(Bloomberg Opinion) -- The masters of the universe are back, for a quarter at least.

Amid a deluge of earnings reports on Tuesday from Wall Street’s biggest banks, bond traders’ performance stood out across the board. At JPMorgan Chase & Co., which kicked off third-quarter results, trading revenue in fixed income, currencies and commodities soared 25% from a year earlier and at $3.56 billion easily topped estimates for $3.09 billion. At Goldman Sachs Group Inc., where shares tumbled after a poor performance in investment banking, FICC sales and trading was a bright spot. And Citigroup Inc., which is two months into a plan to cut about 400 people from its trading division, showed investors that it could still deliver with a reduced headcount: The bank’s fixed-income markets revenue reached $3.21 billion, exceeding analysts’ estimates for $3.06 billion.

A number of trends in the bond markets converged in the third quarter to make it a uniquely robust time for traders.

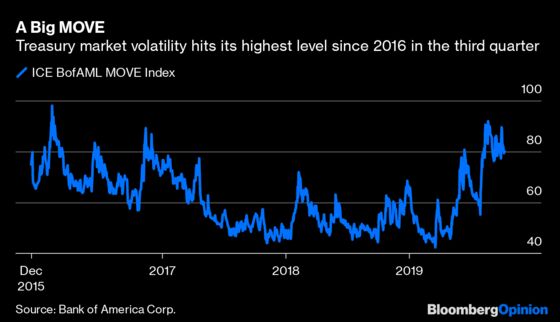

For one, the quarter was especially choppy for U.S. interest rates. The ICE Bank of America Merrill Lynch MOVE Index, which measures volatility in the Treasury market, surged in August to the highest level since early 2016. The benchmark 10-year Treasury yield swung to as high as 2.14% and as low as 1.43%. That 72-basis-point range was the widest since the final three months of 2016. As 30-year Treasury yields fell to record lows, some investors openly pondered whether it was only a matter of time before the U.S. joined other parts of the world with negative-yielding government debt.

While that didn’t happen, the sharp drop in yields encouraged companies to tap the bond market at a breakneck pace. A staggering 130 investment-grade deals cleared the market in September, eclipsing September 2017’s 110 offerings to become the busiest month ever for issuance of high-grade debt. That included 49 deals in 30 hours at the start of the month. Globally, September marked the first time that corporate issuance exceeded $300 billion in a month.

It follows that with so many new bonds hitting the market, bond traders were busier than usual. In each of the past three months, trading volume in corporate bonds reached the highest levels in at least seven years, according to Trace data. September was particularly elevated, with about $715 billion of total par value traded, up more than $100 billion from a year earlier.

The phrase “Masters of the Universe” comes from Tom Wolfe’s 1987 Wall Street novel “The Bonfire of the Vanities,” in which the protagonist was a bond trader. That and political strategist James Carville’s quip in 1993 that he’d want to be reincarnated as the bond market because “you can intimidate everybody” are two of the most prominent examples of turning Wall Street bond traders into larger-than-life figures.

It’s a much different environment now. While it was a banner quarter for fixed-income trading, it’s highly doubtful that banks can keep up the pace. For one, obviously it’s not as if every quarter can be record-setting in the corporate bond market. And with traders expecting the Federal Reserve to gradually lower interest rates over the next year or two, Treasury yields have seemed to stabilize at lower levels, bringing volatility back to earth.

On top of that, the leaders of Wall Street’s biggest banks are generally warning that the road ahead could be rocky. JPMorgan Chief Executive Officer Jamie Dimon and Goldman Sachs’s David Solomon both took a cautious tone on the economy, even before the International Monetary Fund cut its 2019 global growth estimate to a post-crisis low of 3%. Any sort of sustained slowdown wouldn’t bode well for the high-yield market. Last December, when that became a real concern, not a single speculative-grade borrower tapped the market, the first time that had happened in a decade.

It’s worth remembering that the yield spread between two- and 10-year Treasuries turned negative in August for the first time since 2007. Even though it’s no longer inverted, the curve from three months to 10 years was already negative for long enough to indicate potential bad news ahead for the economy. More specifically for banks, a flat yield curve immediately crimps their net interest margins. If they can’t deliver profits that way, they may need to focus on cost-cutting measures.

Banks should toast their bond traders. It will most likely be more of a slog for them in the months ahead, but, for a moment, they’re the indomitable force on Wall Street once again.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.