Cash Piles, Hostile Bids Set Stage for a Wild Japan M&A Year

Cash Piles, Hostile Bids Set Stage for a Wild Year in Japan M&A

(Bloomberg) -- Japanese dealmaking was resurgent in the second half of 2020, with acquisitions dropping only slightly from 2019 to about $140 billion after the pandemic depressed deals in the first half of the year.

The momentum is likely to continue into 2021, M&A advisers say, with a pipeline of already agreed deals still to be announced. Pent-up demand, towering cash piles and external forces that could make 2021 among the most active years yet.

“Japanese companies are heading into 2021 with more cash and more firepower, having sold some non-core assets and consolidated their operations, and will turn again to outbound acquisitions” said Ken Lebrun, a partner at law firm Davis Polk & Wardwell in Tokyo. “When that’s going to be — first, second, or third quarter -- is not perfectly clear.”

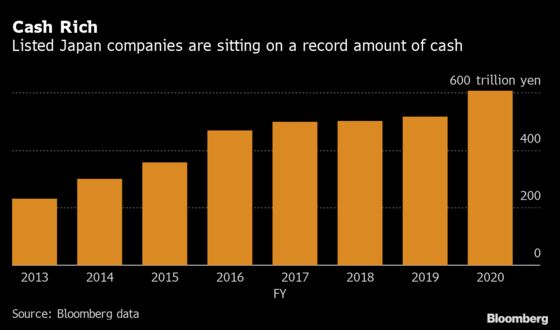

Japan has been the dominant Asian force for outbound M&A deals for the last three years, with firms spending $241 billion to buy up assets overseas, according to Bloomberg data. While the broader trends that have driven recent overseas M&A will likely hold, companies are also focusing inward, as they restructure assets and evaluate domestic competition. The Covid-19 pandemic also remains a wild card in assessing the overseas market.

Here are five themes to watch in Japanese dealmaking in 2021:

Domestic Housekeeping

Just as the pandemic put a stop to international travel, it also forced Japanese companies to look more closely at the domestic market and the state of their balance sheets. That means more companies are offloading non-core assets and weighing acquisitions of domestic competitors to gain market share in industries with high fragmentation.

“Companies are more open to selling their non-core business,” said Koichiro Doi, the head of Japan M&A at JPMorgan Chase & Co. Companies now are more willing to start talks, he said. “That’s a natural thing in the U.S. or European market, but had not been the case here.”

Hitachi Ltd. is among conglomerates shedding non-core assets, selling 60% of its overseas home appliance business to Turkey’s Arcelik AS for $300 million in December. The relative stability in Japan during the pandemic has also drawn more interest from overseas strategic suitors, notably Chinese firms, as well as funds, said Akifusa Takada, head of the M&A practice at the Baker McKenzie law firm in Tokyo.

Family Ties

“Parent-child listings,” where both the parent company and its subsidiary are publicly traded, are common in Japan but a rarity in other developed markets, and criticized by corporate governance experts. While investors have looked to the unwinding of these structures as a potential investment catalyst for years, 2020 was when they really took off.

Late last year the ultimate consolidation was realized with NTT Docomo Inc., Japan’s largest listed unit, being taken private by its parent Nippon Telegraph & Telephone Corp. Sony Corp. also bought out its financial unit after years of rumors and trading firm Itochu Corp. fully acquired its convenience store chain FamilyMart Co.

These types of deals made up the four largest acquisitions announced in Japan in 2020, and in 2021 investors are watching the likes of Fujitsu Ltd. and Toyota Motor Corp. which control multiple listed units. Bankers say these deals are an easier sell, as businesses are intimately familiar with their subsidiaries and more likely to take the plunge in uncertain times.

Overseas Caution

While activity is returning, large overseas purchases will likely remain rare if Japanese executives, who often value personal connections, are unable to travel for due diligence and in-person meetings, bankers said. The value of deals outside Japan fell by almost half in 2020.

With equity prices high worldwide due to central banks pumping money throughout the pandemic, valuations are trickier too. The largest overseas purchase by a Japanese business in 2020 was Seven & i Holdings Co.’s $21 billion acquisition of Marathon Petroleum Corp.’s gas-station business Speedway, with the deal primarily handled by its U.S. subsidiary.

“We have a lot of cash compared to the past, but it doesn’t mean we’re going to use it for M&A,” Olympus Corp. Chief Executive Officer Yasuo Takeuchi said at a briefing on Dec. 7, with the company holding a record 270 billion yen of cash and equivalents at the end of June.

Still, companies know they can’t sit on the cash forever, especially with more shareholders critically eying large cash piles, Lebrun said. A stronger yen could also help convince companies to snag relative bargains overseas.

Domestic Drama

Hostile bids for domestic rivals, once considered taboo in Japan, have gradually become normalized in recent years as corporate governance reforms promoting shareholder value take root.

Business leaders “seem highly attuned to the progress of corporate governance and stewardship, as well as the potential for pressure from activists,” Yoshihiko Yano, the head of Japan M&A at Goldman Sachs, said.

Last summer, Colowide Co. took control of restaurant operator Ootoya Holdings in hostile bid fueled by a family feud. In October, furniture giant Nitori Holdings Co. launched a bidding war for Japanese hardware-store operator Shimachu Co., outbidding a friendly rival offer.

It’s also worked in the other direction, with Mitsui Fudosan Co. becoming a white knight for baseball stadium operator Tokyo Dome Corp. and helping it fend off pressure from activist investor Oasis Management Co.

Dry Powder

Private equity has been eying Japan for years, and companies have begun to see the funds, once considered vultures, as a viable option for their non-core assets. But while 2020 dented private-equity activity, that only means funds are sitting on substantial amounts of dry powder for new transactions.

Carlyle in March raised 258 billion yen ($2.4 billion) for its fourth Japan buyout fund, more than double the previous fund. It’s been hiring new executives and publicly talking up the prospect of large deals in Japan over the past year. CVC Capital Partners said in April it aims to invest about 150 billion yen into the Japan market.

KKR & Co. is in the process of raising at least $12.5 billion for its next Asia fund, while Blackstone Group Inc. is reported to be seeking to raise at least $5 billion for its second Asian private equity fund. In August, Blackstone agreed to buy Takeda Pharmaceutical Co.’s over-the-counter drug business for 242 billion yen, its largest acquisition in Japan.

©2021 Bloomberg L.P.