Bond Traders About to See If They're Underrating Inflation Risks

Bond Traders About to See If They're Underrating Inflation Risks

(Bloomberg) -- A debate is breaking out in the Treasury market before Wednesday’s release of U.S. consumer-price data as tumbling crude oil leads investors to ratchet back inflation expectations.

In one camp, you have the likes of Societe Generale SA. The bank sees price pressures building into 2019, fueling demand for inflation protection, in part as investors anticipate more U.S. tariffs on Chinese goods. Morgan Stanley agrees, saying the import levies and job-market strength should pressure consumer prices higher next year.

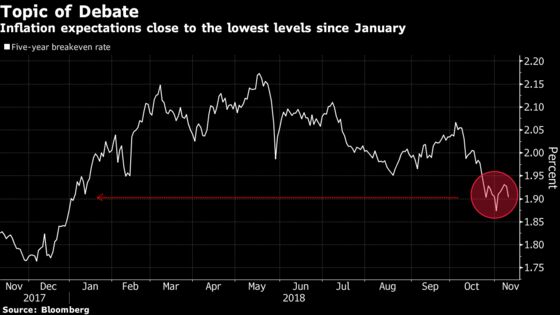

Traders are skeptical. The five-year breakeven rate -- which represents investors’ view on the annual inflation rate through 2023 -- has dropped to 1.9 percent, close to the lowest since January, from a 2018 high of 2.19 percent. Given that the lowest jobless rate since 1969 has yet to cause a jump in inflation, the market’s take is likely spot-on, according to BMO Capital Markets.

“It’s a rational response to the fact that we’re notably through sustainable unemployment levels and you’re not seeing broad pickups of inflation,” said BMO rates strategist Jon Hill. “We’re seeing this as an indication of building concerns about global growth several quarters out.”

The biggest question for bond investors is whether policy makers agree with their tempered outlook for consumer prices, or foresee accelerating inflation that could require additional rate hikes. Traders will get a read on that when Federal Reserve Chairman Jerome Powell speaks on the economy Wednesday evening in Dallas, following the Labor Department inflation data due that morning.

Pullback Week

Benchmark 10-year yields closed at 3.18 percent Friday, pulling back from close to a seven-year high as stocks and oil sank. The spread between 2- and 10-year Treasury yields flattened last week by the most since August as markets turned their focus back to the Fed’s tightening path in the wake of the U.S. midterm elections. Traders are pricing in nearly two quarter-point rate hikes in 2019, after an expected tightening in December.

Mary Daly, who took over as head of the Federal Reserve Bank of San Francisco last month, on Monday voiced her support for gradual rate normalization and said that she expects the modest uptrend in inflation to continue. She voted for the first time at the Fed’s policy meeting in November and will do so again next month, when officials are expected to hike for the fourth time this year.

Click here to read more about Daly’s views.

The CPI figures are the next key for the inflation debate. Consumer prices likely rose by 2.5 percent in October from a year earlier, according to a Bloomberg survey of economists, after a 2.3 percent increase in September. The CPI report is generally expected to be in sync with other data indicating steady progress on the Fed’s 2 percent inflation goal.

“The fundamental forces all point to higher inflation,” said Stephen Stanley, chief economist at Amherst Pierpont Securities LLC. “From here on, the risks are easily more to the upside than the downside. We’re going to get a significant overshoot on the inflation target.”

Go Long

Morgan Stanley in a note last week said it finds Treasury Inflation-Protected Securities and CPI swaps “highly disconnected” with the likely path of consumer prices in the year ahead. It recommended going long front-end TIPS on a breakeven basis, or one-year CPI swaps.

BMO sees a different scenario playing out. West Texas crude was on track for an 11th day of declines Monday and plunging oil could be a sign of things to come should the U.S.-China trade spat dent Chinese growth, reinforcing the argument for the decline in breakeven rates.

“If you get a slowing Chinese economy, that would have less global demand for commodities, which would be yet another downside risk to inflation,” said BMO’s Hill.

What to Watch This Week

- U.S. bond markets are closed Monday in observance of Veterans Day

- Powell’s appearance and CPI are the highlights of the week, while the Treasury will cram its bill sales into one day

- Here are the U.S. economic data releases:

- Nov. 13: NFIB small-business optimism; monthly budget statement

- Nov. 14: MBA mortgage applications; CPI

- Nov. 15: Empire State manufacturing; retail sales; Philadelphia Fed manufacturing index; retail sales; import/export prices; jobless claims; Bloomberg consumer comfort; business inventories

- Nov. 16: Industrial production; Kansas City Fed manufacturing index; Treasury’s international capital flows

- On Nov. 13, Treasury will sell a combined $164 billion of bills maturing in 4 weeks, 8 weeks, 3 months and 6 months

--With assistance from Emily Barrett.

To contact the reporters on this story: Katherine Greifeld in New York at kgreifeld@bloomberg.net;Shobhana Chandra in Washington at schandra1@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, ;Scott Lanman at slanman@bloomberg.net, Mark Tannenbaum, Boris Korby

©2018 Bloomberg L.P.