China Bond Market Meltdown Brings World of Hidden Bills to Light

China Bond Market Meltdown Brings World of Hidden Bills to Light

(Bloomberg) -- China’s property developers are struggling to pay bills that many of their bond investors didn’t know were there in the first place.

Missed payments on off-balance sheet IOUs such as high-yield consumer products, secretive loans and private bond guarantees have rocked China’s credit market in recent weeks. Dollar bondholders are struggling to know their place in the repayment queue in the event of a default, forcing a dramatic repricing of risk that’s all but frozen the primary market for developers.

Kaisa Group Holdings Ltd. said on Thursday it failed to meet payments on wealth products, triggering a plunge in its bonds and shares. Fantasia Holdings Group Co. defaulted on a dollar bond last month only weeks after assuring it had sufficient working capital and no liquidity problems. Its failure to pay undermined the credibility of Chinese issuers just after Bloomberg reported China Evergrande Group was on the hook for an unknown bond issued by a separate entity.

“A lot of these companies have a lot of private credit,” said Philip Tse, director and head of Hong Kong and China property research at Bocom International Holdings Co. “It’s very hard to say who is safe now anymore because the whole market has lost its refinancing capacity.”

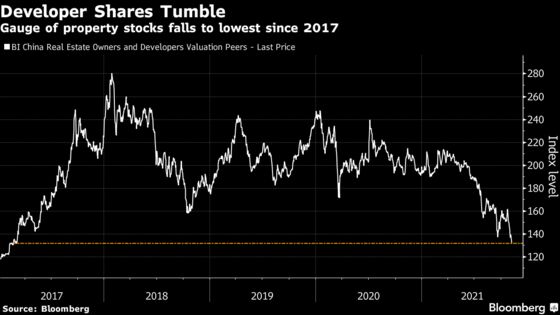

The repeated shocks have only worsened investor sentiment toward the sector. An index tracking developer shares slumped as much as 3.3% on Friday to its lowest level since March 2017. China Aoyuan Group Ltd. tumbled more than 15%. Shimao Group Holdings Ltd.’s dollar bond due 2026 sank about 10 cents to 71 cents on the dollar. The company said online speculation that it was in talks to extend payment on a trust product wasn’t true.

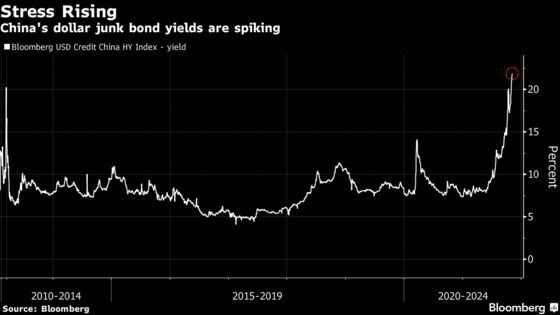

The rout has sent junk dollar bond yields toward 22%. That makes it prohibitively expensive for firms to tap the offshore market to repay debt as they did in the past. Other avenues for cash-raising are narrowing rapidly. Plunging home sales have curbed revenue, while finding buyers for asset disposals is proving challenging. Evergrande last month ended discussions to sell a controlling stake in its property-management business that would have raised about $2.6 billion.

Kaisa is seeking to sell property projects with a combined value estimated at 81.8 billion yuan ($12.8 billion), the South China Morning Post reported Friday.

Limited refinancing options increase the risk of developers failing to meet payments on debt -- hidden or not. One such blind spot for bondholders are the investment products sold and guaranteed by some developers to Chinese retail investors. The offerings typically have high annualized rates but are marked as safe. But knowing the exact value of outstanding products is difficult. Evergrande sold the products to more than 70,000 people across China, and set aside more than 80 billion yuan ($12.5 billion) in assets to repay them.

Kaisa’s exposure could be as high 12.8 billion yuan, local media reported this week.

Then there are undisclosed private bonds -- often issued by special-purpose companies with different names. Evergrande privately guaranteed a $260 million issue by Jumbo Fortune Enterprises, for example. Fantasia had $150 million of private bonds, according to Fitch Ratings, information that the credit assessor said it had only received from the company “in a recent call.”

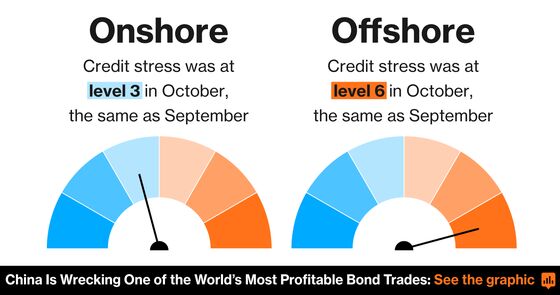

Whether Beijing will take measures to stem the rout is hard to gauge. Even as double-digit slides in some local property bonds triggered a flurry of trading halts this week, stress levels remain relatively low onshore. The stock market is far from bearish, with the Shanghai index down just 6% from a six-year high.

Inflows and unprecedented trade surpluses have helped keep the yuan steady near the strongest since 2018. China’s money market rates are calm, with the cost of overnight borrowing in the interbank market dropping below 2% -- far off credit crunch levels. The country’s government debt is rallying.

For bondholders and minority shareholders, the lack of transparency complicates their ability to assess risk and calculate the true value of a company’s assets. It is resulting in a sell-now, ask-later mentality that has started to infect securities of higher-rated issuers with no obvious liquidity problems.

“The Kaisa debacle suggests investors need to be aware not only of upcoming public debt payments but of obligations such as WMPs which may not be widely known,” said Andrew Chan, an analyst at Bloomberg Intelligence.

©2021 Bloomberg L.P.