Brazil Investment-Grade Survivor Eyes Bolsonaro’s Asset Sales

Brazil Investment-Grade Survivor Eyes Bolsonaro’s Asset Sales

(Bloomberg) -- For its next expansion cycle, Brazilian industrial conglomerate Votorantim SA is eyeing less cyclical, state-owned power and infrastructure assets that may go up for sale.

With operations ranging from cement to orange juice, Votorantim is looking to resume growth but with a more defensive approach after facing years of economic malaise in Latin America’s largest economy, Chief Executive Officer Joao Miranda said in an interview in Sao Paulo.

One of the few investment-grade issuers left in junk-rated Brazil, Votorantim may team up with other companies for federal and local government offers. “There are many good assets, of all sizes,” he said.

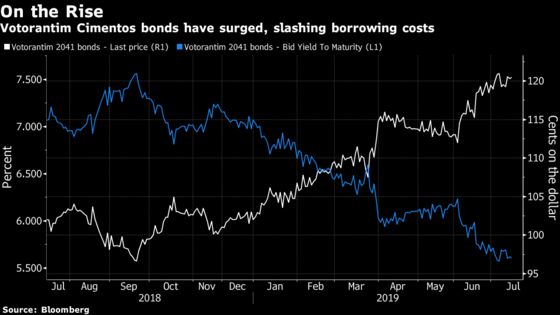

Votorantim group, with about $3 billion in outstanding bonds, has won over investors after slashing leverage over the past couple of years. Its cement unit has returned 21% this year on $610 million in notes due in 2041, the most among emerging-market industrial groups. The yield on the bond fell to a record low 5.6% earlier this month from over 7% by 2018-end.

Privatization is at the heart of President Jair Bolsonaro’s plans to lure investments and replenish government coffers. His administration has already auctioned concessions to operate several airports, port terminals and a major railway in the past few months.

That’s an opportunity for Votorantim The Sao Paulo-based company, founded in 1918 as a textile producer, has shifted toward more fixed-income-like industries, reducing its exposure to commodity swings and the ups and downs of the Brazilian economy. Illustrating its strategy, Votorantim earlier this year completed the sale of a controlling stake in pulp giant Fibria SA while acquiring power utility Cesp, which was sold by the Sao Paulo state government, in a joint venture with Canada Pension Plan Investment Board.

Votorantim will also weigh opportunities, directly or through its subsidiaries, in developed nations including the U.S. and Canada as it seeks to boost hard currency revenues as a hedge against the volatility of the Brazilian real, Miranda said.

Only seven Brazilian companies with outstanding debt are rated investment grade from at least two of the rating firms, less than half the number three years ago. Brazil is rated three notches below investment grade as the economy remains sluggish despite record-low borrowing costs.

--With assistance from Fabiana Batista, Julia Leite, Aline Oyamada and Tatiana Freitas.

To contact the reporters on this story: Gerson Freitas Jr. in São Paulo at gfreitasjr@bloomberg.net;Felipe Marques in Sao Paulo at fmarques10@bloomberg.net

To contact the editors responsible for this story: James Attwood at jattwood3@bloomberg.net, Reg Gale

©2019 Bloomberg L.P.