China Huarong Showdown Reveals Beijing’s Tougher Stance on Risk

China Huarong Showdown Reveals Beijing’s Tougher Stance on Risk

(Bloomberg) -- Market turmoil surrounding China Huarong Asset Management Co. intensified on Wednesday as investors interpreted government silence on the embattled firm as a lack of official support.

The Communist Party has yet to comment on the distressed-debt manager, which is controlled by the finance ministry, even as concern about a potential restructuring sent its dollar bonds plunging to distressed levels. China’s State Council, the country’s top administrative body, instead reinforced the idea that struggling state-backed companies shouldn’t rely on government support.

In a statement late Tuesday, the State Council urged local government financing vehicles to restructure or enter liquidation if they can’t repay their debts. While it’s unclear if the comments were meant to send a veiled message about China Huarong, they added to the perception that the government is taking a tough stance on reining in risks to the financial system.

The resulting turbulence in the offshore debt market is having an impact on fundraising for even blue-chip Chinese firms. Tencent Holdings Ltd., which along with other tech giants has also faced increased government scrutiny in recent months, is holding off marketing a planned dollar bond deal Wednesday to raise as much as $4 billion, according to people familiar with the matter.

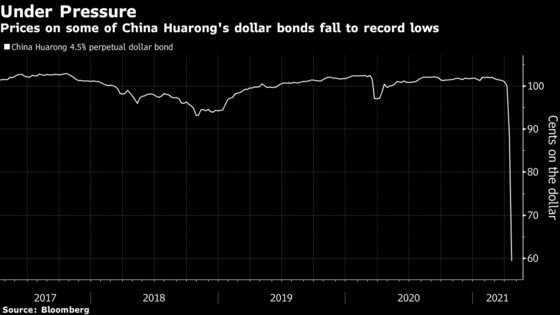

Meanwhile, the selloff in China Huarong’s bonds is deepening, with the notes set for another day of record lows. The firm’s 4.5% perpetual dollar bond fell 9.7 cents on the dollar to 61.2 cents, Bloomberg-compiled prices show. The company, which has yet to publish its full-year earnings after missing a March 31 deadline, has said it has access to liquidity and is making payments on time.

“The lack of information is being taken negatively,” said Paul Lukaszewski, head of corporate debt for Asia Pacific at Aberdeen Standard Investments in Singapore. “Investors are increasingly concerned about the broader implications if Huarong’s offshore bonds are pushed into financial restructuring.”

Withdrawing support from weak or badly run companies is becoming an increasing trend in China as President Xi Jinping seeks to restrain growth in debt in the world’s second-largest economy. One consequence is that state-owned enterprises have replaced private firms as the country’s biggest source of defaults.

SOEs reneged on a record 79.5 billion yuan ($12.1 billion) of local bonds in 2020, lifting their share of onshore payment failures to 57% from 8.5% a year earlier, according to Fitch Ratings. The figure jumped to 72% in the first quarter of 2021.

The dilemma for authorities is how to avoid contagion spilling over into the financial system as investors reprice risk and sell bonds previously considered immune from default because of an implicit state guarantee.

An onshore default by a state-linked coal producer in November triggered a brief selloff in the nation’s credit market. Further defaults, including by chipmaker Tsinghua Unigroup Co., also caused short-term market volatility.

But failure to successfully tackle rising debt levels could fatally undermine the government’s efforts to build a world-class economy to rival that of the U.S.

Local government debt is of particular concern. Hidden debt at local levels was elevated to a “national security” issue at China’s annual legislative meetings last month. Local governments had 14.8 trillion yuan ($2.3 trillion) of hidden debt last year, and the figure could climb further this year, according to a government-linked think tank.

Like much of China’s debt issues, the problem with local government financing vehicles, or LGFVs, dates back to 2009 and the central government’s response to the global financial crisis. Barred from borrowing through official channels but facing funding shortfalls to pay for infrastructure stimulus, local governments created off-balance sheet financing vehicles.

No LGFV has defaulted on a public bond, and sales in 2020 hit a record 4.4 trillion yuan, but cracks have started to appear. Chongqing Energy Investment Group Co. this year failed to repay 915 million yuan of commercial bills.

“It is only a matter of time before an orderly breaking of the implicit guarantee for public-issued bonds, including LGFVs,” said Wu Qiong, executive director at BOC International Holdings Ltd.

©2021 Bloomberg L.P.