Dismal Oil Prices Could Help Break Logjam in Canadian Energy Deals

Dismal Oil Prices Could Help Break Logjam in Canadian Energy Deals

(Bloomberg) -- The recent collapse in Canadian oil prices may have a silver lining.

Analysts and investors this year have been pushing smaller Canadian energy companies to combine into larger entities that are more efficient, can better allocate capital among multiple plays, and are more attractive to long-term investors. Despite those calls, the value of Canadian energy deals has declined this year, in contrast to a surge south of the border.

However, the recent plunge in heavy Canadian crude to less than $20 a barrel may spark a wave of consolidation, bringing buyers off the sidelines and causing “capitulation” among entrenched management teams of smaller producers, said Martin Pelletier, a portfolio manager at TriVest Wealth Counsel in Calgary.

“If I’ve got a good balance sheet, if I’m a well-run company with a process that works, why wouldn’t I look to take advantage of this environment?” Pelletier said in an interview. “There’s no better time than when management teams have been beaten up, investors have completely lost patience in the sector, oil prices are in the toilet and you’ve got a very large differential that may not be sustainable.”

Pelletier said his firm has moved 25 percent of its energy investments back into Canada -- after temporarily abandoning the country -- to buy into possible takeout candidates whose shares have been beaten into “deep value” territory by the widening differentials. He declined to disclose the size of the positions or any particular stocks he’s bought into.

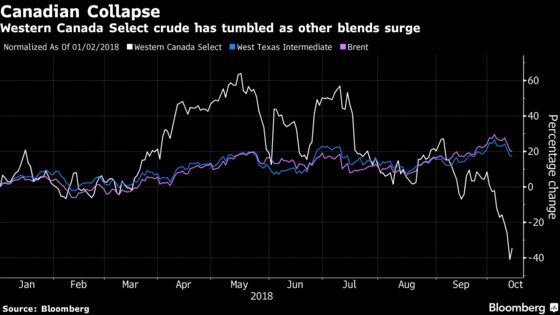

Crude Slide

Western Canada Select plunged below $20 a barrel on Thursday, the lowest price since February 2016. That widened WCS’s discount to West Texas Intermediate to $52.40 a barrel, the biggest discount on record in Bloomberg data back to 2008. WCS rebounded on Friday, narrowing the discount to $48.50.

That slide has weighed on Canadian energy shares. The S&P/TSX Energy Index dropped 7.8 percent this year through Friday, compared with a 1.3 percent gain for the comparable U.S. index.

The value of acquisitions involving Canadian energy companies has plunged as well, falling 16 percent to $55.8 billion in the first nine months of this year, according to data compiled by Bloomberg. Excluding $23.6 billion tied to Enbridge Inc.’s roll up of partnerships and other units, the total falls to $32.2 billion, which would be a 51 percent drop from the same period last year.

By contrast, the value of U.S. energy deals has surged 72 percent to $300.2 billion.

‘Getting Killed’

Cheap Canadian oil and stocks already are luring buyers. The Lundin family, a Swedish commodities dynasty, was explicit about the role that weaker Canadian prices played in International Petroleum Corp.’s C$600 million takeover of heavy oil producer BlackPearl Resources Inc. announced Wednesday.

“Right now, the Canadian oil patch is getting killed by the differential, which is enormous,” Lukas Lundin, IPC’s chairman, said in an interview. “But over time we think that’s going to change because there’s going to be some pipelines coming up. So if you survive this short-term pain, the long-term gain is very big.”

Still, despite the slumping oil prices, many acquisition targets may resist being taken over because they don’t want to sell with their valuations so depressed, said Rafi Tahmazian, who helps manage about C$1 billion in investments at Canoe Financial in Calgary. Management teams also may fear for their ability to find work again or start up a new company in an inhospitable market, he said.

Post-Deal Psychology

“In Canada, it’s a bit of a desert after you get sold,” Tahmazian said. “Psychologically, I think that’s a factor playing into this.”

Husky Energy Inc. cited its immunity to the widening differentials in its hostile cash-and-stock bid for MEG Energy Corp. Channeling MEG’s output into its refining system would maximize the value of each barrel of crude produced, benefiting MEG investors who currently are exposed to those weaker prices, Husky said.

While MEG may reject Husky’s bid and seek higher offers, the wider differentials may ultimately prompt investors to pressure MEG into accepting a deal, Pelletier said. And if similar scenarios play out across the industry, it could draw major investors back into the sector, rather than just short-term traders trying to play off the volatility, he said.

“To get the long-term money back in like it was in the old days, it’s going to take a fundamental shift,” Pelletier said. “There’s going to have to be some sort of catalyst, and it could be mass consolidation.”

--With assistance from Danielle Bochove.

To contact the reporter on this story: Kevin Orland in Calgary at korland@bloomberg.net

To contact the editors responsible for this story: Simon Casey at scasey4@bloomberg.net, Joe Carroll, Christine Buurma

©2018 Bloomberg L.P.