China Developer R&F Delays Bond Maturity as Buyback Falls Short

China Builder Guangzhou R&F Set to Avoid Dollar Bond Default

(Bloomberg) -- Chinese developer Guangzhou R&F Properties Co. succeeded in delaying payment on a dollar bond due Thursday despite buying back only 16% of the note, underscoring the company’s liquidity shortage.

The firm will repurchase $116.4 million of a $725 million note under a tender offer, according to company filing to the Hong Kong exchange Tuesday. The company last month said it had planned to set aside about $300 million for the buyback. As part of the offer, bondholders agreed to extend repayment on the remaining principal by six months.

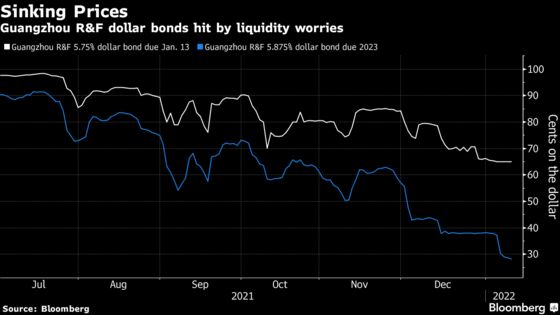

Its dollar bonds plunged last week when Guangzhou R&F said it might have “materially less” money than expected to buy back the note, citing delays in completing asset sales. Concerns about the company’s financial health have been growing in recent weeks as a historic credit crunch engulfing China’s property industry sent borrowing costs soaring and spurred defaults to a record high.

“The tender amount is much lower than the expected amount of $300 million, indicating lower cash available than investors expected,” according to Bloomberg Intelligence analyst Daniel Fan. While the “low ball” offer gives the firm six months, it may need to accelerate asset disposals to gain market confidence, he said. The company did not immediately respond to a request for comment Tuesday afternoon.

Property firms are scrambling to deal with imminent payments as falling sales further strain their finances. Prohibitively high borrowing costs in the offshore market mean many developers have effectively been unable to sell fresh dollar debt to roll over their upcoming obligations.

Buyback versus Extension

Guangzhou R&F is making payment on about 16% of the note’s principal. Funds used to settle the repurchase, related interest and consent fee total about $104 million, with some notes bought at a discount to face value. Investors who tendered their bonds to one of the two repurchase offers made by Guangzhou R&F “will be deemed to have voted in favor” of the six-month debt extension, according to the Dec. 15 exchange filing unveiling the proposal.

Holders also had the option to just support a six-month payment extension and receive no cash until July. None chose that, but now most of the $725 million note’s principal likely won’t be paid until at least then.

“The repayment ratio of the deal is too low for it to be considered a true tender offer,” according to Ting Meng, a senior credit strategist at Australia & New Zealand Banking Group Ltd. The capacity of Guangzhou R&F to repay the note now depends on its asset disposal progress as its basically lost its refinancing ability, she said.

A group of bondholders had engaged law firm Ropes & Gray LLP to hold talks with the developer about the tender, according to a Debtwire report dated Jan. 7 that cited two sources. Deutsche Bank AG is that group’s leading noteholder, the report said. Ropes & Gray and Deutsche Bank had no immediate comment when reached by Bloomberg News on Tuesday.

Fitch Ratings downgraded the borrower to C from B- in December due to the tender offer and consent solicitation, calling the effort a “distressed debt exchange.”

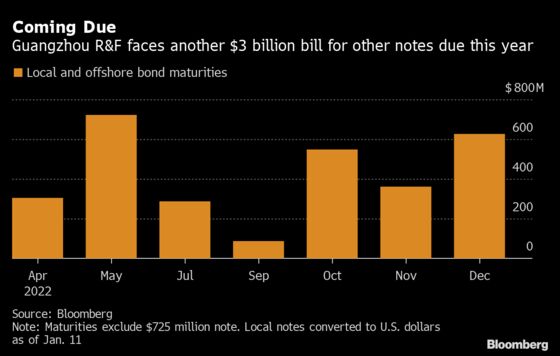

The builder is facing a series of key payment tests over the coming months, with 6.6 billion yuan ($1.04 billion) of local notes maturing in April and May as well as a $288 million dollar bond due July, according to Bloomberg-compiled data. Guangzhou R&F needs to repay or refinance some $3 billion in bonds this year excluding the note being repurchased and extended.

©2022 Bloomberg L.P.