China Builders Face Defaults as Cashflow Comes Under Pressure

China Builders Face Defaults as Cashflow Comes Under Pressure

(Bloomberg) -- Chinese property developers, the biggest junk bond issuers in Asia, are at growing risk of default as the coronavirus outbreak squeezes funding channels, according to PricewaterhouseCoopers.

In China, 90% of apartments are sold before construction is completed, making developers “reliant on pre-sales as part of their overall financing,” PwC said in a report released in Hong Kong on Thursday.

That strategy has taken a hit after large swathes of the country were locked down to stop the spread of the virus, shuttering showrooms and display units. Cracks have already appeared with Macrolink Holding Co., a Chinese conglomerate with exposure to property, defaulting on its onshore debt earlier this month.

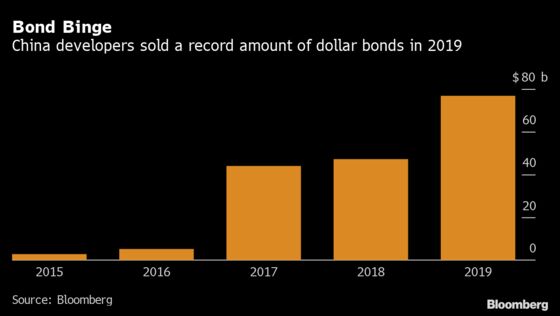

China’s builders raised a record $76.8 billion of dollar-denominated bonds last year, according to data compiled by Bloomberg. Investors have long held the assumption developers are systemically important and the government won’t allow a flurry of failures, and so far, most defaults have been among companies in other sectors. That could change, leaving investors and lenders exposed.

“There will be defaults,” said James Dilley, a Hong Kong-based partner at PwC. “There are certainly some weaker ones that are under a lot of stress, so I think there certainly will be more stress in the sector.”

In China, builders often use proceeds from pre-sales of one development to help finance other projects, and any disruption could lead to a breakdown of their financing cycles, according to the PwC report.

A reliance on short-term debt could also bite developers. Under current rules, Chinese builders are prohibited from using offshore bonds to fund land purchases and development, but the rules don’t apply to short-term debt with a maturity of 364 days or less, according to PwC.

“A handful of developers continue to use this loophole to secure short-term debt to finance bridging loans or working capital,” the report said. “Should the scope of the regulation widen, there would be further pressure on developers financing channels.”

However, the financial stress is also throwing up opportunities for private debt funds that lend to stressed companies.

“The coronavirus will mean there are more special-situation opportunities” because companies have liquidity concerns and real estate is a big part of that, said Dilley.

©2020 Bloomberg L.P.