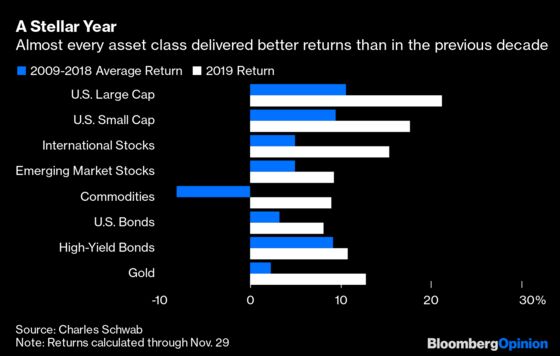

(Bloomberg Opinion) -- Traders and investors are tiptoeing nervously into 2020, after a stellar 2019 in which returns from almost every asset class outpaced their averages for the previous decade. The following charts illustrate why trading with cautious optimism might be the way to approach the coming year.

THE TREND IS YOUR FRIEND

Buying and holding anything from stocks to bonds to commodities proved to be a winning strategy this year.

To be sure, those stock market returns are flattered by the slump in global equities in the fourth quarter of last year. But rumors of the death of the bull market have been greatly exaggerated before, and the U.S. recession that doomsayers have been predicting is inevitable still hasn’t arrived. Yes, it’s late in the economic cycle. But maybe midnight is further away than many fear?

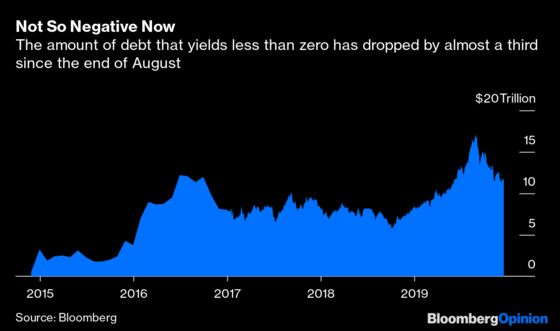

$11,769,509,000,000

The bad news: The fixed-income market is still plagued with more than $11.7 trillion of debt that yields less than zero. The good news: That total is down from a peak of more than $17 trillion at the end of August.

With Sweden abandoning its half-decade old policy of maintaining a negative interest rate this week, criticism of the unintended consequences of sub-zero borrowing costs is growing louder. Expect more soul-searching about reinstating the so-called zero bound in other central bank jurisdictions next year — perhaps led by the policy review instigated by newly installed European Central Bank President Christine Lagarde.

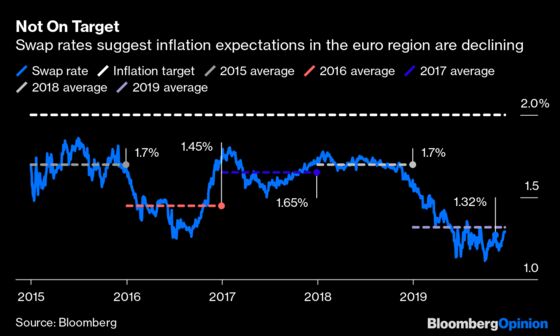

INFLATION IS AWOL

One key question that review will need to address is why inflation expectations in the euro region, as measured by the five-year forward inflation swap, continue to sink even as the ECB has restarted its quantitative easing program.

The future market is anticipating little chance of a change in the ECB’s key interest rate, which currently stands at -0.5%, for most of next year. But those lackluster inflation expectations are providing powerful ammunition to those who say negative rates are becoming less effective the longer they’re in place.

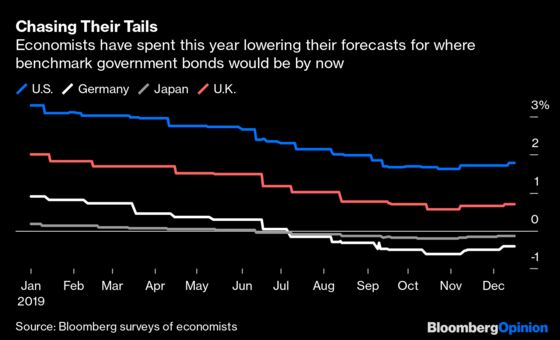

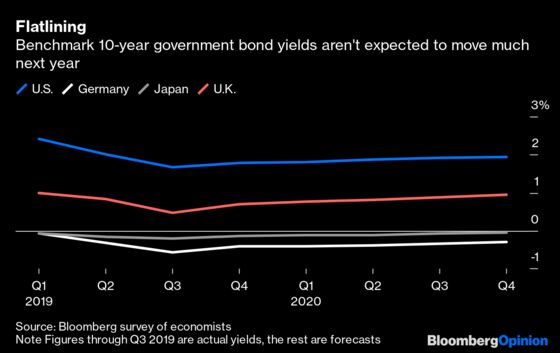

BOND BEARS RETREAT

Bond bears keep getting their noses whacked. At the start of this year, the consensus forecast of economists was for the 10-year U.S. Treasury to yield 3.3% by the end of December, compared with its actual current level which is a smidgeon above 1.9%. As this chart shows, however, bond yields have stubbornly failed to rise, prompting market soothsayers to keep chopping their estimates throughout the year.

So it’s perhaps understandable that the collective wisdom of the bond-forecasting crowd is predicting almost no movement in 10-year government borrowing costs in the coming year.

But it strikes us as awfully unlikely that yields will go absolutely nowhere in 2020 — even if we’re not brave enough to say whether higher or lower yields are the most likely outcome.

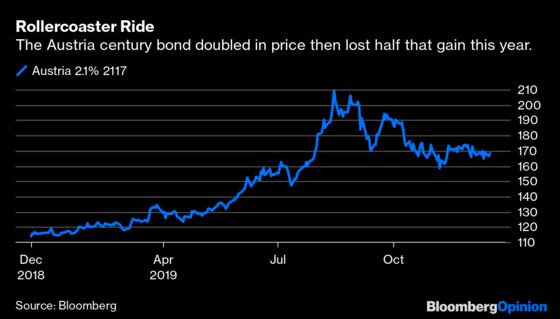

CENTURY BONDS

They are already a thing with countries as diverse as Austria and Argentina having issued 100-year bonds. They are on the agenda for 2020 for the U.S. where Treasury Secretary Steven Mnuchin is a notable advocate. Sweden and even the U.K. may follow suit. Super low global interest rates along with the global savings glut and aging demographics are tempting both corporate and sovereign issuers.

But while they are great for issuers, that is not always the same for investors. They are highly volatile, as the chart above shows.

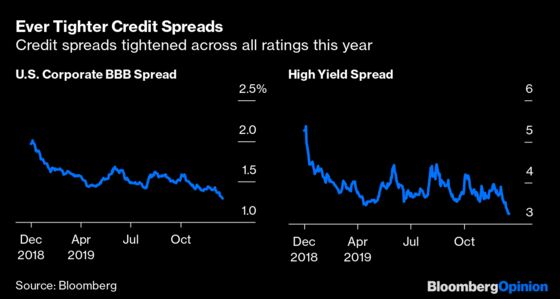

CREDIT RISK

Jeffrey Gundlach, chief investment officer of DoubleLine Capital, is not the only one worried about the bulking of investment grade corporates in the lowest-rated category of BBB. Credit spreads are the tightest since the global financial crisis.

Analysts at S&P Global Ratings say they see only a “moderate increase in defaults” for next year, with global credit markets enjoying “a weaker but still positive environment.” But if the U.S economy were to slump, the risk of multiple downgrades of BBB bonds to junk status could cause a stampede to safety as the hunt for yield quickly reversed.

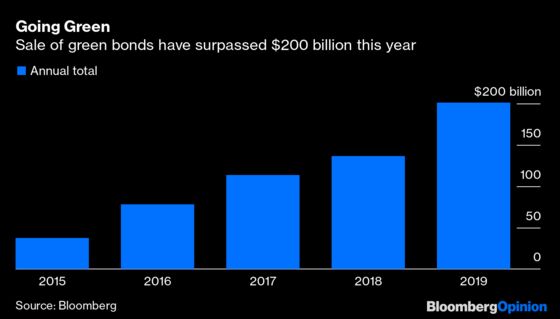

EVERYTHING’S GOING GREEN

Perhaps the most far-reaching development in 2019 was the rise of environmental concerns, culminating with Time magazine naming 16-year-old climate activist Greta Thunberg as its youngest-ever Person of the Year earlier this month. Global sales of green bonds — debt specifically designated to raise funds to combat the climate crisis — have soared by 47% this year.

There’s more to come. Germany plans to sell green twins alongside its conventional bonds, beginning in the second half of next year. Royal Dutch Shell earlier this month took out a $10 billion revolving credit facility on which the interest payments are linked to its progress on reducing its net carbon footprint.

And earlier this week, the European Union said it would come up with a list of categories and definitions for what it considers sustainable activities, known as a taxonomy, in an effort to put an end to so-called greenwashing and embed environmental goals in the finance industry’s activities. The future’s bright; the future’s green.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.