Boom or Bust? Brexit Makes Property Outlook Hard to Read

Boom or Bust? Brexit Makes London Property Outlook Hard to Read

(Bloomberg) -- London’s biggest office landlords face an unprecedented situation: a political fork in the road that could send the real estate market in polar opposite directions.

Developers such as Land Securities Group Plc, British Land Co. and Great Portland Estates Plc bet on the way the market will look years in the future when they green light plans to buy land and build new developments. They are grappling with uncertainty surrounding Brexit through a combination of paring down debt, postponing large-scale developments and squeezing more out of existing projects.

“Clever management is all about managing those options and being appropriate with risks,” Toby Courtauld, chief executive officer of Great Portland, said in an interview. “We are really trying to have our cake and then eat it, whatever happens to the weather outside.”

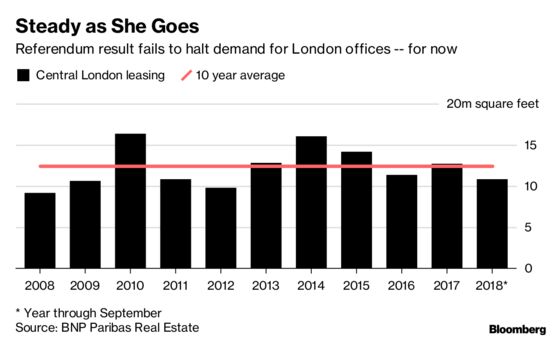

Even as the odds of a no-deal Brexit have come down of late, the political turbulence has disrupted the typical boom-and-bust cycle in the world’s most liquid property market. The process of committing to new developments over a multi-year period remains a risky proposition. Yet, if the office market manages to avert disaster -- as it has since the 2016 referendum -- companies that don’t have a pipeline of properties in the works face the prospect of missing out on years of profitable growth.

The dilemma for most office REITs is really whether or not to build. Land Securities, the U.K.’s largest real estate investment trust, stopped building on a speculative basis four years ago. The firm decided to secure tenants before developing properties to counter the risk of oversupply in a market that was heating up.

It has instead focused on filling existing properties with tenants on long leases, while reducing debt. The firm has also been pushing performance through refinancing and returning capital to shareholders. Land Securities will soon have to decide whether to resume projects without securing tenants beforehand: The first of three potential developments will be ready to start work as early as March, the same month in which Britain is due to leave the EU.

“I don’t think we will make a decision three weeks before Brexit,” CEO Robert Noel said in an interview. “No one knows quite what is going to happen, but we approach Brexit with an appropriate balance of low current risk and exciting future prospects.”

Overseas Buyers

British Land, the second-largest of London office REITs, has been rewarded for taking a more bullish approach in the past two years. The company has a pipeline of big new leases for projects it started in recent years without the assurance of new tenants. The firm has also divested two of its most valuable London office buildings since the Brexit referendum, as overseas investors -- encouraged by the pound’s weakness -- are still willing to pay high prices.

Still, British Land isn’t ignoring the risk of a crash. Instead of developing the site of an office building vacated by UBS Group AG in 2016, the company has refilled the existing premises by offering tenants short-term leases. The REIT intends to carry out the project at some stage, but for now it’s focusing on smaller developments and less costly refurbishments.

“What we like about all of that is the optionality that we have,” British Land CEO Chris Grigg said. “And that’s obviously relevant in the context of current circumstances.”

Adopting a cautious approach hasn’t prevented REIT shares from falling. Most London-focused developers still trade at wide discounts to the value of their assets because of the risk that Brexit will cause rents and values to fall. That, together with a lack of cheap opportunities to buy plots for future projects, means most landlords are finding it hard to replenish their development pipelines.

‘Challenging Outlook’

“We find it tough in the U.K.,” JPMorgan Chase & Co. analysts including Tim Leckie wrote in a note Friday. “Most management teams have done a good job navigating this unconventional property cycle, but the outlook is challenging.”

Firm are using funds raised from the sale of completed developments to return capital to shareholders or undertake buybacks. Great Portland announced its second buyback program in less than a year this month, which will push its gearing from less than six percent to a still-modest 11 percent.

“We have got more capital than we need to prosecute the existing developments we have on site,” Great Portland CEO Courtauld said. That still leaves the developer “bucket-loads of capital, which we need to exploit” any potential downturn. “It’s all about balance, and it’s a pretty tricky balancing act right at the minute.”

To contact the reporter on this story: Jack Sidders in London at jsidders@bloomberg.net

To contact the editors responsible for this story: Sree Vidya Bhaktavatsalam at sbhaktavatsa@bloomberg.net, Ross Larsen, Christian Baumgaertel

©2018 Bloomberg L.P.