Briggs & Stratton, Stalwart of Suburban Lawns, Goes Bust

Briggs & Stratton, Stalwart of Suburban Lawn Culture, Goes Bust

(Bloomberg) -- Another icon of post-war American suburbia went bust as Briggs & Stratton Corp. declared bankruptcy, felled by weak sales, too much debt and a final push over the edge from the coronavirus pandemic.

The world’s biggest maker of gasoline engines for outdoor power equipment sought protection from creditors in a St. Louis bankruptcy court on Monday, citing debts of more than $1 billion. The filing included a $550 million bid for the company from KPS Capital Partners, a New York private equity firm, which promised to keep Briggs & Stratton in business without the crushing debt that plagued the century-old company.

KPS, whose portfolio includes TaylorMade golf clubs and Life Fitness gym equipment, specializes in manufacturing companies. It agreed to serve as the lead bidder in a court-supervised auction, setting a minimum price for any eventual sale, and it’s contributing to a bankruptcy loan that will keep Briggs & Stratton operating, according to a statement. KPS said it has already negotiated a new contract with the United Steelworkers of America.

If you’ve ever pushed or driven a lawn mower in your backyard or wielded a snow-blower, chances are the engine was made by Briggs & Stratton, which supplied brands such as Craftsman and Snapper.

If you hired a lawn service instead, some of its equipment probably had Briggs & Stratton components, too; it sold products to Deere & Co., MTD Products Inc. and Husqvarna Outdoor Products Group. The Wisconsin-based company’s product lineup also includes power generators and pressure washers, made by 5,200 employees as of the end of last year. It employed more than 9,000 in 2005.

The company has been pressured by falling sales, tied in part to the pricing power of mass merchandisers such as Home Depot, Lowe’s and Walmart, according to regulatory filings. It didn’t help that Sears Holdings Corp., which accounted for a large chunk of sales, went bankrupt in 2018. Briggs & Stratton said it also faces competition from big rivals such as Honda Motor Co. and Kawasaki Heavy Industries Ltd.

On top of that, Briggs & Stratton’s news release about the bankruptcy cited pressures from the Covid-19 pandemic, which “have made reorganization the difficult but necessary and appropriate path forward to secure our business.”

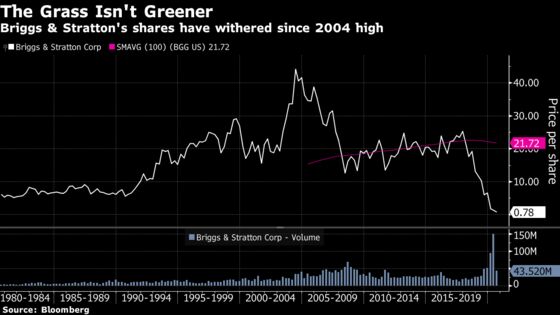

The company, led since 2010 by Chief Executive Officer Todd Teske, is headed for a third straight annual loss, and the stock -- which topped $40 in 2004 -- has been selling for less than 80 cents.

Trading was halted Monday while the news was disseminated, but at $550 million, KPS’s offer wouldn’t be enough to cover all the outstanding obligations, which means that shareholders could be wiped out. The company’s junior bonds would have to be paid off before stockholders get anything, and those notes were quoted recently at about 10 cents on the dollar -- a sign that full repayment is unlikely.

Acquisitions Planned

“KPS intends to grow the new Briggs & Stratton aggressively through strategic acquisitions,” said Michael Psaros, co-founder and co-managing partner of KPS, in a statement. “The new Briggs & Stratton will be conservatively capitalized and not encumbered by its predecessor’s significant liabilities.”

The offer by KPS would need court approval and could still be topped by a rival bidder for the company, whose headquarters is in Wauwatosa, less than 10 miles from downtown Milwaukee.

Briggs & Stratton said in its statement that it lined up $677.5 million of debtor-in-possession financing that will help fund operations during the court reorganization. KPS said it’s contributing $265 million of that sum.

Banks including Wells Fargo & Co., Bank of America Corp., BMO Harris Bank and PNC Business Credit will provide exit financing for a new company created through the acquisition of Briggs & Stratton’s assets, according to a spokesman for KPS.

Briggs & Stratton began as an informal partnership in 1908, initially focused on auto parts under founders Stephen F. Briggs and Harold M. Stratton, according to the company’s website. (“Briggs was the inventor and Stratton was the investor,” the company said.) They ventured into areas such as engine-powered bicycles, electric refrigerators and coin-operated paper towel dispensing machines, and their company blossomed alongside American suburbs dotted with single-family homes and grass-covered yards.

Global Reach

KPS, based in New York, runs the KPS Special Situations Funds with more than $11.4 billion of assets. The firm said its portfolio companies run 150 manufacturing facilities in 26 countries with about 23,000 employees.

Kirkland & Ellis is legal counsel for KPS. Briggs & Stratton previously hired Houlihan Lokey Inc. to advise it on strategic options including refinancing its debt, selling assets and cutting costs.

The case is Briggs & Stratton Corporation, 20-43597, U.S. Bankruptcy Court, Eastern District of Missouri (St. Louis).

©2020 Bloomberg L.P.