in the December quarter. That’s the third straight period it’s been above 60%. Prior to last year, this had topped 50% just once in the past decade.

Lenovo also accounts for another category of receivables — which “mainly comprise amounts due from subcontractors for components sold in the ordinary course of business” — in a separate line item on its balance sheet. If you add this figure in, the total comes to 87% of sales. While this is also near historic highs, the contrast to a few years ago isn’t as stark.

An interesting caveat for these receivables is that long-dated IOUs haven’t jumped as a proportion of the total. Most of the spike has been in those due within 30 days, not 90 days or more.

One possible explanation for higher receivables would be a drop in factoring, which is the practice of selling these IOUs to a third party at a discount. The company gets immediate cash (albeit less than the nominal value) and the buyer gets to collect that debt and make a profit. Chief Financial Officer Wong Wai Ming mentioned this during the Feb. 20 investor call he said “our accounts receivable factoring volume dropped year-to-year.”

However, according to its financial filing for the December quarter published at the same time, the cost of factoring increased by $20 million, which helped drive up total finance costs by 25%. So, if factoring amount fell but costs rose, then that might indicate Lenovo needs to accept a larger discount in order to convert those accounts receivable into immediate cash. It could mean that there’s fewer finance companies even willing to take on that work.

In the current macro-economic environment, especially with a pre-existing slowdown in sales and likely impact from the Covid-19 virus to come, companies would do well to rein in line items like receivables and inventory rather than let them balloon.

At Lenovo, these accounts receivable simply can’t be allowed to keep growing. This may require either selling more through factoring with the possibility of taking a bigger discount, or tightening credit for clients, which could hurt the PC maker’s own sales in the face of already weakened demand.

That leaves management with some tough decisions to make, and investors waiting for the company to decide its next move.

To contact the editor responsible for this story: Patrick McDowell at pmcdowell10@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2020 Bloomberg L.P.