Bond Trading Slumps for Another Year at Canada’s Big Six Banks

Bond Trading Slumps for Another Year at Canada’s Big Six Banks

(Bloomberg) -- Canada’s biggest banks suffered the worst decline in bond trading revenue since 2011 as volatility pushed investors to the sidelines.

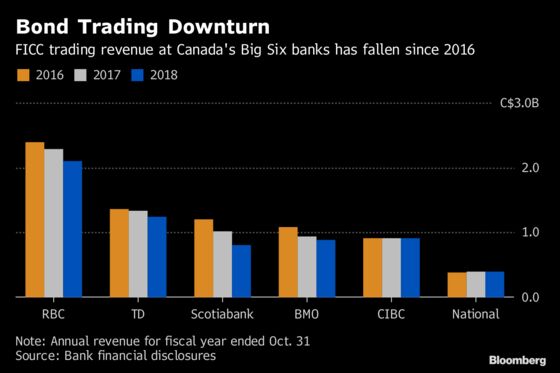

Revenue from trading fixed income, currencies and commodities fell 8.1 percent to C$6.32 billion ($4.72 billion) at the six large Canadian lenders in the latest fiscal year, a further erosion from the 6.1 percent decline in 2017, according to financial disclosures released this month. Revenue from those products, known as FICC, sunk to the lowest level in three years.

“Volatility finally emerged, which caused some investors to pause in activities and review their positioning and commitment to credit,” said Brian Calder, a trader and fund manager at Franklin Bissett Investment Management in Calgary, who oversees about C$6 billion in fixed income. “We have also seen issuers back away from the market and wait.”

This year’s decline in bond trading contrasts with the gains in equity trading, which rose 12 percent for the year ended Oct. 31, helping lift overall trading revenue at Canada’s Big Six banks to a record C$10.9 billion.

Fixed-income trading at the six lenders peaked at C$7.32 billion in 2016 -- a year with a 26 percent surge -- and annual revenue has declined since. Last year, FICC trading slid to C$6.88 billion, the first drop since 2014.

Volatility Plague

Bond traders were plagued with increased volatility amid Federal Reserve rate hikes and escalating trade tensions, which roiled markets in 2018. The Canadian investment banks saw only modest increases in arranging corporate bond sales and debt deals for provinces and government agencies in the fiscal year, which weighed on secondary trading revenue.

“The move towards risk-off had investors reluctant to expand positions but, at the same time, averse to move out from positions at a loss,” said Jason Parker, head of North American credit research at Bank of Montreal’s BMO Capital Markets division.

Royal Bank of Canada, which has the biggest trading shop among the Canadian banks, had an 8.1 percent decline in fixed-income trading, to C$2.1 billion.

“The market environment did remain challenging,” Jonathan Hunter, global head of fixed income, currencies and commodities at RBC Capital Markets, said in a phone interview. “Despite the fact that our volumes are up and our market share is growing, you’ve got a compression in margins and spreads due to market-structure changes, which have been ongoing and continue to be front and center for the business.”

Banks’ Declines

Toronto-Dominion Bank had a 6.7 percent decline in bond trading, to C$1.25 billion, while Bank of Montreal saw a 6 percent drop, to C$913 million. At Bank of Nova Scotia, it fell 22 percent to C$798 million and at National Bank of Canada it slumped 1.5 percent to C$391 million.

Canadian Imperial Bank of Commerce was the only one of the Big Six to see an increase in bond trading -- albeit a small one. The Toronto-based company had C$913 million in revenue from trading fixed-income, currencies and commodities, up C$2 million from a year earlier.

Representatives for TD, Scotiabank, National Bank and CIBC declined to comment on their FICC trading.

“Some banks are a bit more optimistic going forward and, if credit spreads narrow, there can definitely be more activity in this market,” said Foster Cheng, a director at Fitch Ratings. “Also, Canadian banks are very diverse and have other levers to pull on.”

Agency Trading

Fixed-income trading could shrink further in the coming year, when banks begin planning their financing needs under standards including the “net stable funding ratio” that determines the types of liquidity they must hold, said Parker of BMO. As the capital costs for holding inventory rise significantly, agency trading will become more the norm, he said.

Agency trading is when a dealer acts as an intermediary only, arranging a transaction between two investors without taking the position onto its own balance sheet. In that circumstance, the dealer would charge a fee for arranging the sale. Principal trading, by comparison, is when a dealer buys bonds from one client and then sells them to another, taking the position onto its balance sheet.

“Canadian banks are reluctant to act as a dealer in corporate credit. In many cases, they will act only as an agent to a transaction,” said Raymond Humphrey, a New York-based portfolio manager at AllianceBernstein LP. “My guess is that portfolio managers have adjusted to this new operating arrangement by reducing position sizes, migrating towards names that have broader sponsorship and are therefore easier to trade, and holding positions longer. I would not expect any of this to change in 2019.”

Performance on Canadian bond desks mirrors declines on Wall Street and in Europe, where fixed-income trading traditionally has been the biggest source of investment-banking profits.

Earlier this month, Citigroup Inc. Chief Financial Officer John Gerspach warned of a potential decline in fixed-income trading revenue. BNP Paribas SA, with one of the world’s worst-performing fixed-income units, said last month that its trading business was caught on the wrong side of the emerging-market selloff, blindsided by the Turkish currency crisis, and deserted by clients at home, even after investing to become a top-tier securities firm.

To contact the reporters on this story: Doug Alexander in Toronto at dalexander3@bloomberg.net;Paula Sambo in Toronto at psambo@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, ;David Scanlan at dscanlan@bloomberg.net, Daniel Taub, Alan Mirabella

©2018 Bloomberg L.P.