Caterpillar’s Grim Outlook Bulldozes Wishful Thinking

(Bloomberg Opinion) -- As investors pore over every earnings report for the very latest read on the economy, Caterpillar Inc. provided fresh evidence that the slowdown in manufacturing is no blip.

The maker of bulldozers and mining machinery said Wednesday that its 2019 earnings would fall on the low end of its guidance range, snapping a streak of quarterly boosts to its outlook. Caterpillar’s pain points were similar to those that have routinely popped up in industrial companies’ results so far this second quarter: rising manufacturing costs, moderating demand and weakening confidence in the prospects for a second-half rebound. After a bizarre Tuesday turn in trading, when industrial companies including Pentair Plc and Sherwin-Williams Co. got resoundingly rewarded for cuts to their sales guidance, the glum outlook from an economic bellwether like Caterpillar seems to have shaken the market out of its reverie. Shares of Caterpillar slumped about 5% in early trading.

Caterpillar continues to expect a modest sales increase in 2019, but that assumes oil and gas markets recover toward the end of the year, and that dealers work through inventory buildups and are able to accept the price increases the company is banking on to offset increased costs. Those assumptions seem tenuous.

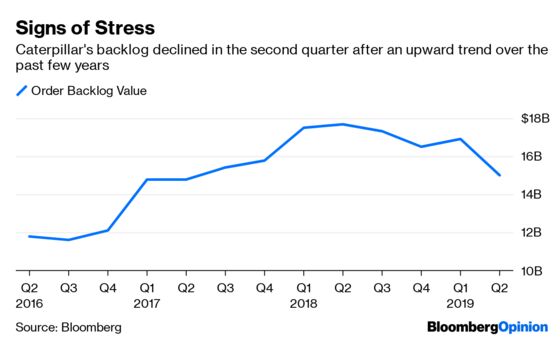

Dealers’ inventories of machines and engines climbed by $500 million in the second quarter, compared with a $100 million rise in the year-earlier period. But Caterpillar’s backlog slumped by about $1.9 billion relative to the first quarter, implying a softer demand environment. Meanwhile, sales of oil and gas equipment in North America declined in the second quarter, in part because of weaker demand in the Permian Basin. Halliburton Co. earlier this week announced an 8% cut to its North American workforce and said it would park unused fracking equipment rather than chase after market share. The oilfield services provider echoed Schlumberger Ltd.’s expectations for further sluggishness in the region in the second half of the year, even as international markets deliver robust growth. It’s also worth noting that the competitive pricing pressure in Asia that so spooked Caterpillar investors in the first quarter isn’t fading away. Sales of construction products slumped 22% in the region in the second quarter.

Caterpillar’s results came as IHS Markit’s euro-area manufacturing gauge signaled the steepest contraction in more than six years and Germany’s factory Purchasing Manager’s Index fell to the lowest level in seven years. A gauge of U.S. factories showed activity is hovering on the borderline between expansion and contraction in the lowest reading since 2009. The slowdown in this sector appears to be deepening and I remain skeptical that a quarter-point cut to interest rates by the Federal Reserve would be enough to motivate the kind of investment surge that could reverse that trend.

Elsewhere in industrials, aerospace has remained a haven this earnings season, with strong organic sales growth in the Honeywell International Inc. and United Technologies Corp.’s units that sell engines and aircraft parts. But it’s worth noting that Boeing Co.’s backlog is shrinking. The planemaker also reported results on Wednesday, and said its commercial backlog included more than 5,500 airplanes valued at $390 billion, down from more than 5,600 planes valued at $399 billion at the end of the first quarter. That’s likely at least in part a reflection of the fact that the embattled 737 Max is now in the fifth month of a global grounding following two fatal crashes. But should aerospace start to wobble, then we’re really in trouble.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.