Bonds From Mexican Airport That Doesn’t Exist Are in a Tailspin

Bonds From Mexican Airport That Doesn’t Exist Are in a Tailspin

(Bloomberg) -- Bonds sold to finance a $13 billion airport in Mexico City that was ultimately scrapped are among the region’s worst performers as investors question the revenue stream that backs them.

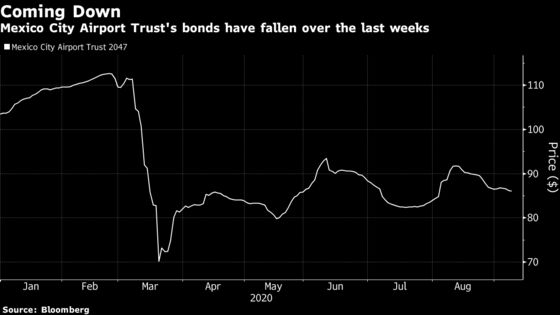

Notes due in 2047 from the Mexico City Airport Trust had a volatile first half and are now poised for their fourth straight weekly decline. Their drop to 86 cents on the dollar from above par at the beginning of the year is the seventh-worst performance in the Bloomberg Barclays Latin America Bond Index.

The notes have a tumultuous history. First sold in 2017 to fund a public-private partnership formed to construct a replacement for the capital’s aging and overcrowded Benito Juarez International Airport, the bonds crashed the next year after then President-elect Andres Manuel Lopez Obrador moved to cancel the project, saying it was a waste of money.

The government agreed in December 2018 to buy back $1.8 billion of the bonds and assured investors that passenger fees at the existing airport would be used to pay back interest and principal on the remaining $4.2 billion of debt. By late 2019, the longest-dated notes traded at 102 cents on the dollar.

While the notes have an implicit government guarantee, there’s growing concern that the trust’s ability to pay is under threat as the pandemic crushes global travel demand and sends Grupo Aeromexico SAB, the country’s No.2 carrier, into bankruptcy. Passenger fees have plummeted, with the number of travelers passing through Benito Juarez down 70% in August from a year earlier.

The trust may need to restructure the bonds and push back payments, according to Roger Horn, a strategist at SMBC Nikko Securities America in New York.

“Airport credits are normally as resilient as electric utilities and have been tested by 9/11, global recessions, pilot strikes and airline bankruptcies, but this pandemic tops them all,” Horn said.

Mexico’s Finance Ministry didn’t respond to a request for comment about a possible restructuring.

Fitch Ratings has the notes on rating watch negative “to reflect the possibility that liquidity within the Mexico City airport trust could rapidly erode,” analysts Astra Castillo and Rosa Cardiel wrote in a Sept. 1 note.

Still, the ratings company classifies them at BBB-, the lowest investment-grade rung, because of sovereign support and an expected steady recuperation in airport traffic.

Adrian Garza, an analyst at Moody’s Investors Service, said passenger volume will probably improve significantly by December. He added that the company has funds set aside for principal payments that could be used for interest payments if necessary.

“Before a restructuring, they have to exhaust all of these options first,” he said at a press conference. “For now, it’s not our base case.”

Aaron Gifford, a Baltimore-based analyst at T Rowe Price, says that speculation about a restructuring is overblown and that the project’s roots as a private-public partnership mean the government is likely to provide support. A cash injection as small as $500 million could provide enough money to cover interest payments for the next few years, he said.

“Sovereign support is high and this is a relatively easy problem to solve,” he said. T Rowe Price is the largest reported holder of the bonds, according to data compiled by Bloomberg.

“I’m positive on the bonds, though I recognize there’s some indigestion in the near-term given they’re exposed to the terrible airline sector,” Gifford said. It’s “just a matter of time until they trade back at par.”

©2020 Bloomberg L.P.