China Local Government Unit Escapes Default With Late Payment

China LGFV Secures Investor Approval On Late Bond Repayment

(Bloomberg) -- A Chinese local government investment arm narrowly escaped a bond default, ending yet another scare that could have shaken belief in Beijing’s support for such borrowers.

The latest drama offers a fresh signal that Chinese policymakers remain wary of allowing its heavily indebted regional funding vehicles to fail and destabilize a stressed financial system. Beijing also relies on these local government entities, which have been responsible for China’s infrastructure boom in the past decade, to cope with a sharp economic slowdown and unabated trade tensions.

Hohhot Economic & Technological Development Zone Investment Development Group, a local government financing vehicle from the northern region of Inner Mongolia, has repaid 565 million yuan ($80 million) of principal and 68 million yuan interest on its 1 billion yuan privately issued note on Monday, according to a company statement to bondholders, which was seen by Bloomberg.

The resolution came after the borrower missed Friday’s deadline to deliver early repayment on the bond. Investors had earlier exercised a put option on the note.

The Hohhot LGFV said it has also secured an extension to repay the remaining 435 million yuan principal on that note by March 6. The issuer originally had a 10-day grace period to make good on the debt obligations.

The borrower’s earlier bond payment failure had rekindled concerns about the fate of Chinese LGFVs, a group of borrowers whose outlook is closely tied to Beijing’s shifting definition of its implicit backing.

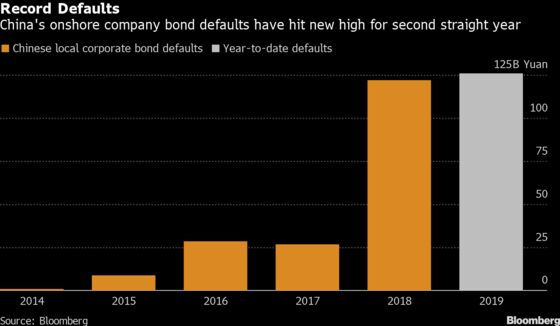

The development also came just as onshore corporate bond defaults in China rose to a record high this year as the worst economic slowdown in three decades constrains Beijing’s ability to bail out failing borrowers.

Companies such as the LGFV from Hohhot have until recently emerged as major beneficiaries of the surge in defaults as investors feared debt from ailing private businesses and on expectations that Beijing wouldn’t let these government-linked firms ever go bust.

The borrower said it missed the repayment deadline because its “former main leader” was under investigation and some of its assets were frozen. It added that it plans to accelerate asset sales and raise funds via various means to repay the note.

According to an official announcement dated September 7, 2018, Li Jianping, a senior Communist Party member of the Hohhot Economic & Technological Development Zone, was put under a probe for serious violation of laws and rules. Calls to the company’s financing department went unanswered.

For LGFVs, their willingness to service debt matters much more than their capacity to do so when it comes to bond payments, said Zhang Xu, chief fixed-income analyst with Everbright Securities Co. The former relies on factors including regional financial strength and changes in local leadership.

Modest Rebound

Some of the dollar bonds issued by LGFVs rebounded modestly Tuesday. Inner Mongolia High-Grade High Way Construction and Development Co.’s dollar note due 2020 rose by 0.07 cents on the dollar to 99.3 cents as of 11:31 am in Hong Kong after dropping 0.7 cents on Monday, according to prices compiled by Bloomberg. Yunnan Metropolitan Construction Investment Group Co.’s bond due 2022 gained 0.2 cents following a drop of 2.2 cents on Monday.

A similar incident last year briefly jolted China’s bond market as well. Xinjiang Production Construction 6th Shi State-owned Assets Management Co., a cotton trader owned by the local government, missed interest and principal on a 500 million yuan note, before making good on the delayed repayment a few days later.

Compared to the case of Xinjiang Production, the proposal by the Hohhot LGFV, which is from one of China’s poorest regions, looks much weaker, according to Liu Chenhan, a fixed income analyst with Northeast Securities Co.

“We expect there will be more cases of LGFVs missing private bond payments in the future given the slowing economy, and the market will turn more cautious toward their privately placed notes,” said Liu.

Regional governments in China have long used LGFVs to raise funds via off-balance-sheet debt. Without formal state backing, Beijing’s shifting attitude over the years has dictated their fortunes: after years of lax oversight, Beijing placed restrictions on debt issuance by LGFVs in 2014 to cut financial risk, only to ease those later as the economy started slowing.

The outstanding value of yuan-denominated bonds sold by LGFVs now totals 8.3 trillion yuan, according to data compiled by Bloomberg. Outstanding value of offshore notes from such entities is around $71.5 billion.

--With assistance from Qingqi She, Tongjian Dong and Molly Dai.

To contact the reporter on this story: Ina Zhou in Hong Kong at hzhou179@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Shen Hong, Chan Tien Hin

©2019 Bloomberg L.P.