Bond Traders Are Eager to Get Past G-20 and Focus on Data Again

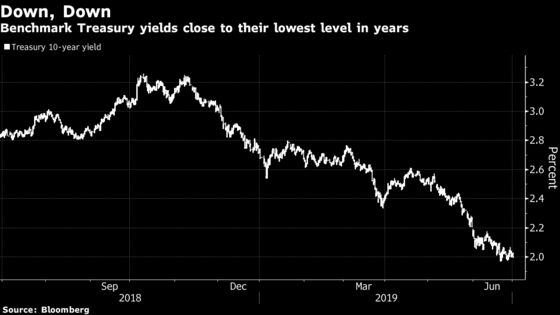

The U.S.-China trade dispute has helped push 10-year Treasury yields to their lowest level since 2016.

(Bloomberg) -- News from Osaka could ambush markets at any point, so now is the time to give some thought to why economic data in the days ahead -- and especially next Friday’s U.S. jobs report -- will be crucial for bond investors.

The U.S.-China trade dispute that’s the focal point in this weekend’s Group-of-20 meeting has helped push 10-year Treasury yields to their lowest level since 2016. But the strength of American payrolls has been one of the few tethers on the bond bull market. The 3.6% unemployment rate is the lowest since Federal Reserve Chairman Jerome Powell got his drivers’ license, by his own testimony. And it’s exhibit A for those who say the near-record economic expansion can continue.

Cracks may be starting to show in the labor market. Data for May showed a big slowdown in payroll growth, adding to concerns about the impact of tariffs against a darkening global economic backdrop. A second straight disappointment could see yields breach their recent lows. Conversely, the biggest risk for Treasuries would be a strong report that also hints at climbing wage pressures, says Chuck Tomes at Manulife Asset Management.

“If that came with average hourly earnings surprising to the upside as well, you could see a sharp move in a short period of time,” with yields spiking higher, said the portfolio manager. “If you combine that with positive headlines from the G-20 and a move towards an agreement happening, that could have implications for the U.S. Treasury market and pricing for the Fed.”

Traders are betting the Fed will take more drastic action than the modest cut it seems to be leaning toward as soon as next month. Market pricing reflects expectations the central bank will cut rates by around a percentage point in the coming year.

The market’s view may start to look more likely if the next round of purchasing managers indexes shows a further slide in activity in the world’s largest economies. Manufacturing sectors have broadly weakened, and the coming days bring reports from China and Europe. Service-sector data, which have generally held up, are due Wednesday in the U.S. and Europe. That’s the day before U.S. markets shut for the July 4 holiday.

Barclays Capital’s head of macro research, Ajay Rajadhyaksha, says that even if there’s a truce in trade hostilities following this weekend and payrolls rebound, U.S. yields are unlikely to rise more than a few basis points.

As long as inflation remains weak globally, and with negative yields making large swaths of non-U.S. markets “uninvestible” at this point, he doubts that much of the rally over the last couple of months will be reversed.

What to Watch

- Here’s the economic calendar next week:

- July 1: Markit U.S. manufacturing PMI; ISM manufacturing; construction spending

- July 2: Wards total vehicle sales

- July 3: MBA mortgage applications; Challenger job cuts; ADP employment; trade balance; jobless claims; Bloomberg consumer comfort; Markit U.S. services and composite PMIs; durable goods/factory orders; ISM non-manufacturing index

- July 5: Nonfarm payrolls report

- Fedspeak is thin:

- July 1: Vice Chairman Richard Clarida speaks in Helsinki on monetary policy

- July 2: New York Fed’s John Williams in Zurich on the global economic and policy outlook; Cleveland Fed’s Loretta Mester in London

- The auction calendar:

- July 1: $36 billion 3-month bills; $36 billion 6-month bills

- July 3: 4-, 8-week bills

To contact the reporter on this story: Emily Barrett in New York at ebarrett25@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum

©2019 Bloomberg L.P.