Buyout Titans Fire Up LBO Machine With $1.6 Trillion to Spend

Buyout Titans Fire Up LBO Machine With $1.6 Trillion to Spend

(Bloomberg) -- The biggest private equity firms in the U.S. are unleashing a flurry of new leveraged buyouts and debt-funded dividends, seeking to make up for lost time after staying on the sidelines for much of 2020.

From Blackstone Group Inc. to KKR & Co., firms have been pivoting from repairing the balance sheets of companies they own to hunting for new investments and realizing gains on businesses that performed well during the pandemic. North American buyout activity, which was 57% off last year’s pace at the end of June, is now only 32% behind, according to data compiled by Bloomberg.

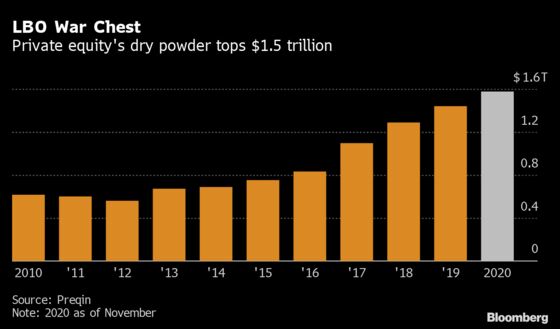

Of course, any number of adverse developments -- from a worsening economic outlook to setbacks in Covid-19 vaccine production -- could upend the trend. But with interest rates at record lows, seemingly insatiable demand from bond and loan buyers and almost $1.6 trillion of pent-up cash, industry watchers say the ramp up in deal making might just be getting started.

“Private equity firms don’t get paid to sit on cash,” said Harold Varah, global co-head of financial sponsors at RBC Capital Markets. “You’ve seen a tempering of the storm, a desire to deploy capital and a leveraged finance market that has recovered pretty remarkably. All the elements that you need for deal making are there.”

Private equity is hardly the only market that’s heating up again. U.S. stocks have continued to set records in recent weeks, while borrowing costs for much of corporate America are close to all-time lows. For some, it’s a sign of froth and complacency, especially amid the resurgence of coronavirus cases globally.

But for buyout executives, the Federal Reserve’s pledge to support credit markets and the availability of willing lenders have been enough to restore confidence.

“The credit markets are in fantastic shape, and most banks don’t have large exposures in their credit books,” said Rob Pulford, head of the U.S. financial and strategic investors group at Goldman Sachs Group Inc. “There is no doubt 2021 will be a very big year for sponsor M&A.”

It’ll be a stark turnaround from much of the first half of the year, when buyouts virtually ground to a halt amid the economic destruction of the pandemic.

Despite the slowdown, cash has continued to pile up as pensions and endowments flood into the asset class seeking higher returns. Private equity funds globally have amassed an unprecedented $1.6 trillion war chest, according to London-based research firm Preqin.

“Private equity is operating at a very frenetic pace,” said Jeff Cohen, head of leveraged and acquisition finance at Credit Suisse Group AG. “Many private equity firms have very specific goals with respect to how many deals they want to do per year and how much capital they want to put to work.”

Creative Solutions

Companies in sectors such as health-care services and technology have proven particularly attractive, as they’ve been more resilient to the pandemic and offer buyers and sellers more visibility about future performance.

Yet many are also commanding higher prices, forcing private equity firms to fund as much as half of the purchase with equity, according to bankers.

Still, debt investors are often showing up in droves, allowing buyout firms to walk away with attractive financing terms.

Blackstone this week received over $10 billion of demand for a $2.8 billion bond and loan offering to fund its planned acquisition of Ancestry.com Inc., according to people with knowledge of the deal, despite investor safeguards that were widely regarded as weak.

And last month, KRR raised over $1 billion to finance its acquisition of 1-800 Contacts, which was announced in September.

Representatives for Blackstone and KKR declined to comment.

“With the amount of dry powder available, we believe next year will be the ‘year of the sponsor,” said Randall Chafetz, deputy head of global corporate and investment banking at Mitsubishi UFJ Financial Group Inc. “The leveraged loan market came back strong, albeit months later than the high-yield bond market. This bodes well for financial sponsors who have been incredibly busy over the past few months.”

Beyond ramping up takeovers, private equity firms are also turning to more creative ways to book gains in their funds when outright sales prove difficult or undesirable -- including selling only partial stakes in companies that have performed well during the pandemic.

“We are seeing a lot of these transactions where sponsors are keeping a stake and rolling,” said Christopher Blum, head of leveraged finance for North America at BNP Paribas SA. “They get to show a monetization with the new valuation and keep that equity at work in a year when it’s been difficult to invest.”

Of course, traditional debt-funded dividends are still very much in vogue as well.

In July, KKR took a $560 million payout from Epicor Software Corp. as part of a recapitalization that made it easier for the company to be sold to Clayton Dubilier & Rice only a month later.

And two weeks ago KKR took a dividend out of Internet Brands Inc. -- the owners of web portals such as WebMD and Avvo -- by saddling the company with $400 million of additional debt.

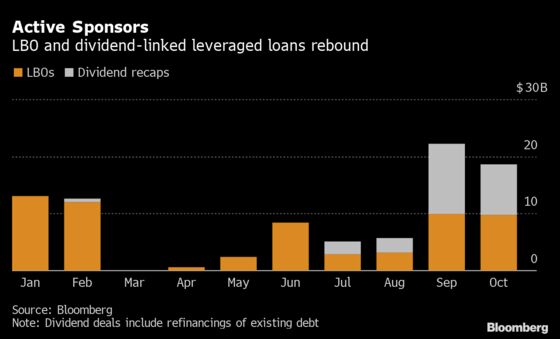

In all, buyout firms have issued roughly $30 billion of leveraged loans in the U.S. market that included dividend payments in the use of proceeds since July, according to data compiled by Bloomberg.

SPAC Demand

Even if equity or debt markets claw back some of their recent gains, buyout firms can count on a deep pool of capital available from non-traditional sources going forward.

Blank-check companies that raise money through a public listing before they identify a merger target have become potential acquirers of companies that private equity firms may be willing to shed.

“There is a new buyer in town,” said Pulford. “We are seeing SPACs becoming buyers of portfolio companies and that is creating an additional source of capital in the exit market.”

The vast amount of cash amassed by direct lenders could also come to the rescue of private equity if funding in the broadly-syndicated debt markets dries up.

For now, however, competition among lenders to finance buyouts is so intense that private equity barons are getting financing on terms that are in line with or even better than those before the Covid-19 outbreak.

Leverage ratios have surpassed six-times a measure of adjusted earnings in the last three months, according to Covenant Review. Meanwhile, bankers are taking more risk to underwrite LBOs by reducing the amount of wiggle room they have to sell the debt to investors.

“There’s a lot of private equity money on the sidelines and lots of demand for high-yield debt,” said Gershon Distenfeld, co-head of fixed income at AllianceBernstein. “We are getting set up for another LBO cycle.”

©2020 Bloomberg L.P.