British Banks Brace for Deeper Slump by Pulling Mortgage Deals

British Banks Brace for Deeper Slump by Pulling Mortgage Deals

(Bloomberg) --

British mortgage lenders are beginning to batten down the hatches for an oncoming spike in unemployment.

HSBC Holdings Plc, Barclays Plc and Natwest Group Plc have tightened restrictions on home loans for risky borrowers as officials unwind pandemic-support efforts. Then there’s the renewed prospect of a no-deal Brexit, threatening to deepen what’s already the worst recession in centuries.

“Life could get very difficult,” said Mick McAteer, a former board member of the U.K. Financial Conduct Authority and now a housing advocate. “I’m not sure people fully understand that we are just coming to the end of the ‘emergency’ phase of the Covid crisis.”

By moving to tighten mortgage lending, banks will dim one of the few economic bright spots as Prime Minister Boris Johnson struggles to contain isolated hot spots. Home prices have rallied since the end of lockdowns, driven by pent-up demand and cuts in transaction taxes. Values rose the most in four years in August.

The headlines mask the looming risks in the wake of a fight for mortgage market share that led to looser home-loan criteria in the past three years. One in six mortgage holders has already paused their repayments. Regulators, meanwhile, say they don’t know how much was loaned to those most at risk of losing their jobs in the downturn: the workers in the booming gig economy.

“Do they really know how much people borrow and to what extent this is risky? The answer is no, they don’t,” said Alla Koblyakova, a lecturer at Nottingham Trent University who studies the mortgage market. She was surprised to find that some borrowers spend 55% of their household income on home-loan repayments.

Barclays’ changes stemmed from its desire to be a “responsible lender,” a spokesperson said. Spokespeople for HSBC and Natwest said they continually review their mortgage offerings.

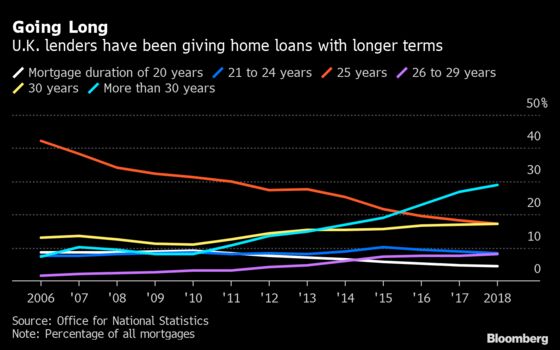

The economic downturn will also be the first test of lenders’ decision to roll out longer-term mortgages to help borrowers pay record house prices. Home loans of more than 30 years rose to 29% of the market in 2018 from about 19% in 2015 and 8.2% in 2010 to reduce monthly repayments.

Bloomberg Economics forecasts unemployment could more than double to 8.5% by the end of the year. The rise in joblessness will also put downward pressure on incomes, making it harder for those who are employed to make mortgage payments.

The biggest decline in weekly wages from January through June was construction’s 11% drop and a 6% fall in the category that includes retail and restaurants, two of the industries most likely to use flexible workers, government data show.

A desktop stress test from the Bank of England suggested house prices may fall 16% in the virus-wracked economy. Banks would face impairments of just 4 billion pounds ($5.3 billion) in that scenario, because their balance sheets are more resilient than during the financial crisis, the analysis showed. The BOE has also used tools to limit risky lending, through affordability tests and retrictions on high loan-to-income lending.

Mortgages for workers without guaranteed hours were common before the pandemic, with banks charging interest rates in line with more secure borrowers, Ray Boulger, senior mortgage technical manager at mortgage broker John Charcol, said earlier this year. Banks and customer-owned lenders advanced as much as 95% of the house price to the borrowers, he said.

Almost two million people “are on zero-hours contracts, and rely on them for their income. The flexibility suits their lives and their lifestyle, and their needs shouldn’t be ignored,” Aaron Shinwell, head of mortgages and savings at HSBC U.K., said 12 months ago when the bank relaxed some requirements to qualify for a home loan. The lender also increased the number of payslips an applicant required to three from one.

Pulling Products

The bank’s average LTV ratio on new mortgage lending in the U.K. rose to 59% in the first half, 10 percentage points higher than the previous six months even as the pandemic shut down the property market for a chunk of the period.

After the country’s deepest recession on record and with a no-deal Brexit looking more likely, banks have decided against passing on cuts to benchmark rates. Meanwhile, the number of products offered to first-time buyers with small down payments has fallen 92% to 62 since March, according to data compiled by comparison website Moneyfacts.

| Median Mortgage LTV% | |||||

| Employed | Self-employed | Retired | Other | Unknown status | |

| 2018 | 72.8% | 62.6% | 26% | 43.4% | 42.2% |

| 2019 | 73.7% | 64.1% | 26.1% | 42.4% | 40.2% |

| Q1 2020 | 72.5% | 61.8% | 25% | 45.7% | 44% |

The Bank of England, the FCA and industry lobby group UK Finance say they do not compile data on home loans to flexible workers. Fitch Ratings Inc. and S&P Global Inc. said they do not collate the number of zero-hour contract workers in mortgage pools. Moody’s Investor Service declined to comment.

The pandemic is already throwing up some surprising home loan data. One in two borrowers in some prime residential mortgage-backed securities took a payment holiday compared with an average of 28% for subprime pools, data compiled by Moody’s in July show.

Additionally, it’s not the riskiest borrowers on paper who are taking a mortgage holiday. The average LTV balance of a Barclays customer using the program is 57%. At Lloyds Banking Group Plc it’s just 52% for those extending payment holidays.

“We don’t know at the loan level what’s happening,” said Koblyakova. “The risks might be underestimated for certain groups of households.”

©2020 Bloomberg L.P.