(Bloomberg Opinion) -- History shows that betting against the bond market is a fool’s errand. There’s no shortage of smart people over the years who have prematurely called the end of the bull market that began in the early 1980s. And while the market hasn’t avoided some rough patches, with the Bloomberg Barclays U.S. Treasury Index posting relatively small losses in 1994, 1999, 2009 and 2013, there’s been nothing like the “bondageddon” predicted. Even so, it’s hard not to think that bond traders are a bit too overconfident these days.

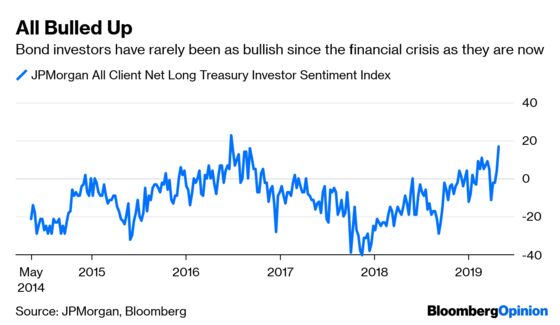

Treasuries rose broadly Tuesday as a widely followed JPMorgan weekly survey showed that bond traders are the most bullish since mid-2016. That’s when the U.K. voted to leave the leave the European Union in a decision known as “Brexit,” fostering concern the global economy would be upended. At the recent reading of 17, JPMorgan’s so-called All Client Net Long index is well above the average of negative 3 since the onset of the financial crisis in 2008. Bond traders clearly feel the Fed is done lifting interest rates and that the next move may be a cut, and perhaps soon. The odds of a reduction this year have risen over the past two weeks to about 65 percent from 40 percent as inflation has slowed, according to data compiled by Bloomberg. Yes, inflation has slowed markedly in recent months, but it’s still hard to see a rate cut happening anytime soon with the economy having expanded at a 3.2 percent rate in the first quarter, wage growth beginning to pick up and a labor market nearing full employment. According to LPL Financial, of the 45 times the Fed has cut rates since 1950, only 12 came after a quarter with output growth of 3 percent or more. Plus, in many of those instances, leading indicators had signaled impending weakness, which is not really happening now. On top of that, the latest data out of the euro zone and China are encouraging. “We see plenty of evidence that solid U.S. fundamentals are intact even as the global economy struggles with trade and political risks,” LPL Chief Investment Strategist John Lynch wrote in a research note Monday.

At the least, bond traders may want to bone up on their history. Although anxiety levels were elevated in mid-2016, Brexit ended up being a relatively benign event for the global economy. The Bloomberg Barclays U.S. Treasury Index ended up falling in the third and fourth quarters, dropping a painful 4.11 percent in the final six months of that year, which culminated with a Fed rate increase.

THE EURO’S LOOKING SPRY

A chief reason the Fed gave for its decision earlier this year to unexpectedly stop raising rates was the rapidly weakening economy outside the U.S. The central bank was concerned that sluggish economic growth in places such as the euro zone would drag America’s economy down. That was true then, but lately the euro zone’s economy has started to show some signs of life. The euro enjoyed its best month this year in April, rising about 0.80 percent against a basket of nine other developed-market currencies. The foreign-exchange market’s optimism was ratified on Tuesday when Eurostat said that the region’s gross domestic product rose 0.4 percent in the first quarter, twice the pace at the end of last year and more than economists predicted. Strong investment in Spain, buoyant consumer spending in France and a faster-than-anticipated rebound in Italy bolstered the 19-nation currency bloc, according to Bloomberg News’s Carolynn Look. Of course, 0.4 percent doesn’t mean boom times have arrived, but the upward trend is encouraging. “The euro area economy is regaining its footing after a very weak showing” in the second half of 2018, the economists at JPMorgan wrote in a research note Tuesday. “The initial impetus is expected to come from the fading of temporary drags. More gradually, we look for an improvement in underlying performance to sustain faster growth into midyear and beyond.” Not only that, firms including Goldman Sachs, NatWest Markets and Societe Generale are beginning to recommend trades to profit from the euro zone’s rebound.

MELT UP? WHAT MELT UP?

The U.S. stock market did little on Tuesday, with the S&P 500 Index rising just 0.1 percent to a new record high as a big drop in the shares of Google parent Alphabet Inc. weighed on the benchmark. Even so, that hasn’t damped talk that equities are in the midst of a “melt up.” There’s no exact definition of a melt up like there is for a correction — a decline of 10 percent from the recent peak — or a bear market – a drop of 20 percent from that same peak — but most generally believe it to be an accelerating increase in prices with no corresponding change in fundamentals. In that sense, this year’s 17.5 percent surge in the S&P 500 despite a Federal Reserve Bank of New York measure showing a 27 percent chance of a recession in the next 12 months shows all the hallmarks of a melt up to many market participants. But such thinking is increasingly at odds with any number of data points showing a stable economy. Besides the first-quarter GDP report, commercial and industrial loan growth as tracked by the Fed set a record in March at $2.36 trillion, and corporate earnings are on average coming in better than expected. And it’s not as if animal spirits are running rampant. Some 55 percent of stocks on the New York Stock Exchange are trading above their 200-day moving average, in line with the average of 52 percent over the past five years and far below the recent highs of 76 percent in September 2016 and 73 percent in July 2014. Wells Fargo head of equity strategy Christopher Harvey, who had one of the lowest S&P 500 forecasts, just boosted his year-end price target to 3,088 from 2,665, representing an increase of almost 5 percent from where the benchmark closed on Monday.

KOREA CONCERNS

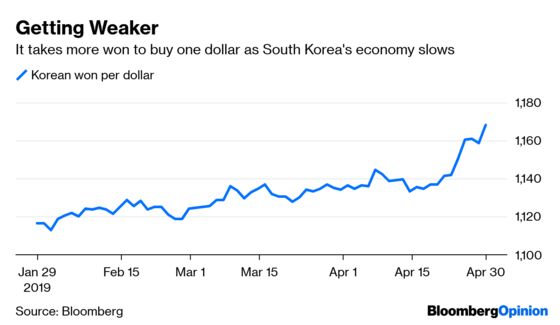

To be sure, there is still plenty to worry about, with many investors and strategists pointing to South Korea, which is a bellwether for global trade and technology. The won depreciated almost 3 percent in April in its biggest monthly loss since June 2018. Only Turkey’s lira declined more in April among 31 major currencies tracked by Bloomberg. Having dropped about 4.50 percent since the start of the year, the currency is now the weakest since the start of 2017 following a report showing the economy posted its biggest quarterly contraction in gross domestic product in a decade. “The fact that just under half of this year’s losses materialized last week speaks of a growing crisis of confidence in the currency,” BNY Mellon senior currency strategist Neil Mellor wrote in a research note Monday. The reason South Korea is watched so closely is because exports from companies such as Samsung and Hyundai account for about half the nation’s GDP. The Bank of Korea just reduced its 2019 growth forecast to 2.5 percent amid signs that global trade volumes are falling at the fastest pace since the depths of the financial crisis. Calculations by Bloomberg based on the Dutch statistics office’s trade monitor show a 1.9 percent drop in the three months through February compared with the previous three months, according to Bloomberg News’s Fergal O’Brien. That marks the steepest drop since the period through May 2009.

BEEF GETS BATTERED

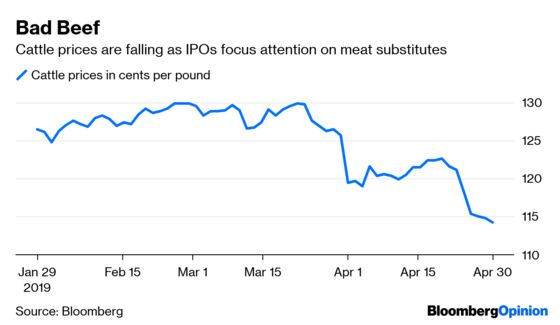

The cattle market is having a rough few weeks, with prices down 12 percent over the last five weeks or so, far more than the 6 percent drop in the Bloomberg Agriculture Subindex. It’s hard not to wonder if the weakness in cattle prices has anything to do with the increasing hype over the Beyond Meat Inc. initial public offering. The maker of vegan chicken and beef substitutes plans to raise as much as $241 million by selling about 9.63 million shares for $23 to $25 each, according to an updated filing Tuesday with the U.S. Securities and Exchange Commission. Just last week, Beyond Meat said it planned to raise as much as $184 million selling 8.75 million shares for $19 to $21 each. In other words, demand is high as investors bet on the growing market for plant-based protein products amid consumer concerns about health, animal welfare and the environment, according to Bloomberg News’s Deena Shanker. Startups such as Beyond Meat and Impossible Foods are tapping into that demand by offering beef-like versions of the veggie burger and other meat products. Supermarket sales of meat alternatives surged 19.2 percent to $878 million for the year ended Jan. 5, 2019, according to data from Nielsen. Regular meat isn’t going away though, with U.S. government data showing that per capita beef consumption is growing despite the rising popularity of alternative meat products, Shanker reports. The country’s beef consumption should rise to 57.6 pounds per person this year, the most since 2010, according to the U.S. Department of Agriculture.

TEA LEAVES

The Fed wraps up a two-day monetary policy meeting Wednesday by announcing its decision on rates, but it really is no decision as only one of the 89 economists surveyed by Bloomberg expects the central bank to reduce rates from the current target range of 2.25 percent to 2.50 percent. That’s despite President Donald Trump tweeting on Tuesday that he thinks the Fed should lower rates by 1 percentage point and resume its quantitative easing measures. Nevertheless, the Fed does face a bit of a conundrum, according to the strategists at Cantor Fitzgerald. “What should it do when data points towards solid U.S. economic growth, yet U.S. inflation remains sluggish and global growth dismal?” the Cantor strategists asked in a research note Tuesday. “We will be looking for expressions of concern about persistent inflation shortfalls, which would currently be the most persuasive argument for a cut.” As for those solid data points, the Institute for Supply Management is forecast to say Wednesday that its manufacturing index for April was little changed at 55, a level that denotes steady growth.

DON’T MISS

The Fed Should Dump Its Interest-Rate Target: Bill Dudley

At the Fed, Patience Isn’t a Virtue: Narayana Kocherlakota

Historic Stock Rally Favors Bears More Than Bulls: Nir Kaissar

Maybe Europe Can’t Recover From the Financial Crisis: Noah Smith

Turkey Can’t Just Wish Away Its Reserves Woes: Marcus Ashworth

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.