China's ‘Game Changer’ Pipeline Reform to Supercharge Gas Demand

China's ‘Game Changer’ Pipeline Reform to Supercharge Gas Demand

(Bloomberg) -- China’s looming pipeline reform is poised to spur competition in its natural gas industry, lowering prices and supercharging demand from the world’s top importer in years to come, according to Credit Suisse Group AG.

The government is creating a national pipeline operator from the assets of its three biggest oil and gas companies. The move will break a monopoly that China’s state-owned giants have over downstream users and result in gas prices falling 10% over 2020 and 2021, the bank’s analysts including Horace Tse said in a report. The national operator is likely to be formed by August, Citigroup Inc. said, citing a National Development & Reform Commission official.

“We do not believe that the market has taken active views on post-reform pricing,” the Credit Suisse analysts wrote. “The majority of investors have only focused on asset sales and valuation specific to the pipeline company.”

Lower prices will revitalize China’s gas demand in two years, according to Credit Suisse, predicting consumption growth of 13% in 2021. That outlook contrasts with rival Citigroup Inc.’s view that demand expansion in the world’s biggest natural gas importer will hold steady for another three to four years then slow to about 4% after 2022.

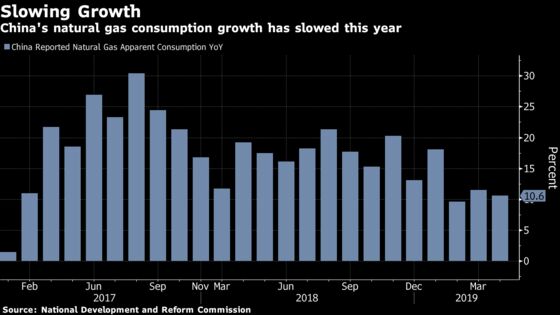

China’s gas demand has skyrocketed in the past two years amid a state campaign that favors the cleaner-burning fuel over coal. Consumption rose 15% in 2017 and a further 18% last year, but that rate may weaken to 11% this year and 10% in 2020 amid an economic slowdown, Credit Suisse said.

Price Declines

Falling prices following the reform will entice higher consumption from industrial users, which make up about 40% of national demand, according to the bank. The national pipeline company will be “a gamer changer,” the analysts wrote.

It has major repercussions for China’s natural gas companies. Without direct pipeline control, top producer PetroChina Co. will probably suffer from price declines and market share loss, while Cnooc Ltd. should gain from the easing of infrastructure bottlenecks, Credit Suisse said.

The pipeline network will continue to expand based on government plans, which could challenge the already oversupplied domestic liquefied natural gas processing and trucking business. Gas distributors will be winners from better demand and improving margins, the bank said.

The pipeline company could operate similarly to China Tower Corp., the $43 billion giant that maintains and operates telecommunication towers in the country, Citigroup analysts including Toby Shek said in a June 4 note, citing comments from NDRC analyst Liu Manping during a May 30 conference call. Some LNG import terminals and gas storage facilities are likely to be included in the pipeline giant, with none of China’s big three oil companies holding a majority stake.

--With assistance from Aibing Guo.

To contact the reporter on this story: Dan Murtaugh in Singapore at dmurtaugh@bloomberg.net

To contact the editors responsible for this story: Ramsey Al-Rikabi at ralrikabi@bloomberg.net, Jasmine Ng, Aaron Clark

©2019 Bloomberg L.P.