Bulls Look to Alphabet Results to Keep Tech Rally Going

Bulls Look to Alphabet Results to Keep Tech Stock Rally Going

(Bloomberg) -- When Alphabet Inc. reports results after markets close on Monday, the company’s key advertising business is expected to show few signs of wear from privacy concerns that have weighed on internet companies recently.

The search giant’s fourth-quarter revenue is expected to jump 21 percent to $31.3 billion as marketers spent more on Google ads to reach consumers online. Last week, Alphabet shares rose to the highest levels since October after scandal-plagued rival Facebook Inc. beat Wall Street forecasts and soothed investor anxiety about a privacy backlash by consumers and regulators. Shares of the Mountain View, California-based company rose 1.1 percent at 10:25 a.m. in New York on Monday amid a broader rally in technology and and internet stocks that included Facebook, Netflix, Microsoft and Apple.

"Ad revenue growth deceleration came in better than feared for Facebook, which we view as a positive for Alphabet," Mark Mahaney, an analyst at RBC Capital Markets, wrote in a recent research note.

He’s expecting ad revenue from mobile search, YouTube and Google’s programmatic advertising services to drive growth in the fourth quarter.

Google and Facebook ads are still more relevant and effective than most other options because the companies collect so much information on activity across the internet and beyond. New privacy rules in Europe may have limited this data harvesting slightly, but that’s hit smaller competitors more than the two digital giants.

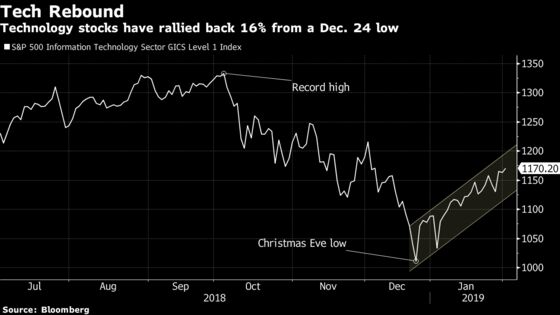

Alphabet’s report follows a big earnings week from industry heavyweights such as Apple Inc. The results have been mostly positive so far, helping extend a winning streak for tech stocks to a sixth week. Despite the gains, the sector has yet to reclaim its market leadership from 2018.

While Alphabet has invested aggressively in new businesses such as cloud services and autonomous vehicles, advertising still generates most of its revenue. Analysts expect sales growth to slow to 19 percent this year from 23 percent in 2018, according to data compiled by Bloomberg. So there’s more focus on profit margins and spending.

"The company’s highest-growth areas (mobile search, programmatic, YouTube, hardware, and cloud) have lower margin profiles than the traditional desktop search business, so we see continued margin degradation for the company as a whole," wrote BMO Capital Markets analyst Daniel Salmon in a recent note.

Alphabet’s swelling cash and other short term holdings totaled $106 billion at the end of the third quarter. That has Wall Street speculating about how the company might spend the money.

Robert W. Baird & Co. analyst Colin Sebastian says Alphabet is increasingly likely to make a large acquisition to boost its cloud business and compete more with Amazon.com Inc. and Microsoft Corp. Jefferies analyst Brent Thill said a new share buyback plan of as much as $15 billion is possible.

Just the numbers

- 4Q revenue ex-TAC estimate $31.32 billion (range $30.35 billion to $31.81 billion)

- 4Q GAAP EPS estimate $10.86 (range $9.83 to $12.13)

- 4Q operating income estimate $8.67 billion (range $7.81 billion to $9.52 billion)

Data

- 41 buys, 2 holds, 0 sells

- Avg PT $1,350 (20.6% upside from current price)

- Implied 1-day share move following earnings: 4.9%

- Shares rose after 6 of prior 12 earnings announcements

- GAAP EPS beat estimates in 9 of past 12 quarters

Timing

- Earnings release expected Feb. 4 after market close

- Conference call website

To contact the reporter on this story: Jeran Wittenstein in San Francisco at jwittenstei1@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Brad Olesen

©2019 Bloomberg L.P.