Breakout You Need to Watch Has Zero to Do With Pot: Taking Stock

Breakout You Need to Watch Has Zero to Do With Pot: Taking Stock

(Bloomberg) -- We may have hit peak mania, or insanity if you prefer, with the pot stocks on Wednesday, with everyone and their mother either watching the madness unfold on their trading screens, trying to get a borrow to short the stock followed by relief that they never were able to short followed by wishing they were short all along, feeling major FOMO, or contemplating whether what they were witnessing was more like the crypto craze of last year, the freakouts from the rare earths (remember Molycorp?) to alternative energy and 3D printers at various points over the past 15 years, the dot com bubble, the tulip bulb crash of the 17th century, and so forth.

But this isn’t going away anytime soon -- for one, Tilray is back up ~6% in early trading (and vacillating in and out of positive territory) after yesterday’s bewildering ride.

The poster boy pot stock still has a massive market value versus its projected sales (~$20 billion market cap as of yesterday’s close vs estimated $42 million revenue for this year), as does Canopy Growth, Aurora Cannabis and some of the other pure plays out there. There are deals with legitimate stalwarts of the consumer industry that are being patched together, there are approvals from the DEA allowing for the import of medical marijuana to the U.S., and there is an enormous catalyst on the horizon with the Oct. 17 Canada roll out.

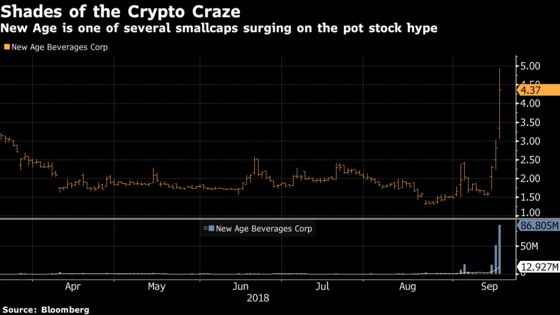

Plus we’re seeing some microcaps creep into the cannabis and cannabidiol (CBD) game, or at least announcing via the press machine that they’re looking to get involved in the industry, which in turn is sending their over-the-counter shares to the moon.

Just look at the one-day charts of MJ Holdings (MJNE) and Alkaline Water (WTER) after their respective statements yesterday, or the multi-day chart below for New Age Beverages (NBEV) to see what I mean -- this last point is shades of Long Island Iced Tea becoming Long Blockchain, or the swift boom to bust of little-known crypto stock LongFin from seemingly eons ago, even though it all took place just last December.

OK, Enough With the Weed

So there are other things going on in this market besides pot, even though it might not seem like it, like maybe the big breakout mentioned in the next section.

One thing that bears mentioning is Red Hat getting slammed almost 5% last night after disappointing for the second quarter in a row on the revenue front. Today’s move doesn’t seem as harsh as the last one, where Red Hat’s 14% plunge took down a huge chunk of tech and caused a stalling out of a rally in momentum stocks.

We probably won’t see that happen again this time, as the QQQs are trading up small in early trading, but it’s definitely something to watch, considering the recent unimpressive action in some of the large-cap tech winners (AMD, Salesforce, Nvidia, Microsoft all negative in the past two days) and ahead of Micron earnings tonight.

A Long-Awaited Breakout

While you and the rest of your colleagues were watching the Tilray pot stock spectacle tick for tick (and halt for halt) with jaws agape, a potentially seismic trade in the market went down involving several sectors that are known to move in lockstep with any giant shift in Treasury yields.

The upside move occurred in the bank stocks, which led all GICS Level 2 sub-sectors on the S&P 500. Citi, JPMorgan, Bank of America, and others rose anywhere from 2.5% to 3.3% while the KBW Bank Index, or BKX, had its largest gain in over two months and broke above three major moving averages in the 50-day, 100-day and 200-day.

The reason traders bid up the space can be attributed to one thing: Yields.

Specifically, it’s the two-day ~8 bps surge in the 10-year to above the closely-watched 3.00% mark (peaked at 3.09% on Wednesday to its highest level since May) that is giving the market more confidence in a sustained upside gap for the sector. The move coincides with a slight reversal in the flattening of the yield curve, which is something we’ve seen very little of so far this year. The steepening is being attributed to everything from a re-pricing of Fed hike odds to a more optimistic view of the economy and, amazingly, increasing prospects for a resolution in the trade war.

On the flip side, the rotation into the banks meant money probably flowed out of some of the more yield-sensitive sectors, which explains the heavy selling that took place in the utilities (-2.1%), telecom (-1.4%), and the REITs (-0.9%). These groups are also viewed as the most defensive sectors in the market, and there was a notable move into them at the beginning of the month when trade war jitters were intensifying -- this all has the makings of a continued unwind out of these sectors if those trade worries ease and the 10-year establishes a hard concrete floor at the 3% level.

Now to be fair, we’ve seen this movie before. The banks have attempted several breakouts this year, like in May when the 10-year hit upwards of 3.11%, but the failure for yields to remain above 3% almost immediately stymied any rally -- the BKX has essentially gone nowhere in the past six months (the index is down 2.6% in that time frame vs the S&P 500 up >7%) -- and the likes of Jamie Dimon predicting rates roaring to above 4%, and even possibly 5%, hasn’t had any sort of effect on the group.

The next few days will be telling, especially leading up to the Oct. 12 kickoff to third-quarter earnings season when JPMorgan, Citi, and Wells Fargo report.

Notes From the Sell Side

Here’s what the biggest Amazon bull is saying about our scoop from yesterday about the company planning up to 3,000 cashierless stores by 2021 (this moved all sort of stocks, from the grocery chains to pharmacy names, Walmart, Target, and hedge fund hotel Impinj): Morgan Stanley’s Brian Nowak, who has a Street high price target of $2,500 on AMZN, pins the potential investment in the "Go" stores at ~$3b, though sees the grocery, pharmacy, data and behavior modification benefits as "far larger"

The big bear on GE, JPMorgan’s Steve Tusa, is at it again. He’s reducing his price target from $11 to a Street low $10 because of this: "The impact on ’asset value’ from a failure at GE’s US H-frame launch customer, while tough to estimate, represents a negative development for a company that has little wiggle room for more ’shoes to drop’"

Baird upgrades Caterpillar, Manitowoc, and Sun Hydraulics to outperform on a combo of good fundamentals and inexpensive valuation; notes steel prices have started to roll over with OEMs enacting outright price increases (the three aforementioned names along with Deere) instead of surcharges likely to benefit.

Following Morgan Stanley’s big upgrade of the oil services earlier this week, we now have RBC upgrading the offshore drillers on increased activity and sanguine company commentary, with Diamond Offshore, Noble Corp., Rowan, and Transocean all going to outperform. The firm is also slashing its ratings on a couple of fracking names (U.S. Silica and Covia to sector perform) as the sand supply curve is overshooting demand. They’re also downgrading ConocoPhillips, a couple of Canadian names (Canadian Natural, Trican Well), and upgrading Helmerich & Payne.

Stifel boosted its price target on Square to match the Street high at $100 as the ongoing penetration of larger merchants, the company’s new partnership efforts, and its emerging financial services offerings (Cash App) will lead to higher growth levels than previously forecasted.

And an Nvidia bull is throwing a little caution in the wind, with Morgan Stanley’s Joseph Moore talking about he wouldn’t expect near-term upside from gaming ("Turing ramp may be a slow burn") but he still likes the stock: "As review embargos broke for the new gaming products, performance improvements in older games is not the leap we had initially hoped for; still, new features such as ray tracing and DLSS will matter more longer term."

Tick-by-Tick Guide to Today’s Actionable Events

- 7:00am -- DRI, THO (roughly) earnings

- 7:30am -- DOVA investor day

- 8:00am -- ATH investor day

- 8:30am -- Philadelphia Fed

- 8:30am -- DRI earnings call

- 9:00am -- Gap CEO Art Peck on Bloomberg TV

- 9:30am -- Lilly’s Elanco (ELAN) IPO expected to start trading after the open

- 10:00am -- Existing Home Sales, Leading Index

- 10:30am -- EIA natgas storage

- 10:30am -- WK analyst day

- 11:40am -- Eventbrite (EB) CEO Julia Hartz on Bloomberg TV

- 12:10pm -- CVS CEO Larry Merlo on Bloomberg TV

- 12:30pm -- Tiger Woods tees off at the Tour Championship

- 1:20pm -- APA CEO John Christmann on Bloomberg TV

- 4:00pm -- MU earnings

- 4:05pm -- UNFI, SCS (roughly) earnings

- 4:30pm -- MU earnings call

- 6:00pm -- RMD healthcare meeting

- 8:20pm -- Jets at Brown (-3)

- Tonight -- IPOs scheduled to price: Farfetch (FTCH), Eventbrite (EB), Remora Royalties (RRI), Y-mAbs Therapeutics (YMAB)

To contact the reporter on this story: Arie Shapira in New York at ashapira3@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, Steven Fromm

©2018 Bloomberg L.P.