China’s Historic Slump to Lay Bare the Scale of the Task Ahead

The scale of the recovery task facing China’s policy makers will be laid bare Friday

(Bloomberg) --

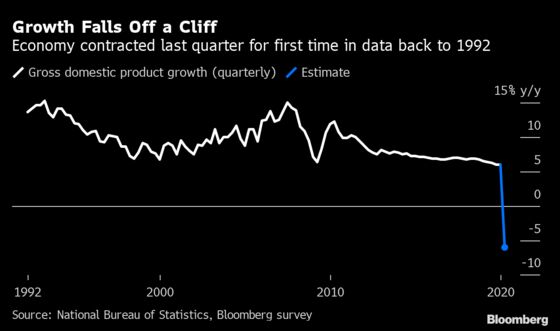

The scale of the recovery task facing China’s policy makers will be laid bare Friday when first quarter gross domestic product data is expected to show an historic slump.

The median forecast of economists surveyed by Bloomberg is for a 6% contraction in the first three months of the year, when the coronavirus outbreak forced an unprecedented lockdown of factories, stores and schools across the country. Bloomberg Economics warns the dive may be as deep as 11%.

At the same time, the government will also release data for retail sales, fixed asset investment and industrial output for March, offering the most complete picture yet of the economic destruction since the virus outbreak.

Unlike the rapid-fire policy response seen in the U.S. and Europe as the disease shuttered economies there, Chinese authorities have offered targeted support and modest monetary easing as they focused on containing the virus’s spread. The first quarter data will provide policy makers a clearer picture of what’ll be needed if they’re to meet long-term economic growth goals.

Indeed, authorities have recently added urgency to their policy response. Credit provision hit a record in March and top leaders last week pledged to expand domestic demand to boost public consumption and investment, as well as faster construction of investment projects, Xinhua News Agency reported, citing a politburo meeting chaired by President Xi Jinping.

Gradual Recovery

“China’s economy is going to recover only gradually,” said Scott Kennedy, senior adviser and trustee chair in Chinese business and economics at the Center for Strategic & International Studies. “If the government over-stimulates, the only result will be a lot of wasted spending and greater debt. And that won’t help resolve the core problem of China’s economy: low productivity.”

How much stimulus China deploys and how swiftly growth can rebound will play a critical role in determining the global recovery too. While the world’s second largest economy is showing renewed signs of strength as workers return and shoppers start to spend again, that nascent recovery will be pressured by a global recession that’s on course to be the worst since the Great Depression.

“The rest of the global economy is now in the grips of the pandemic and there are severe containment measures around the world so that would have a big negative impact in terms of external demand on China’s growth,” International Monetary Fund Chief Economist Gita Gopinath said in an online media briefing on Tuesday. The fund is tipping 1.2% growth for China this year.

Blurry Outlook

The policy outlook has been complicated by the postponement of the annual gathering of the nation’s legislature, which is usually held in early March when the GDP growth target for the year and associated economic plans are unveiled. There’s still no date for when the National People’s Congress will be held, leaving observers with little guidance on the quantity of stimulus that is coming.

A target of 6% would be enough to fulfill the Communist Party’s long-term promise to double gross domestic product and average income by this year from 2010’s levels. But it would require hefty borrowing and spending to pull that off.

Shang-Jin Wei, a China expect at Columbia Business School in New York and formerly Chief Economist of the Asian Development Bank, is among those who argue the government should drop the growth target. Doing so would take pressure off local governments to meet political targets and remove the risk of prematurely unwinding social distancing measures to stoke demand.

“Prevention of a return or the “second wave” of the virus outbreak is more important than getting a high growth rate for the remainder of the year,” he said.

Stimulus Restraint

Most of the stimulus rolled out in China so far has been focused on tax cuts, modest interest rate tweaks, liquidity for banks and financial markets and some extra government spending. That’s a contrast to how policy makers responded to the global financial crisis, when they used a 4-trillion-yuan spending program based around pillar industries such as housing and infrastructure and funding for education, health care and farmers.

While growth rebounded, the cost of that was a surge in debt, housing market bubbles and ghost towns. Total debt to GDP, including the financial sector, ballooned to about 300% in 2019 from about 173% in 2008, according to the Institute of International Finance.

It’s possible that, as the crisis is contained globally and restrictions on working and movement are relaxed, both China and the world experience a sharper than expected recovery, according to Jim O’Neill, Chair of Chatham House and the former Goldman Sachs Group Inc. chief economist who coined the term BRIC.

But in the interim, the kind of stimulus that lifts domestic demand will still be needed.

“Until there is a usable vaccine, it is tough to see life getting anything like being back to vague normality,” O’Neill said.

©2020 Bloomberg L.P.

With assistance from Bloomberg