Brexit Uncertainty Could End for London’s CLO Managers With Q&A

Brexit Uncertainty Could End for London’s CLO Managers With Q&A

(Bloomberg) -- London’s CLO managers are set to get clarity from regulators about how skin-in-the-game rules will work after Brexit.

In the arcane world of securitization regulation, Brexit has thrown doubt onto whether U.K.-based managers of collateralized loan obligations can keep being “sponsors” or have to fall back on the “originator” designation meant for managers from outside the Europe Union.

It’s a critical difference in the early-stage mechanics of building a CLO, and a key issue for the market given most of the 44 managers are U.K. regulated entities. Few, if any, CLO managers will want to risk getting it wrong given that failure to comply with the EU’s new securitization regulation may even lead to a criminal conviction for both the CLO manager and the investors in the transaction.

Christian Moor, a policy officer at the European Banking Authority with a focus on capital markets and structured finance, told Bloomberg News he expects there will be a “question-and-answer” published by the end of the year to clear up the uncertainty. A Q&A is an online database in response to queries from the market to ensure consistent and effective application of the new rules, though they are not legally binding.

Brexit Switch

Risk-retention rules were introduced in the wake of the financial crisis and are laid out in the Capital Requirements Regulation (CRR). Managers must retain 5 percent of a transaction for the life of the vehicle. MiFID regulated entities or investment firms can do this as a “sponsor,” while those from outside have to use the “originator” method, requiring them to take an additional step of originating a certain portion of assets onto their own balance sheet before selling them on to the CLO vehicle.

U.K. managers can currently qualify as sponsor entities by passporting into the EU regime, but after a Brexit -- where the U.K. loses access to the single market and is unable to establish an equivalency regime -- these managers will lose their passporting rights, shutting down the sponsor route for them.

Managers have so far coped with the uncertainty over which option to take by inserting language in their documentation to allow for a switch, or by changing their method of risk retention. That sparked a shift away from the sponsor option to originator CLOs, and this year’s issuance shows the European market split about 50:50 between the two structures.

Originator CLOs Take Hold in Europe After Brexit Vote: Analysis

For some, the originator route is the obvious option to take. It’s tailor-made for non-European retainers, accepted by the market and relatively straightforward to comply with, according to John Goldfinch, partner at Milbank Tweed Hadley & McCloy LLP, a specialist in structured finance law.

“Absent more definitive regulatory guidance, our view is that this is much the better path for non-European firms to tread,” Goldfinch said.

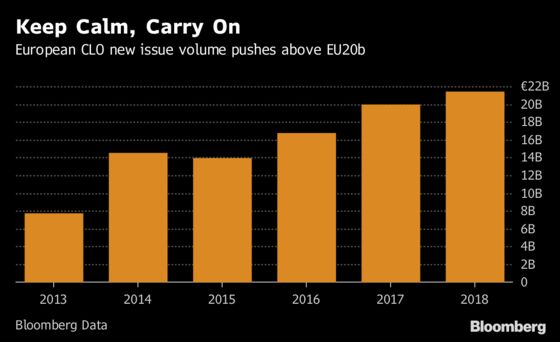

And however inconvenient it may have been to switch to originator structures, Europe’s managers have issued more than 20 billion euros ($23 billion) this year, a new record, taking the size of the outstanding post crisis market to nearly 90 billion euros, according to data compiled by Bloomberg.

Lawyers Divided

To add to the complications, Europe’s new securitization regulation will apply to new securitizations established after Jan. 1, 2019, and has left lawyers debating what the section on risk retention means.

CLOs Future-Proof Themselves Against Hard Brexit, But Not STS

The clause being argued over updates the definition of a sponsor for the new rules, but is ambiguous enough to leave room for debate as to whether the new rules could keep the sponsor route alive for London-based managers post Brexit.

“The position under the regulation is clear, as is the underlying intention of the authorities to expand the scope of the sponsor definition to non-EU firms, as compared with the position under the current regime,” said Franz Ranero, partner at Allen & Overy LLP, with expertise on CLO law.

But it’s a gray area that has caused other firms to adopt a more cautious view even if they would like to see the wider inclusion of non-EU countries in the sponsor definition. They worry that the reading by those on the other side of the debate is inconsistent with the intention of the MiFID definition of sponsor.

“The whole point of MiFID II is to regulate managers that are operating within the EU while providing a narrower set of provisions regulating third country firms operating in the EU,” said Chris McGarry, partner at White & Case LLP.

“If regulators had meant for the new sponsor definition to include third country firms they would have said so as they did when explicitly expanding the definition to cover banks outside of the EU,” McGarry said.

Breaking The Impasse

While EBA’s Moor acknowledges the wider sponsor remit under the new rules, he is also aware of the confusion created by the drafting. The Q&A is intended to help address these layers of uncertainty.

“Compared to the sponsor definition under the current CRR regulation, which states that sponsors have to be MiFID regulated entities, the definition under the securitization regulation is wider,” Moor said.

Moor added that there is “confusion” because in the new regulation the reference to “investment firms” does not address their location, whether situated in the EU or not. It does, however, cross-reference the MiFID II definition of investment firm, according to Moor.

This opens up a debate as to whether such firms, including CLOs, should be MiFID regulated or if the clause is merely laying out the general parameters of an investment firm--and so allowing for them to be located in a non-EU country.

To contact the reporter on this story: Sarah Husband in London at shusband@bloomberg.net

To contact the editors responsible for this story: Tom Freke at tfreke@bloomberg.net, Charles Daly

©2018 Bloomberg L.P.