Bottom 50% of Consumers Are Showing Signs of Weakness, UBS Says

Bottom 50% of Consumers Are Showing Signs of Weakness, UBS Says

(Bloomberg) -- Lower-income U.S. consumers are showing signs of weakness despite the strong market, and if the economy enters a recession, any possible credit crunch could be “material,” according to UBS.

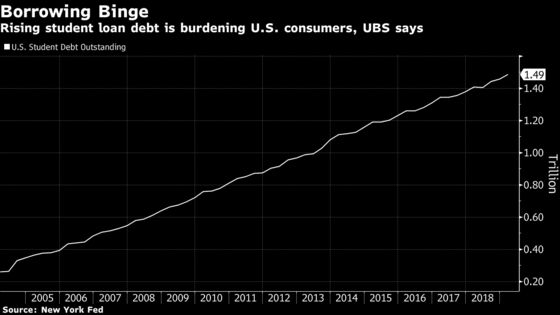

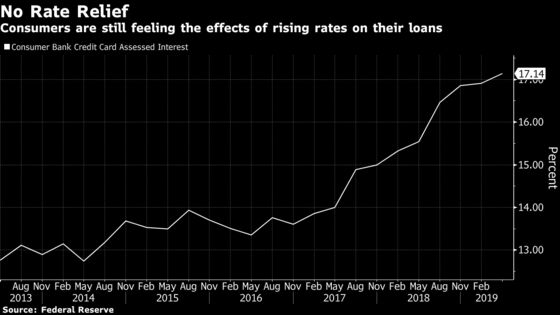

Strategists led by Matthew Mish and Eric Wasserstrom wrote in a note Thursday that they’re worried about lower-income consumers who have seen little net worth improvement since the financial crisis. Debt burdens for many of those households have grown as credit card interest rates hit record highs and student loan borrowings surged. UBS expects that the consumer credit cycle can extend but a future downturn could be worse than the one seen in 2001 and 2002 thanks to subprime consumers’ growing debt loads, higher losses and the growth of “fragile” non-bank lenders.

“Signs of softness fester in the lower tier,” the strategists wrote. “The Fed’s recent pivot should ease increases in future interest rates, although lagged effects of prior rate hikes will continue to filter into consumer loan rates.”

A UBS survey found that households reporting credit problems like loan application rejections matched a survey high of 40%, up 4 percentage points from a year earlier. Consumers’ likelihood of missing a loan payment in the next year increased 1 percentage point to 13%, with most households citing unexpected medical expenses as the primary reason. Many banks are tightening lending standards in response to an uptick on delinquencies on loans like credit cards.

Even though the Treasury rally has sent U.S. interest rates sinking, the strategists say many U.S. households are still seeing their interest burdens rise, similar to what occurred in the years before the crisis. The higher rates may come from a shift in what kind of debts consumers have: household debt was a record $13.7 trillion in the first three months of 2019, and most of the post-crisis growth in obligations has come from non-mortgage debts like student loans that carry higher interest rates.

While U.S. GDP has grown along with total consumer debt levels, “a growing share of GDP has gone to capital, not labor, and post crisis income gains have been below average for the lower tier consumer,” the strategists wrote.

Even though mortgage rates are falling, just 25% of surveyed consumers said they planned to buy a new home, the same percentage as a year earlier. The strategists said the sluggish demand may be explained by moderating wage growth and political and economic uncertainty. Other consumers cited problems getting mortgage credit or concerns about housing affordability. The percentage of households reporting that it was easy to get mortgage credit dropped 5% this year to 77%, and the percentage saying it was easy to find an affordable home declined 6% to 65%.

“Given low real wage growth and limited financial asset exposure it is hard for the lower tier to improve savings,” the strategists wrote. “The channel for building wealth is housing investment, but this is increasingly out of reach for many households.”

UBS’s consumer credit analysts expect some deterioration in delinquency rates, but say positive wage growth should help most consumers stay current on their obligations. They’re more concerned about long-term trends because consumers’ finances aren’t recovering as well as their credit scores might indicate. They estimate some $2.6 trillion of U.S. household debt is subprime, and any future downturn would likely affect lower-tier U.S. consumers, instead of a more systemic problem like 2008-2009.

In parts of corporate credit tied to consumers, UBS is neutral on investment-grade banks after a strong rally so far this year and is reducing its underweight on high-grade auto companies for reasons including stable lending standards and reduced trade risks. In high-yield, the strategists recommend defensive areas like utilities and select health care companies.

To contact the reporter on this story: Claire Boston in New York at cboston6@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Allan Lopez, Rizal Tupaz

©2019 Bloomberg L.P.