(Bloomberg Opinion) -- Just as chemicals conglomerates are going out of fashion in the U.S., they’re back in vogue in China.

The country’s two biggest, Sinochem Group and China National Chemicals Corp. or ChemChina, are finally starting to merge after almost two years of on-again, off-again speculation, Caixin reported at the weekend. That’s in contrast to the way DowDuPont Inc. is reformulating itself into three separate companies. Investors who’ve driven up shares in the publicly traded units of the state-owned Chinese groups this week might want to ponder whether it’s the better path.

Evidence for the outperformance of China’s existing run of national champions is decidedly mixed.

In the 12 quarters before their 2015 merger to create CRRC Corp., Chinese rolling-stock companies CSR Corp. and China CNR Corp. averaged sterling returns on invested capital of 9.2 percent and 7.2 percent, respectively. Over the past four quarters the combined group has averaged a mere 5.6 percent.

That would seem to contradict economic logic. The reason antitrust regulators exist is that, in theory, firms with outsized market shares should be able to extract outsized profits. Under the leadership of entrepreneurial Sinochem boss Frank Ning, surely a chemicals conglomerate with 753 billion yuan ($112 billion) of revenue and an iron grip on the Chinese market should be able to lord it over the likes of BASF SE, Saudi Basic Industries Corp., 3M Co. and the descendants of DowDuPont?

Well, in theory. The problem is that China’s authorities know the economic logic, and aren’t likely to tolerate a chemicals behemoth conspiring against a group of customers that comprise much of the country’s industrial base.

That’s more or less what you saw with CRRC. Despite the elimination of competition in the Chinese rolling-stock market, operating margins trended down for two years following the amalgamation. The proximate cause for that was a decline in top-line sales, but the notable thing is that CRRC was unable to use its market position to at least keep margins steady. Monopolies are all very well, but when your sole buyer is a state-owned monopsony like China Railway Corp. that sort of profiteering won’t wash.

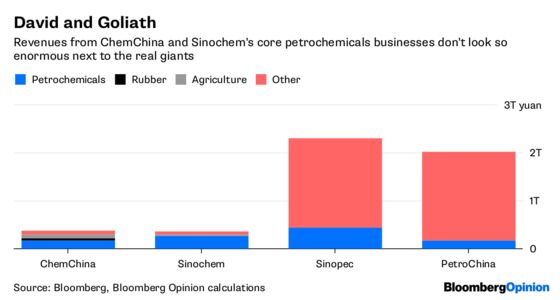

That would suggest a path of suppressed earnings, outsized debts and diminishing returns for the merged group, but there’s a ray of hope from an unlikely corner. While the combined company would be a giant in terms of standalone outfits, in another sense it’s just one player in the market.

With ChemChina’s spin-off of the Pirelli & C SpA tire unit and Syngenta AG likely to be at least partially re-listed at some point over the next few years, the combined entity will look increasingly like a petrochemicals firm. About three-quarters of Sinochem’s revenue comes from petrochemicals and almost half of ChemChina’s.

Even together, those two divisions would be playing second fiddle to China Petroleum & Chemical Corp., or Sinopec, which boasted 438 billion yuan of petrochemicals revenue in its most recent year (compared to 433 billion yuan from the merged group). PetroChina Co.’s 172 billion yuan of revenue from refining and chemicals isn’t all that far behind, either.

Beijing’s push to create monopolistic giants doesn’t work for Chinese consumers or for the companies themselves. The country should be grateful that, in the oil industry at least, a legacy of Deng-era creative competition still exists.

To contact the editor responsible for this story: Katrina Nicholas at knicholas2@bloomberg.net

©2018 Bloomberg L.P.