Breakups Usher In a New Era of Corporate Conglomerates

"The dinosaurs are back, but they are different," New York University professor Baruch Lev says.

(Bloomberg) -- Conglomerates are dead. Long live conglomerates.

General Electric Co., Johnson & Johnson and Japan’s Toshiba Corp.’s breakups this week may have signaled to many the last gasp of a bigger-is-better ethos that’s been losing favor for decades. Activists and corporate governance advocates cheered in what seemed to have marked the end of an era placing blind faith in an almighty CEO overseeing an opaque web of unrelated businesses.

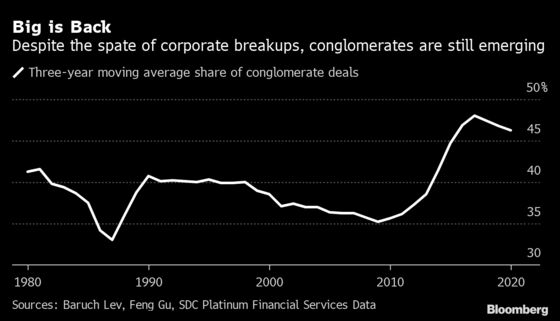

But focus may not really be back in fashion, according to Baruch Lev. The New York University professor has analyzed more than 36,000 mergers and acquisitions in recent decades and found -- to his surprise -- that so-called conglomerate, or unrelated, acquisitions over the past five years accounted for nearly half of all deals. That’s up from between 35% and 40% in the two decades before.

“The dinosaurs are back, but they are different,” Lev said. “They’re now the fashionable, high-growth tech and media companies venturing far out of their core business to acquire unrelated enterprises.”

The technology arena has been driving these transactions and created what University of Michigan business professor Jerry Davis calls “neo-conglomerates.” Among them are Facebook parent Meta Platforms Inc., Tesla Inc., Amazon.com Inc., and Google parent Alphabet Inc.

On Friday, J&J, the maker of cancer treatments, mouthwash and Tylenol, said it will break itself up into two public companies, one focused on drugs and medical devices, and the other on consumer products. That came a day after Toshiba said it would split into three companies, responding to pressure from activists. Earlier in the week, GE also unveiled plans to split into three companies, breaking up of the iconic manufacturer founded by Thomas Edison.

The new breed of conglomerates, fueled by coders and cheap capital, now command the same awe and respect in management and investor circles that Jack Welch’s GE did in the 1980s, or Harold Geneen’s ITT Corp. did in the Mad Men era.

In its heyday, GE made everything from toasters to turbines, while ITT invented the idea of the international conglomerate, with disparate assets that rented cars, baked bread and wrote insurance policies. Today, Amazon sells groceries and cloud services, runs a cargo fleet and creates streaming TV programs. In addition to its cars, Tesla makes electric batteries and sells insurance.

Follow the Money

What Amazon and its ilk do much better than yesteryear’s conglomerates is skate quickly to where the profit is, whether that’s automation, social commerce, sustainability or even the much-hyped metaverse, which will likely influence the future of work and the role of traditional offices.

“It’s not that combining businesses isn’t important for today’s conglomerates,” said Ron Adner, a strategy professor at Dartmouth’s Tuck School of Business, citing Amazon’s business as an example. “The thing that makes them look different is they don’t compete along traditional industrial lines. So you can interpret the current breakups as a concession that the old models aren’t working.”

While GE, J&J and Toshiba were undone by activist pressure, lawsuits and evolving industry dynamics, the tech firms could get upended by government regulators in the U.S. and Europe who are increasingly worried about their growing clout. Last week, the U.S. Federal Trade Commission hired a former Google executive as an adviser, bringing a technology activist to aid its regulatory push. They also face resistance from within, as rank-and-file staffers now openly express concerns about the dangers of their employers’ AI-powered decision making.

Investors gave a muted response to last week’s breakups, in contrast to the enthusiasm that greeted similar moves from IBM and Hewlett-Packard Co. in recent years. Shares of GE are down 1.7% since the split was announced. J&J rose just 1.2% on Friday and was little changed Monday.

Copycat Deals

Meanwhile, this week’s breakup announcements could spark copycat moves, illustrating a phenomenon that sociologists call “organizational isomorphism” -- which basically means keeping up with the Joneses. “We look over our shoulders and do what the other guy is doing,” said Michael Useem, a management professor at the University of Pennsylvania’s Wharton School.

Analysts cited Post-it maker 3M Co. as a prime candidate for a possible shakeup, as its shares have lagged behind those of other industrials due to struggles with intense inflationary pressures. The stock’s 5.1% gain this year is only a quarter of the advance in the S&P 500’s industrial sector index. 3M declined to comment.

“They just have such a sprawling enterprise that it begs for simplification, and frankly they’ve been under-performing,” said RBC Capital Markets analyst Deane Dray.

©2021 Bloomberg L.P.