Bond Traders in Data Limbo Doubt Curve-Steepener Bets Have Legs

Bond Traders in Data Limbo Doubt Curve-Steepener Bets Have Legs

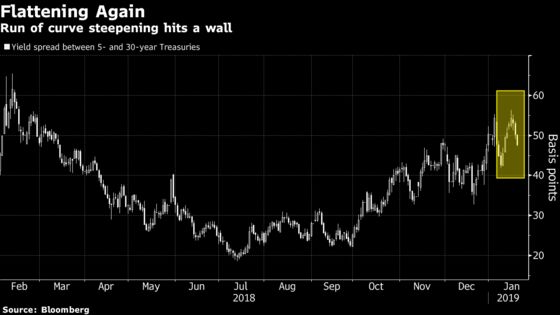

(Bloomberg) -- The past month’s burst of curve steepening in the Treasuries market may have run its course.

Traders crunched the curve flatter this week after the spread from 5- to 30-year yields touched the widest since February. Bond-market strategists see momentum behind the reversal amid improving investor confidence and rebounding expectations for Federal Reserve interest-rate hikes this year.

With the U.S. entering a holiday-shortened week, the government shutdown drying up the stream of economic data and the Fedspeak calendar empty, traders may comb through headlines on trade talks and corporate earnings for clues to the growth outlook. Signs of easing tension between China and the U.S. supported stocks this week and led traders to start rebuilding bets on tighter Fed policy this year.

“There’s a limited amount of data and potentially some trade headlines, so a lot of the focus is going to be on earnings,” said Gennadiy Goldberg, a strategist at TD Securities. “Some of the relatively solid earnings might actually help a rebound in sentiment that maybe the economy isn’t so bad. Maybe that will flatten the curve.”

At 3.10 percent, 30-year yields are about 47 basis points above those on 5-year notes, down from a recent peak of 56 basis points set Jan. 15. The shape of the curve matters because it’s viewed as a signal of investors’ economic outlook -- inversion is seen as a harbinger of recession. The gap sank to about 19 basis points in July, the lowest since 2007.

2019 Flattening Call

TD strategists are sticking to their call for 2019 -- published in November -- that the 5- to 30-year gap will narrow to 25 basis points, predicated on the Fed continuing to raise rates on the back of a strong economy.

In the market for fed funds futures, traders were even starting to price in a rate cut at one point in early January until Fed officials stressed that they’d be patient about further tightening. That reassurance and a solid jobs report helped ease growth concerns and traders are now factoring in about a third of a hike by October.

As long as the Fed intends to be on hold, “the time for a structural steepener is not ripe,” Bank of America Corp. strategist Carol Zhang said in a note Friday. The recent steepening was a reflection of growth concerns and a haven bid, rather than the beginning of a rate-cut cycle, she said.

Of course, there’s also a scenario where steepening resumes. For example, disappointing earnings -- next week brings results from companies including Intel Corp. and Texas Instruments Inc. -- could revive angst about the economy and stir up volatility in stocks. And there’s always the risk that the optimism about trade talks with China fades.

What to Watch

- The U.S. bond market will shut Monday for Martin Luther King Jr. Day

- On Jan. 21, the International Monetary Fund will release its updated World Economic Outlook, which is expected to show a downgrade to growth prospects; the Bank of Japan meets Jan. 23, followed by the European Central Bank the next day

- The shutdown means some economic data likely won’t be released, including durable goods and new-home sales

- Jan. 23: Weekly mortgage applications; FHFA house price index; Richmond Fed manufacturing index

- Jan. 24: Jobless claims; Bloomberg consumer comfort; Markit manufacturing and services indexes; Conference Board’s leading index; Kansas City Fed manufacturing index

- Jan. 25: Durable goods; new-home sales

- Fedspeak calendar goes dark in the lead-up to the central bank’s Jan. 30 decision

- As for Treasury auctions:

- Jan. 22: $42 billion of three-month bills; $39 billion of six-month bills

- Jan. 24: Four- and eight-week bills

To contact the reporter on this story: Alexandra Harris in New York at aharris48@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Greg Chang

©2019 Bloomberg L.P.