Bond Market’s Bulls, Bears Both Face Reckoning With 2020 Calls

Bond Market’s Bulls, Bears Both Face Reckoning With 2020 Calls

(Bloomberg) -- In the world’s biggest bond market, bulls and bears alike have reached a critical juncture with their 2020 forecasts.

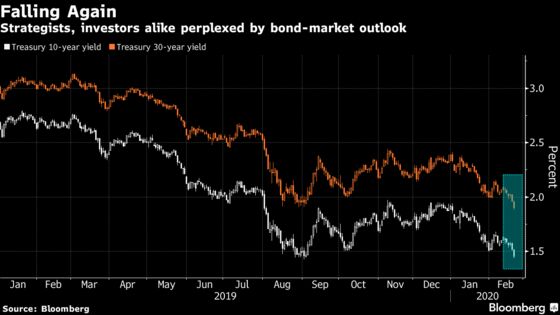

Concern over the economic hit from the coronavirus outbreak is pushing 10-year Treasury yields toward record lows once again. The market move poses a dilemma for Wall Street strategists. Those who saw lower yields in 2020 must now decide whether to drop their targets even further. And the bears, who seemed ascendant just weeks ago, have to figure out whether to throw in the towel altogether. For the time being, both camps appear to be standing their ground.

The debate encapsulates the quandary facing investors as they gauge the epidemic’s severity. Should they dive in and chase yields ever lower, assuming the outbreak will escalate and trigger aggressive Federal Reserve easing? Or is it better to hold off and wait for higher yields, in a bet the virus will be brought under control before long, bringing the focus back to the tight U.S. job market?

“We are getting a lot of client questions on what would be a catalyst for the rally in 10-year yields to extend further,” said Margaret Kerins, global head of fixed-income strategy at BMO Capital Markets.

“Many other portfolio managers are sitting on a wall of cash -- waiting to deploy it at higher yields -- and wondering just how high rates may go” if the virus’s impact proves temporary and growth rebounds.

For its part, BMO is sticking to its call that 10-year rates will end the year only a few basis points above current levels.

The torrid bond rally of the past two weeks has left 10-year Treasury yields at 1.47%, near the lowest since September. A report Friday showing a contraction in U.S. business activity offered the latest bullish jolt, which also pushed long-bond yields to a historic low.

There’s an enormous pile of cash ready to buy on any dips in bond prices, and the global growth backdrop is only darkening. China’s economy is grinding to a halt during the outbreak, while Japan looks like it’s slipping into recession. Germany’s outlook faces pressure too.

In the week ahead, there are only a few Fed speakers on the docket to offer fresh insight. And as far as economic data, which for now have been mostly overshadowed by virus concerns, an expected increase in the Fed’s preferred measure of inflation may buoy yields a bit. The weight of a combined $113 billion of 2-, 5- and 7-year coupon auctions may do the same.

But there’s little doubt that market direction will depend mostly on developments related to the virus’s spread.

Stephen Stanley, chief economist at Amherst Pierpont Securities, says U.S. output will weather the storm, and he sees inflation readings heading higher. His year-end 10-year forecast of 2.7% is the highest among almost 60 firms surveyed by Bloomberg. The median prediction is 1.95%.

“The virus is going to be a major problem for China and as a result it will have ripple effects to the U.S., but so far exposure here seems fairly limited,” he said. “A lot of the drag we are seeing right now is probably going to be reversed.’

Steadfast Bear

He sees little chance of a change in Fed rates policy before the November U.S. election, and expects the next move after that will be a hike. Officials have signaled they’ll stand pat in 2020, and Chairman Jerome Powell has indicated it’s not yet possible to gauge the ultimate impact of the outbreak.

But traders have boosted bets on cuts -- at one point on Friday futures were pricing in more than a half-point of easing in 2020.

Two quarter-point reductions are likely in the second half of the year as U.S. growth slows, said Jabaz Mathai at Citigroup Inc., a view the bank held at year-end as well. Its 1.25% year-end forecast for the 10-year is near the bottom of firms surveyed.

“Our thesis was that we were sliding into a slowdown anyway, with the virus just bringing things a little bit forward,” said Mathai, the head of Group-of-10 rates strategy. “Our essential valuation metric is where we see the fed funds rate going.”

For now, the 1.25% level seems a favored bottom point for many. It would mark a record low for the 10-year, which sank as far as 1.318% in 2016.

Mike Schumacher, head of rates strategy at Wells Fargo & Co., sees that area on the 10-year as a “pretty solid floor,” based in part on the history of the past decade and the yield’s tendency to reverse fairly quickly on breaks below 1.5%.

What to Watch

- Here’s the economic calendar:

- Feb. 24: Chicago Fed national activity index; Dallas Fed manufacturing activity

- Feb. 25: Housing-price figures; Conference Board consumer confidence; Richmond Fed manufacturing index

- Feb. 26: MBA mortgage applications; new home sales

- Feb. 27: Gross domestic product; durable goods/capital goods; jobless claims; Bloomberg consumer comfort; pending home sales; Kansas City Fed manufacturing activity

- Feb. 28: Advance goods trade balance; wholesale/retail inventories; personal income/spending; PCE deflator; MNI Chicago PMI; University of Michigan sentiment

- There are a smattering of Fed speakers:

- Feb. 24: Cleveland Fed’s Loretta Mester

- Feb. 25: Vice Chair Richard Clarida

- Feb. 27: Chicago Fed’s Charles Evans

- Feb. 28: St. Louis Fed’s James Bullard

- The auction calendar:

- Feb. 24: $45 billion of 13-week bills; $39 billion of 26-week bills

- Feb. 25: $26 billion of 52-week bills; $40 billion of 2-year notes

- Feb. 26: $18 billion of 2-year floating-rate notes; $41 billion of 5-year notes

- Feb. 27: 4-, 8-week bills; $32 billion of 7-year notes

To contact the reporter on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Nick Baker

©2020 Bloomberg L.P.